Tråd kring RVRC Holding som presenterade sin Q3 22/23 (brutet räkenskapsår) igår den 9/5.

Jag brukar tänka att jag är ansiktet utåt för den nya generation när det kommer till aktieintresse. En som läser mycket på diverse olika kanaler som nås av olika åsikter och tankar från många individer. Här kommer mitt första inlägg, halvt partisk då jag jobbar med detta hos Financial Hearings, men förhoppningsvis kan detta vara starten på något.

Om RevolutionRace

RevolutionRace erbjuder högkvalitativa funktionskläder för människor med en aktiv livsstil. Bolaget grundades 2013 av Pernilla Nyrensten och Niclas Nyrensten, Creative Director. Genom att sälja kläder online, direkt till konsument utan onödiga mellanhänder, kan RevolutionRace erbjuda produkter som har ett oslagbart värde avseende pris, kvalitet och design. Tillsammans med sina kunder har vi vuxit snabbt och säljer våra produkter till fler än 35 länder.

Men sedan augusti 2022 är inte Pernilla Nyrensten VD för bolaget. Den dåvarande ordförande i styrelsen Paul Fischbein, tog över som VD. Tillsammans med CFO Jesper Alm presenterade duon RVRCs Q3 rapport den 9/5.

Personligen är inte jag den som sitter på mest kunskap när det kommer till analysera rapporter. Så för mig är intervjun nedan väldigt intressant att lyssna på, då det ger mig mer klarhet kring RevolutionRace som aktie för mycket av rapportens innehåll summeras på ett enklare sätt.

@Isa_Hudd ställer sig frågan: hur sover VD Paul Fischbein? Se intervju av @Isa_Hudd med Vd Paul Fischbein här.

Kommentarer

Aktien har fallit omkring 18 procent sedan årskiftet med fick en halv-positiv reaktion på rapporten. Försäljningen minskar återigen på den nordiska marknaden men VD Paul Fischbein benämner att man är inte är så beroende av enskilda marknader längre. Investeringar sker inom marknadsföring (vilket man själv har märkt hos influencers). Men reaktionen från aktiemarknaden påverkades även av att man i rapporten flaggar för att tillväxten har varit högre hittills under innevarande kvartal.

Så det ska bli intressant att följa RVRC och se om förväntningar nu på tillväxten blir för hög till nästa kvartalsrapportering eller om det kan bli en positiv reaktion. RVRC kommer att presentera sin Q4 rapport den 15/8.

Skulle vara kul att läsa andras tankar kring RVRC, eller komma med förslag kring vad vi kan fråga VD Paul Fischbein om vi får chansen att intervjua honom igen vid nästa rapport.

I took a look into RVRC and its financials, and I was impressed by their business model and performance. Here are some noteworthy highlights on their financials:

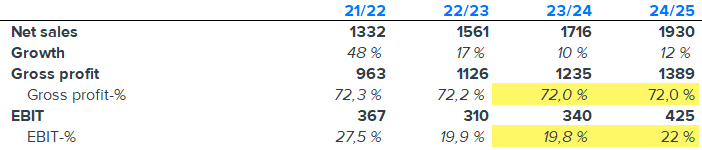

Gross profit >70 % - This is quite impressive considering the outsourced manufacturing and cost leadership within comparable producers. Also, the outsourced production keeps the balance sheet asset light and CAPEX needs low.

The company has low CAPEX needs and comparably low level of working capital (currently around 10 % NWC/Sales). This allows the company to translate profits efficiently to cash. Additionally, the balance sheet is debt free, which gives the company a solid position to invest in growth or distributing cash back to owners as dividends.

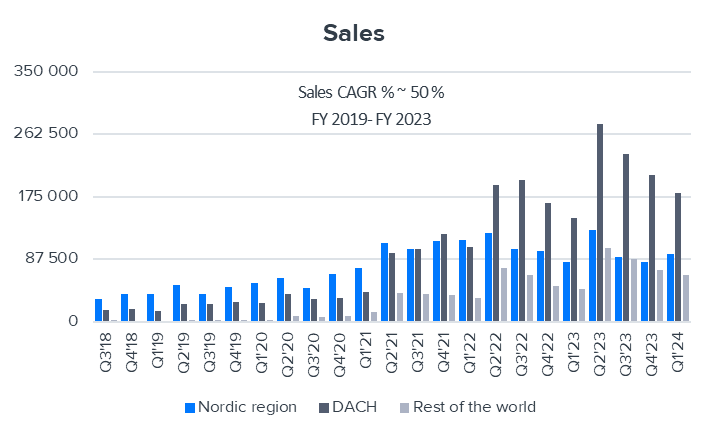

High ROIC (around 30 % in the last 12 months) and strong track record of organic growth (above 70 % revenue CAGR during the last three financial years) – If sustained, High ROIC with organic growth enables companies to create value. To add, the biggest line on the asset side of the balance sheet is goodwill. Thus, the operative return on capital is even higher.

