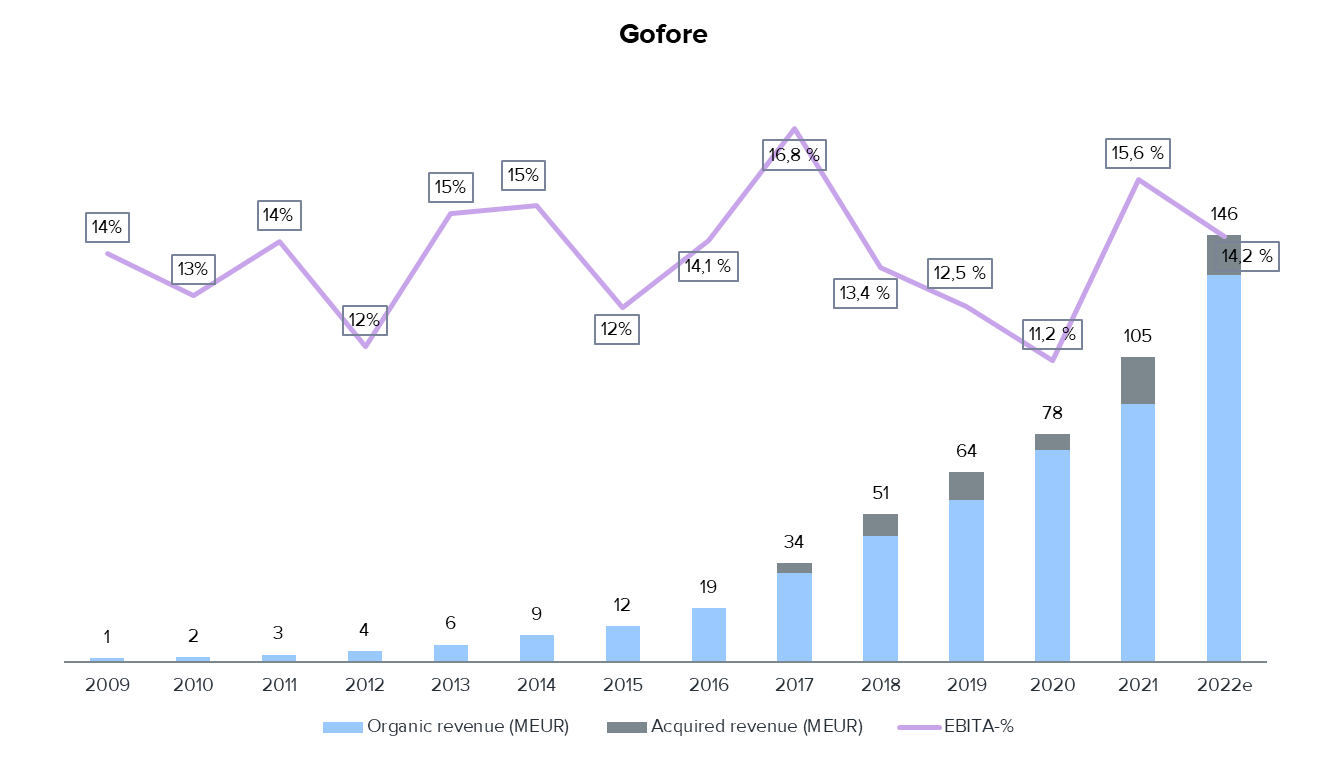

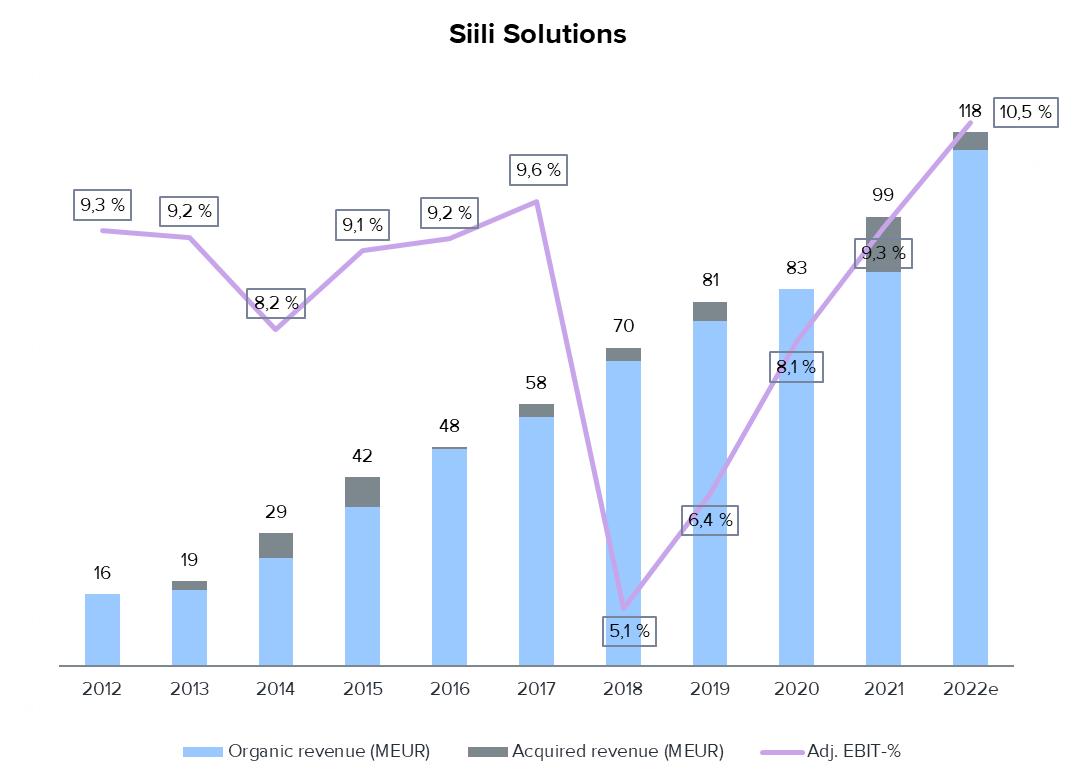

I am one of our analysts (Inderes) covering the IT-services sector in Finland, currently following Witted and Loihde. The sector has seen rapid growth, especially in the new IT-services segment (CAGR ~10 %), during the last ten years. In Finland, the amount of listed IT-services companies has now grown already to 12 firms in total. In the sector, there are many interesting firms in my opinion at the current valuation levels. Companies like Gofore and Siili Solutions have been few of the best performing stocks measured by the total return during their listed history. Both firms for example have created a great amount of shareholder value by organic and inorganic