Are you familiar with DollarStores private labels? How much of their sales come from private label?

This sounds very promising. I wonder if we´re going to see more acquisitions like ClickShoes, which increase the product range, or acquisition of smaller low cost chains?

The private label accounts about 25 % of Dollarstore’s sales and about 30 % of Tokmanni’s, and focus is to increase that level.

CEO Mika Rautiainen comment on the CMD that in Finland Tokmanni is not looking further retail chain acquisitions. In Finland, Tokmanni will grow by opening new stores. However, it is possible that Tokmanni buys some brands like they did last year when they bought Catmandoo, which is supporting Tokmanni’s clothing sales. I assume that in other markets they are open to M&A.

Tokmanni’s Q4 report was in line with expectations in terms of operational items. The integration of Dollarstore has progressed well and the company has shown the first concrete signs of synergy benefits. We see a slight reduction in the company’s risk level due to a faster-than-expected decrease in the debt position and positive integration news.

The target market for Kesko’s daily goods trade, Tokmanni and Lindex (department store and hypermarket chains) increased by 6% in May to 797 MEUR. Food products continued to grow steadily by about 5%, while the durable goods market increased by almost 9%. Within durable goods, growth was split between clothing, up 9.4 %, and home and leisure, up 8.5 %. According to our estimate, the market development of durable goods has been supported by the warm weather in May and demand that moved from the weak April. Kespro’s Foodservice market decreased by one per cent, while delivery days remained at the level of the comparison period.

Analyst Heikura’s Comment on Tokmanni’s New Announcements.

Tokmanni announced new store openings in Denmark during 2024-25. Considering the objectives stated in connection with the strategy update the announced store openings were expected, and thus do not cause any forecast changes.

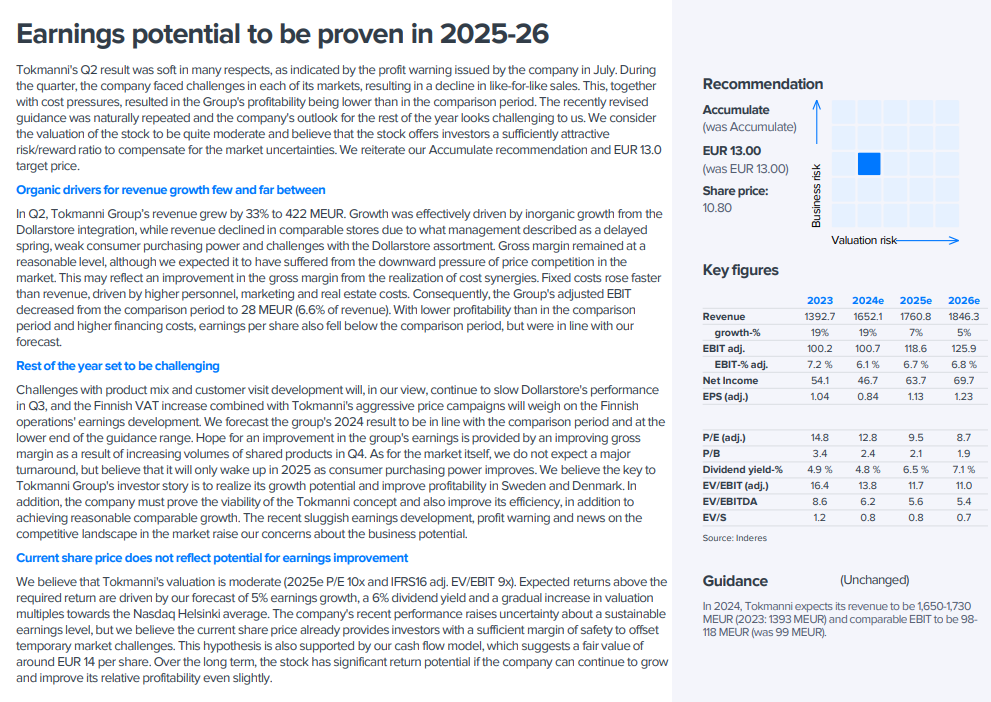

Tokmanni’s Q2 result was soft in many respects, as indicated by the profit warning issued by the company in July. During the quarter, the company faced challenges in each of its markets, resulting in a decline in like-for-like sales. This, together with cost pressures, resulted in the Group’s profitability being lower than in the comparison period. The recently revised guidance was naturally repeated and the company’s outlook for the rest of the year looks challenging to us. We consider the valuation of the stock to be quite moderate and believe that the stock offers investors a sufficiently attractive risk/reward ratio to compensate for the market uncertainties. We reiterate our Accumulate recommendation and EUR 13.0 target price.

Här ännu kommentarer angående hur den nu i höst höjda mervärdesskatten påverkar Tokmanni + att vi trots det “motiga helhetsläget” anser aktien vara köpvärd.

Att momsen höjs är en diksussion i sig (och detta ej ett politiskt forum, men kan inte annat än sucka)… och måste tydligen skriva detta.

Alla M&A’s tar sin tid, men kan inte hjälpa att undra, om detta ser ut att vara lite krångligt, dvs Dollarstore? Om jag inte missminner mig var det inte så mkt gnissel gällande Click shoes delen? Eller, correct me if I’m wrong…

Att segmentet “billighetsbodar med brett sortiment” är på stor frammarsch har knappast undgått någon… men i ngt skede kommer säkert ytterligare konsolideringar att ske, kunde man anta… Eller? (Detta nu mest Isa som drar ur hatten). Men om man fortsätter på Tokmanni-Dollarstore, Europris-Ö&B, Puuilo - Hurrikaani linjen är detta inte otänkbart.