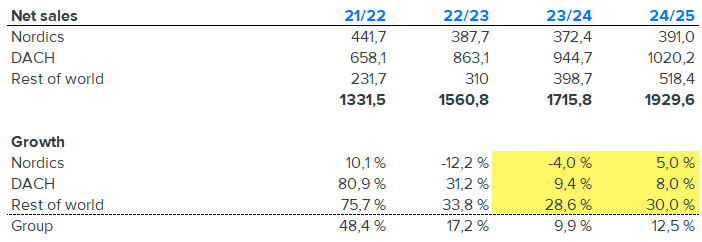

The growth has been exceptional, and it has probably been supported by an outdoor activity boom during Covid. In Nordics (the most mature market), RVRC experienced a decrease (- 11 %) in sales in the latest quarter, but strong development in the other market areas has kept the topline of the entire company growing. The management of the company seems optimistic about growth in new geographies (as they usually do :D). On the other hand, the stock market is clearly doubting the company’s ability to grow in the coming years.

The stock price has fallen around 70 % from the 105 SEK (30.12.2021) to SEK 32,34 (25.5.2023), and the valuation is around 10x EV/EBIT assuming stable EBIT for the current financial year.

för ett tillväxtbolag är den lönsamhet man kunnat uppvisa hittills imponerande

det är en sak att vara stor i Norden, en annan att ta sitt bolag “från garaget till en verkligt internationell marknad”, vilket grundarna lyckats med

att klippa mellanleden sänker kostnadsstrukturen över hela linjen: ja, men hur kommer köpbeteendet att se ut hos målgruppen i framtiden?

Om blickarna nu vänds mot USA: vad krävs det för att lyckas “på andra sidan Atlanten”

Som även berördes i intervjun: returer: något branschen lever med: hur stort blir problemet framöver? Konsumenter har tunnare plånböcker och håller hårdare i slantarna världen över. Returkulturen är även starkare inom vissa geografiska områden än andra.

lojala kunder = en oerhörd vallgrav

Då bolaget expanderar ytterligare (internationellt): varulager, logistik: rullar det på? Detta en oerhört viktig del av upplevelsen från konsumenthåll.

Fischbein, med sin erfarenhet av e-commerce säger: “jag tror på mig själv, jag tror på bolaget” låter alltid trevligt. (Med hänvisning till intervjun). Å andra: vad kan han annat säga :). Men han låter övertygande. I like it.

Few comments on the Q4 which went overall quite according to my expectations

Positives:

Germany still performing extremely well in tough market (+16 % CX adjusted growth, +27 % in SEK)

Rest of the World also still gaining momentum with 43 % growth (non CX adjusted). Especially positive comments on Netherlands, UK performing well, US growing fastest but still small numbers

Canada, Japan and South Korea local sites launched today

Slightly more positive comments in Webcast regarding the Nordic markets

Gross margin at strong 74,5 % level, very strong level even when considering one-time positive effects

Slight improvement in underlying operating profitability

July and early August growing >14 %

Overall great performance in very tough market conditions

Negatives:

Nordics still in clear downtrend (-16 % non CX adjusted)

Profitability still clearly below Q4’20 level (as expected)

Other DACH-markets than Germany performing weaker than previous quarters

Here are my rough estimates for the next two years and valuation based on these estimates and 35 SEK stock price. Valuation still seems quite moderate considering the high growth potential combined with high ROIC and profitability improvement potential. Greatest risk in my opinion is the large share (almost 50 %) of German market. If Germany would start to deteriorate, it would be hard compensate with other markets for quite some time.

Måste tillägga att det var synd att jag ej fick mig en pratstund med VDn Paul Fischbein denna gång. De presenterade sin kvartalsrapport i vår ena studio i Stockholm förra veckan - och jag befann mig i Stockholm precis då.

Tyvärr var presentationen ung. samtidigt som Hexatronics (då hade vi redan slagit fast att det blir en intervju med deras vd HLL) , vilket vi ej hade vid förra kvartalet (då vi däremot hade Revolution Race :).

