Revenio är ett bra företag som nu har haft det lite svårare, men som ett kvalitets- och innovationsinriktat företag kommer det kanske att klara sig bra på lång sikt.

Därför behöver detta företag sin egen företagskedja.

Revenio är verksamt inom medicinteknik. Inom koncernen återfinns forskning och utveckling av tryckmätningsteknik som används vid behandling av ett flertal sjukdomar såsom glaukom, osteoporos, hudcancer samt astma. Verksamhet innehas på global nivå och drivs via flertalet dotterbolag med vardera affärsinriktning. Bolagets huvudkontor ligger i Vantaa.

Revenio has been a difficult case for me to crack. The moat and competetive advantage is there in plain sight, you have a high gross margin, strong growth, good ROIC. It´s a great company no doubt, but health care is a business area that´s difficult for me to grasp. How durable is the business and what could break it?

I started to buy Revenio way too soon, I think at 40€ish. I overestimated the resilience of the business model and as we saw they had to give a profit warning, which the market did anticipate (but I didn´t). I´m optimistic in the long run, but in the short time period, I´m not sure if there´s a risk for another profit warning? Like we saw with Incap, there´s seldom just one warning and it can be hard for the management to make accurate adjustments to the estimates after there has been such a long run of excellent performance?

A minor minus in this case, is that I´ve been wondering for a long while what is Revenio´s plan with Ventica and Cutica. They haven´t been a part of the strategy since 2021, wouldn´t it be best to sell these innovations? Or why isn´t anyone willing to buy them?

My understanding is that they are on divestment list but it’s difficult to find a buyer for them. On high level I would not give any weight for these when evaluating Revenio’s investment case.

Of course there is cyclicality element like seen this year, but overall I see the business model very resilient. Conservative buyers, new technology is slowly adopted, regulation etc etc… For example in IOP measurement Goldman standard dominated for over half a century as the standard way for measurement and it took Revenio’s rebound technology over 20 years to become a relevant alternative / challenger in IOP measurement - despite the obvious benefits compared with Goldman. Probably in imaging devices the technology cycles are a bit faster however and of course the future speed of change overall will be faster than history. But it is hard to get in to these markets but when you get there, it’s usually very good business. What could break it - I guess that instead of external force, that would more likely be the company’s own wrong strategic choices and over investing in some hype (not seeing these signs myself ) …

My personal take as a shareholder for over 10 years was that I’m happy to stay with the company for the next 10 years as well - though I sensed that some short term weakness is still ahead.

It’s a big transformation going from “one product” company (tonometers) into opthalmology med tech company… and they still have way to go in this transformation. I sensed that that acquisition is on the pipeline to get the final pieces needed for the product portfolio they want to have (my speculation). And from there the next big transformation is going from selling devices into selling solutions combining software and devices. You really need to take a long perspective when evaluating these transformations given also how slowly this industry evolves. But I feel the direction is right, they have good moats and they are continuosly working on wider moats. Also a firm “no” reply to a question if there is price erosion or price competition.

Interesting option in the investment case is still HOME product. I recall the buzz around that product already almost 10 years ago. You just need to remind yourself that with a completely new category, 10 years is a relatively short time in this industry

Revenio’s share has risen by nearly 20% since our previous update, which means the clearest buying opportunity admits the weakness has passed. We made small adjustments to our forecasts after the CMD, but the big picture is largely unchanged. The long-term outlook is clear and our confidence in this strengthened, but in the short term there is still weaknesses ahead and considering this, the valuation (2024e EV/EBIT 20x) is close to justified levels.

Q4/2023: Strong profitability and sales for our imaging and tonometry products

October–December 2023

Net sales totaled EUR 29.1 (28.3) million, up by 3.1%

Exchange rates did not affect the quarter’s net sales growth

Operating profit was EUR 9.5 (9.3) million, or 32.6% of net sales, up by 1.6%

EBITDA was EUR 10.5 (10.2) million, or 36.1% of net sales, up by 3.1%

Cash flow from operating activities totaled EUR 5.2 (11.7) million. Cash flow from operating activities was weakened especially by the increase in sales receivables as a result of the strong end of the quarter.

Earnings per share came to EUR 0.270 (0.214)

January–December 2023

Net sales totaled EUR 96.6 (97.0) million, down by 0.4%

The currency-adjusted growth of net sales was 2.2%

Operating profit was EUR 26.3 (29.7) million, or 27.3% of net sales, down by 11.3%

EBITDA was EUR 30.3 (33.1) million, or 31.4% of net sales, down by 8.5%

The EUR 1.0 million non-recurring costs of one-time projects had a negative impact on the operating profit and EBITDA for the review period. The adjusted operating profit was EUR 27.3 (29.7) million, or 28.3% of net sales, down by 7.9%. The adjusted EBITDA declined by 5.6% compared to the EBITDA in the review period.

Cash flow from operating activities totaled EUR 10.9 (23.2) million. Cash flow from operating activities was especially weakened by changes in working capital and taxes paid during the review period.