Var passar Biltema, Motonet, Jula, Classe, Normal osv in i bilden? En personlig favorit i M&A pusslet är: när köps Halpa-Halli upp av någon av dessa? (Puuilo kunde vara en kandidat…)

@Lillen och @Dividendseglaren : hur tänker ni? Äger ni? Vem är den vinnande hästen i billigbodsracet?

Tokmannis resultat för Q3 överträffade förväntningarna och stärkte vår tro på en vändning i resultattillväxten fram till 2025. Det ökade konsumentförtroendet syntes i ökad kundtrafik i butikerna, vilket enligt Inderes skapar en stark grund för en framgångsrik julhandel och framtida tillväxt.

Lite reflektioner kring Tokmanni baserat på vad jag läst.

På den positiva sidan finns möjligheter till tillväxt i omsättning och marginaler, särskilt genom högmarginalprodukter som kläder och egna varumärken. Även en återhämtning i konsumentförtroendet eller bättre än förväntade synergier från förvärvet av Dollarstore kan stödja utvecklingen.

På risksidan kan utmaningar komma från prispress för att försvara marknadsandelar, väderförhållandens påverkan på sortimentet och konsumenters övergång till specialiserade lågprisbutiker. Dessutom kan den allmänna ekonomiska utvecklingen och svårigheter med integrationen av Dollarstore påverka resultatet negativt. Expansion ökar också de operativa riskerna.

Rusta:s resultat kan vara av intresse för Tokmannis ägare.

Här är analytikerns kommentarer:

Nordic discount retailer Rusta reported Q2’25 (August-October) sales broadly in line with expectations. However, earnings landed below expectations, possibly due to negative currency movements. Tokmanni, which we cover, appears to have outperformed the market in Q3, which we believe is a positive factor in overcoming the company’s early year hiccups.

Tokmanni Group har ingått ett nytt långfristigt finansieringsavtal på 325 miljoner euro, som ersätter det tidigare arrangemanget från 2021. Det treåriga avtalet inkluderar två ettåriga förlängningsoptioner och består av ett banklån på 250 miljoner euro samt en kreditlimit på 75 miljoner euro. Avtalet är kopplat till Tokmannis skuldsättningsgrad. Dessutom fortsätter Tokmanni sin expansion genom att öppna nya butiker i Nickby i Sibbo och i Sodankylä, där sortimentet utökas avsevärt. Tillväxtstrategin stöds också av Click Shoes-kedjans expansion i Tammerfors och Lahtis. Dessa åtgärder stärker Tokmannis position som en leverantör av låga priser och ett mångsidigt sortiment på den finska marknaden.

Här är information från en nyhet som är ett par veckor gammal.

Tokmanni har ingått ett samarbetsavtal med SPAR International, vilket innebär att SPAR-produkter kommer att finnas i Tokmannis butiker. Avtalet ger också Tokmanni rätten till SPAR-varumärket i Finland. Som en del av samarbetet kommer Tokmannis avdelningar för färskvaror att profileras under SPAR-namnet, och dessa ska utvidgas till fler butiker under 2025. Dessutom överväger Tokmanni att öppna fristående SPAR-butiker, vilket skulle innebära konkurrens med de stora aktörerna inom dagligvaruhandeln.

Genom att utnyttja SPARs globala inköpskedja kan Tokmanni förbättra sin prisstrategi, men de ekonomiska effekterna på kort sikt förväntas vara marginella. De lägre marginalerna inom färskvaruhandeln samt SPARs egna krav begränsar de omedelbara vinsterna av samarbetet.

Att öppna fristående SPAR-butiker vore ett ambitiöst steg, men konkurrensen mot Kesko, S-gruppen och Lidl är krävande. Dagligvaruhandelns lägre marginaler kan också påverka Tokmannis lönsamhet negativt. Samarbetet ses dock som en positiv strategi för Tokmannis tillväxt och utökning av produktutbudet.

Jag rekommenderar att läsa den här nya analysen om Tokmanni.

Tokmanni rapporterar sitt Q4-resultat på fredag klockan 8:00. Vi förväntar oss att slutet av året har gått bra för bolaget på alla dess huvudmarknader, vilket stöder vinsttillväxten. Bolagets guidning för 2025 borde indikera en tydlig vinsttillväxt. I samband med uppdateringen höjde vi våra vinstestimat något till följd av SPAR-samarbetet. Aktiens kursrally har enligt vår uppfattning ätit upp den mest flagranta undervärderingen. Vi sänker vår rekommendation till Öka (tidigare Köp) och höjer vår riktkurs till 15,5 euro (tidigare 14,0 euro) på grund av estimatrevideringen.

Tokmannis fjärde kvartal utvecklades starkt, även om marginalnivåerna visade viss svaghet.

Omsättningen och kundantalet ökade på alla huvudmarknader, och kostnadsstrukturen skalerade väl. Bolaget förväntar sig att både omsättning och resultat växer under 2025, men början av året kan innebära utmaningar. Tillväxten väntas accelerera mot slutet av året, särskilt tack vare Dollarstore-segmentet. Aktiens värdering är måttlig, och den starka utdelningen gör den till en potentiellt attraktiv investering.

Pia from Inderes and analyst Arttu discussed Tokmanni.

Tokmanni released its Q4’24 report on March 10. In the interview, analyst Arttu Heikura summarizes the result and tells us more about the Dollarstore segment and SPAR collaboration in Finland. We also learn how Rusta’s recent report compared to Tokmanni.