Fischbein hade dessutom bråttom vidare, o måste susa till nästa ställe. Det måste man respektera. På rapportdagarna är ett VD jobb inget att avundas (de susar hit o dit hela tiden, det är ren o skär lyx om de tar sig tid o sitter ner o svarar på dina frågor). Hur som haver, så gick det helt enkelt inte att få till en intervju denna gång. Däremot kan vi försöka sikta på nästa kvartal, utan att lova ngt. (Man skall aldrig lova, iom att rapportdagarna kan se ut hur som helst).

Anyway: super sammanfattning av @Frans-Mikael_Rostedt ovan gällande rapporten. Presentationen (15 aug) ser ni här:

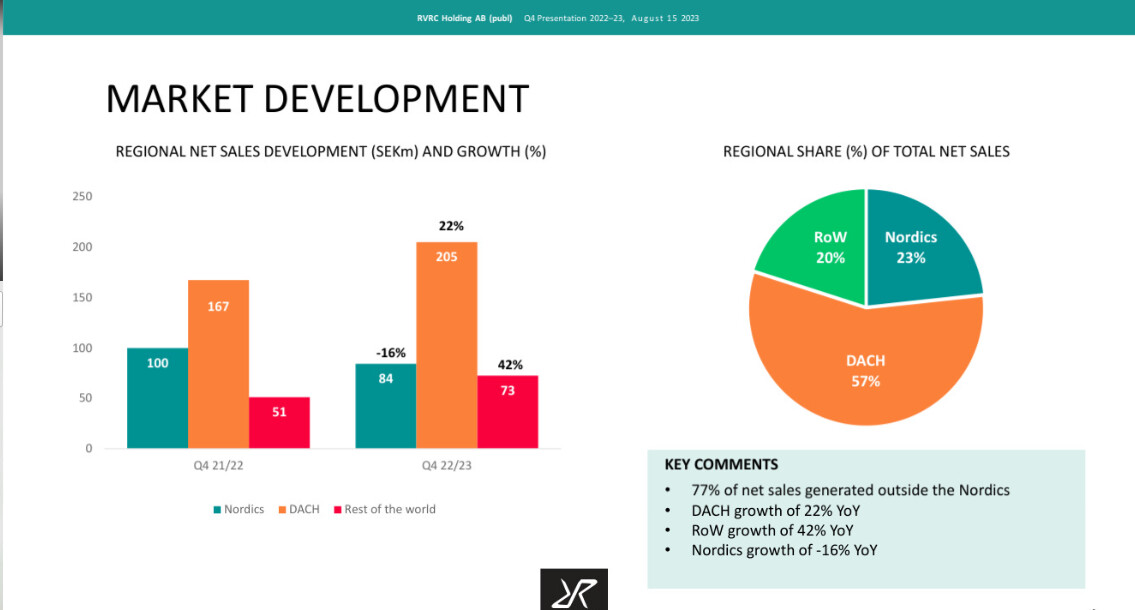

Här ett utdrag på gällande “Market development”:

DACH regionen drar tydligt, som även diskuterades senast.

Äger ej aktien. Är dock imponerad över bolagets resa “från garaget till världen”.

Summa summarum: vi hoppas på ny intervju i samband med nästa rapportering!

Q1 looking great at a first glance considering the market conditions.

“During the beginning of the second quarter, we have seen continued strong development with sales growth of around 20 percent. This is despite the weak market conditions.”

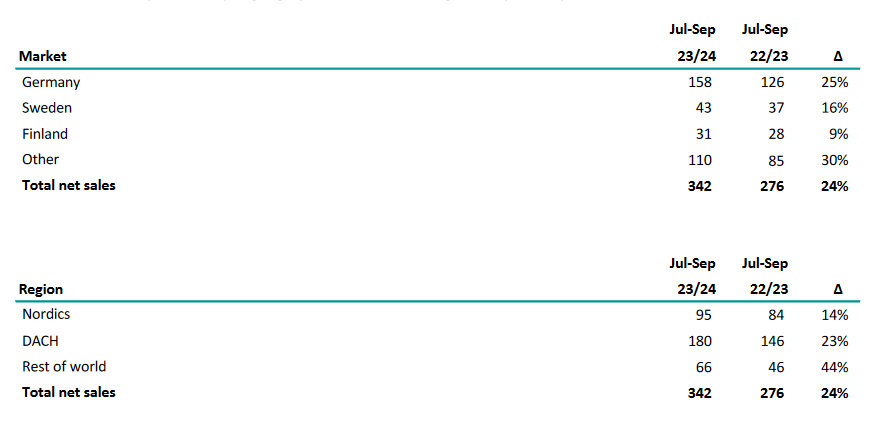

Net sales for the period increased by 24 percent and amounted to SEK 342 (276) million.