Earnings per share came to EUR 0.719 (0.818)

The Annual General Meeting was held on March 23, 2023. The dividend was confirmed as EUR 0.36.

The Board of Directors will propose to the Annual General Meeting of April 4, 2024, that a dividend of EUR 0.38 per share be paid

Som ägare är jag nöjd i resultatet. Var rädd för att omsättningen skulle sjunka. Framtiden verkar också bra bara marknaden inte blir sur.

Legendary analyst @Juha_Kinnunen has written an analysis of Revenio

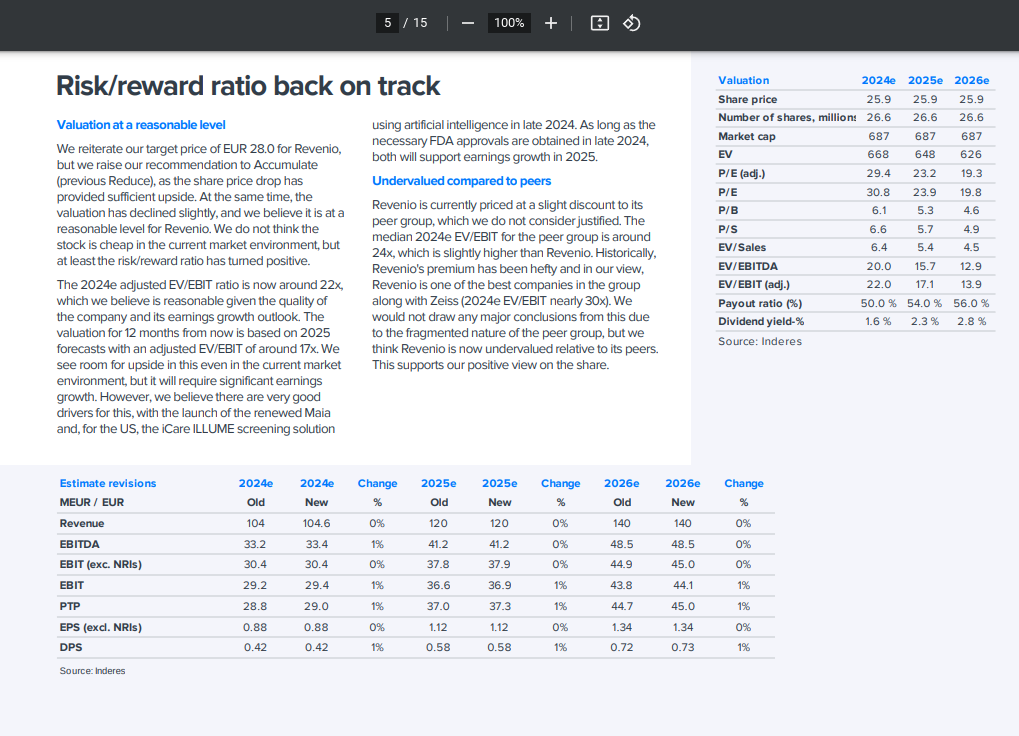

We expect the start of the year to still have been difficult for Revenio, with Q1 results below the strong comparison period, but a return to earnings growth thereafter. The valuation level is reasonable (2024e EV/EBIT 22x) relative to the outlook for the next few years, and the company is undervalued compared to its peer group. As a result, we consider the stock’s risk/reward ratio to be reasonably good again.

Nice to see that we some have interest in Revenio also behind to the Gulf of Bothnia

I’m visiting our Stockholm office, so I decided to see also what’s happening here. Sorry I haven’t been participating more in conversations - if you have questions about Revenio, tag me and I’ll try my best to answer

I guess it’s safe to say now that last years crash to around 20 € levels was a good buying opportunity as we thought at the time (buy recommendations in Autumn of 2023). Business seems to be getting back to profitable growth and outlook for the coming years is solid at least in my humble opinion. Generally strong fundamentals stayed intact despite a weak period.

The correction was quite sharp once sentiment started to improve. Now that the share price hovers around 30 €, valuation is no longer “cheap” and company needs to deliver earnings growth in the coming quarters. I’m quite confident that it will happen.

Of course the share price is also higher then our target price (28 €) and our recommendation is still acuumulate. One might reasonable wonder how the conflict should be interpreted, so here’s a general guideline - both will naturally be evaluated in the next update, but until then recommendation trumps over the target price.

Thank you for the thought-provoking message, Mr. Kinnunen.

Here are a couple of questions, if you have time to answer them sometime, that would be great. Thank you in advance for your responses!

How are Revenio’s new products, such as the renewed Maia microperimeter and the iCare ILLUME screening solution, expected to impact the company’s market position and earnings growth in the coming years? What are the key competitive advantages of these products?

Could you elaborate on the risks associated with Revenio’s FDA approval process in the United States and how these risks might affect the company’s earnings development? How has the company prepared for potential delays or failures in the approval process?