Här är en färsk analys av Tokmanni. ![]()

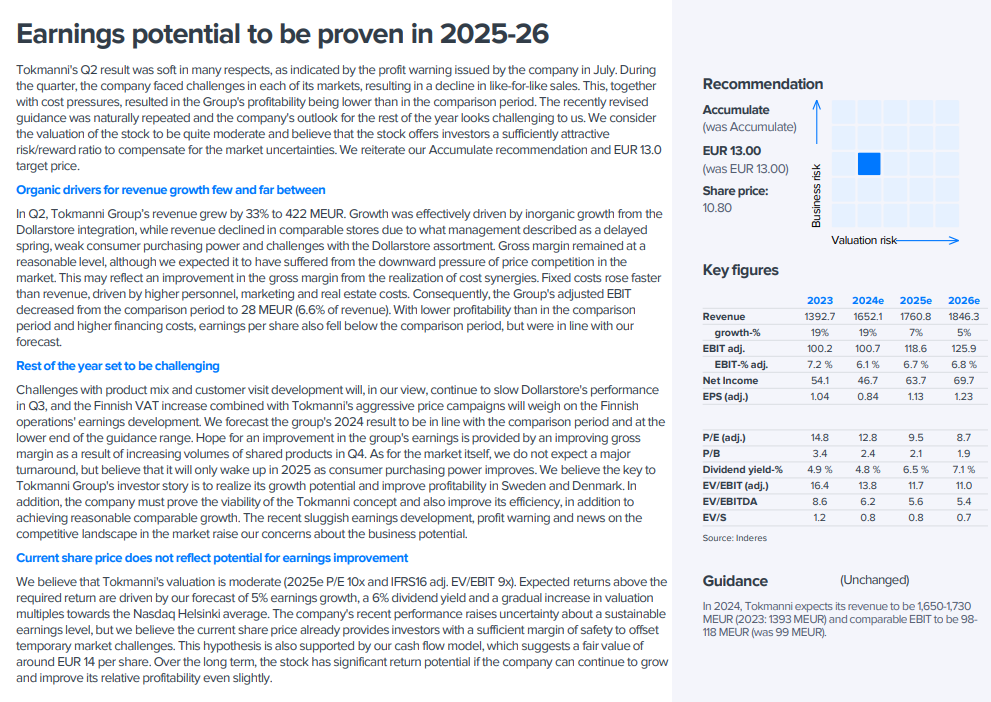

Tokmanni’s Q2 result was soft in many respects, as indicated by the profit warning issued by the company in July. During the quarter, the company faced challenges in each of its markets, resulting in a decline in like-for-like sales. This, together with cost pressures, resulted in the Group’s profitability being lower than in the comparison period. The recently revised guidance was naturally repeated and the company’s outlook for the rest of the year looks challenging to us. We consider the valuation of the stock to be quite moderate and believe that the stock offers investors a sufficiently attractive risk/reward ratio to compensate for the market uncertainties. We reiterate our Accumulate recommendation and EUR 13.0 target price.