Gross profit amounted to SEK 247 (197) million, corresponding to a gross margin of 72.2 (71.4) percent.

EBIT amounted to SEK 67 (50) million, corresponding to an improvement of 34 percent.

EBIT margin amounted to 19.5 (17.4) percent.

Earnings per share before dilution amounted to SEK 0.47 (0.34) and after dilution to SEK 0.47 (0.34).

Sales growth for RevolutionRace in local currency amounted to 13 percent.

“The Rest of the World region showed the highest growth percentage in the quarter, with an impressive sales growth of 44 percent, with the UK and the Netherlands as the largest markets. At the same time, we see that the US is contributing to the growth in the region.”

All markets seems to be performing quite well again. Although it is good to remember that Swedish Kronor declined 10,7 % against euro compared to last year.

Very very interesting! Thank you for the summary, would have missed this otherwise. I remember looking at the company a while ago, but decided to stop researching because I was afraid that the growth might slow or decline if the demand for the products turned out to be a covid fad. How do you see this, do you think that the growth is durable?

The growth in Nordics seems to have saturated after Covid. However, the market share in Nordics is still low (below 2 % based on the market research put forth in prospectus). Thus, there is still room to grow, but I think that reaching double digit growth rate going forward will be difficult.

In contrast, the DACH region and the Rest of the World (RoW) have sustained a robust growth trajectory. It’s important to note that the Swedish krona has depreciated by approximately 13% against the Euro, and this currency effect has contributed to the reported sales growth in the recent quarters.

In my view, the RoW region holds highest prospects for ongoing robust growth. At present, the United Kingdom and the Netherlands are driving growth, and the launch of online stores in the United States and Canada increase growth potential.

For sure, the post Covid outdoor/online boom helped the company to achieve the outstanding 50 % sales CAGR between 2018 and 2023. I don’t expect the company to continue growing at this pace, but neither I’m expecting the growth to stop now. These are my thoughts, remains to be seen…

Inga direkta nyheter från RVRC under senaste tiden men aktien fortsätter gå starkt. Trots att den föll denna vecka (likt hela börsen) så ser det ljust ut om vi zoomar ut och ser från sommaren 2023 till idag. RVRC kommer att presentera det senaste kvartalet 30/1 och det ska bli spännande att se siffrorna som presenteras då.

Sorry @Lillen for the very late answer. @tommi.saarinen raised some great points already but here are few thoughts from me as well.

That has been my biggest fear as well, especially Germany which has so large share and has performed extremely well. Although Germany’s revenue per capita versus Finland and Sweden, which are more mature markets I would say, is still rather low and there should be still room to grow. The revenue split between countries is getting better and better by the quarter, but there is still a long way to go until Germany’s weight is balanced by other markets. I believe one of the main drivers for the stock will be continuing growth of Rest of world. I am not anymore scared of them being just a Covid fad at least as they have done still very well during these difficult economic times. Their marketing seems to be doing really good work and the existing social media accounts support nicely expanding to other countries. If UK and USA continue growing, there should be a lot of runway ahead. In short I believe their growth is durable, but Germany’s weight being still so large keeps the risk higher in the short term.

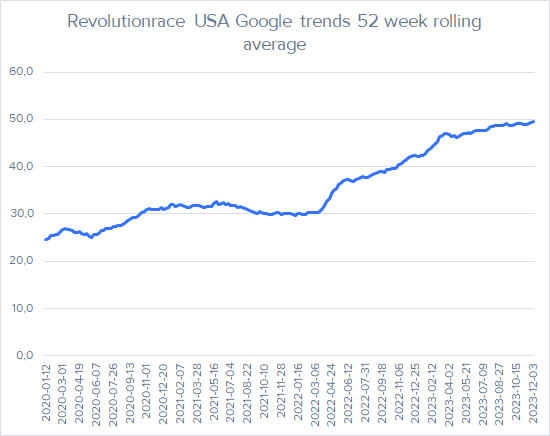

US Website traffic is also starting show some encouraging signs. According to Similarweb their website saw clearly increasing traffic at the end of the last year, especially in December.

Handelsbanken har sänkt sin långsiktiga rekommendation (på tre års sikt) för Revolution Race från market perform till underperform (som motsvarar sälj). Riktkursen höjs dock från 41 till 60 kronor. På tre månaders sikt upprepas rådet behåll.

Revolution Race-aktien backar med drygt 5 procent till strax under 60 kronor på torsdagsförmiddagen.

Handelsbanken noterar att aktien har ökat med 72 procent under de tre senaste månaderna och att banken tror på en lägre genomsnittlig resultatökning per år än konsensus. Vidare skriver banken att förhållandet mellan risk och förväntad avkastning har försämrats och att det är därför den långsiktiga rekommendationen sänks.

Ska bli intressant med rapport nästa vecka den 30/1.

RevolutionRace publicerade färska siffror idag där deras omsättning ökade med 21% under Q2 perioden. En hyfsat stark rapport som levereras efter att bolaget har gått starkt på börsen. Hur tar marknaden emot denna rapport?

VD Paul Fischbein och CFO Jesper Alm presenterar kvartalet klockan 10. Ni följer den här.

Något bättre övergripande resultat för Q2 jämfört med analytikernas uppskattningar. Vikten av Q2 (okt-dec) är hög för RVRC på grund av säsongsvariationer. Försäljningstillväxten var 21 %, Dach-området (särskilt Tyskland) var den huvudsakliga tillväxtmotorn. Tyskland stod för nästan hälften av intäkterna under Q2.

Justerat EBIT-% stärktes till 23,8 % vilket överensstämde med analytikernas förväntningar. Kassaflödet var utmärkt tack vare minskade lager nivåer och god lönsamhet. Tillväxten i resten av världen var något lägre än vad jag förväntade mig.

Det ska bli intressant att se om detta var i linje med marknadens förväntningar. Aktiekursen genomgår för närvarande allvarlig volatilitet.

Overall, the report turns slightly positive in my books. The 15% currency-adjusted growth and profitability in Q2 were excellent and somewhat better than my expectations, but the growth in Rest of the World slowed down a bit more than I expected. Considering the difficult market situation, the realized figures are still excellent in my books. However, RoW represents future growth potential, which is why its significance is so large. There were also no mentions of the development of countries in this region in the CEO’s review, as there usually are. In the webcast CEO commented that UK and Netherlands are good markets and US is growing the fastest but is still smaller than UK and Netherlands.

Positives relative to my expectations:

Strong growth and accelerating growth in Germany and the DACH region.

Germany grew by 21.5% currency-adjusted. On one hand, this increases dependence on the development in Germany again, but the accelerating growth is naturally positive and supports the idea that there is still market to win in Germany. Especially considering the current difficult economic situation. In my opinion the complete absence of a “corona hangover” in Germany strengthens the idea that there is still growth runway ahead. I still maintain somewhat cautious expectations for Germany.

The Nordic countries returned to clear growth at +8%. Positive surprise considering very difficult market environment especially in Finland and Sweden.

Growth continued in Q3 at the same level as Q2, which is stronger than my expectations.

Strong profitability with an EBIT% of 23.3% and adjusted 23.8%

Somewhat stronger than my expectations.

The workforce decreased slightly compared to a year ago, which was due conservative replacement hiring

CEO commented multiple times in webcast how they want to keep the growth balanced and profitable. Growth continues to be very value-creating for owners.

Very strong cash flow

Very efficient inventory management. The development of working capital is really encouraging. Although, in the future I expect the working capital to grow again more or less in line with the revenue growth. Net working capital 84 MSEK vs 203 year-on-year. The net cash position is so strong (340 MSEK) that the question is starting to be what will they do with it in the future? New business targets coming before July, in which I expect something more specific also regarding the capital allocation.

On the product side, the company reported that the launch of the Alpine skiing collection had been well received and brought in many new customers. This collection is naturally more cyclical though.

Negatives relative to my expectations:

The slowing growth in Rest of the World

No mentions of RoW countries in the CEO’s review

In the webcast they commented that main reason behind slowing growth was the balancing between profit and growth.

Despite strong profitability, the gross margin % slightly decreased compared to last year (70.7%), but remained at a good level of 70.2%.

November which is campaign heavy (black friday) and competitive this year was a very good month for them. This had a small impact to gross margins.

Blev ett het ämne här på sistione och tycker även olles inlägg belyser något oroande. Med det sagt så är det ÄGARNA som skapar frågetecken och gör en tveksam aktion för att möjligen trycka upp kurs innan avyttring. Nuvarande LEDNING med Paul i spetsen är däremot ett praktexempel på stark och skicklig ledare som kvartal efter annat visar på hans förmåga. Han lägger därtill in ett köp av aktier i samband med detta vilket jag tycker visar på hans intentioner med bolaget.

Jag tänkte på exakt detta i fredags när jag såg nyheten om att Paul köpte fler aktier efter rapporten. Det sänder en tydlig signal till aktieägarna efter att marknaden först nåtts av det som nämns ovan av Olle och som ledde till en del negativa rubriker. Men min känsla är att oron kan ligga kvar kring bolaget, då till exempel detta skulle kunna ske igen. Men vi får se.