revenue growth combined with solid profitability while aiming to be the best workplace for their employees. Year by year they have been winning market share from the traditional actors while expanding into new customer sectors and services.

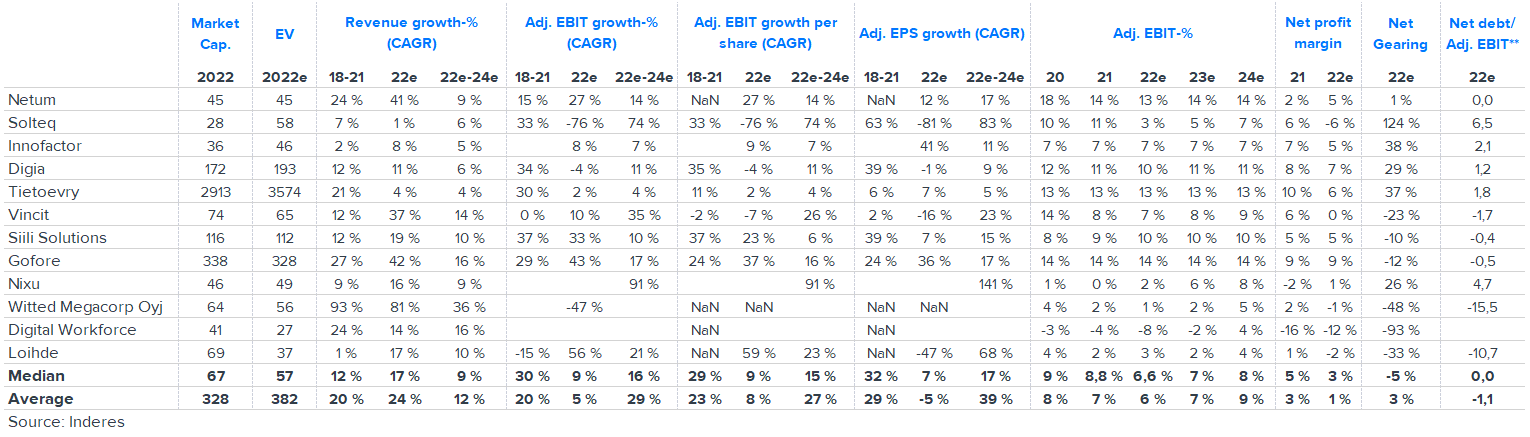

Here are some operating metrics of the companies from our coverage. During the last 3 years the revenue growth has been rapid with median growth being 12 % annually (CAGR). Profitability levels have also been solid during 2020 & 2021 and we expect some dip in the adjusted operating margins compared to these years as the general economic situation weakens. Cost structures were also a little bit lighter during the Covid-time as the firms had less travel expenses etc.

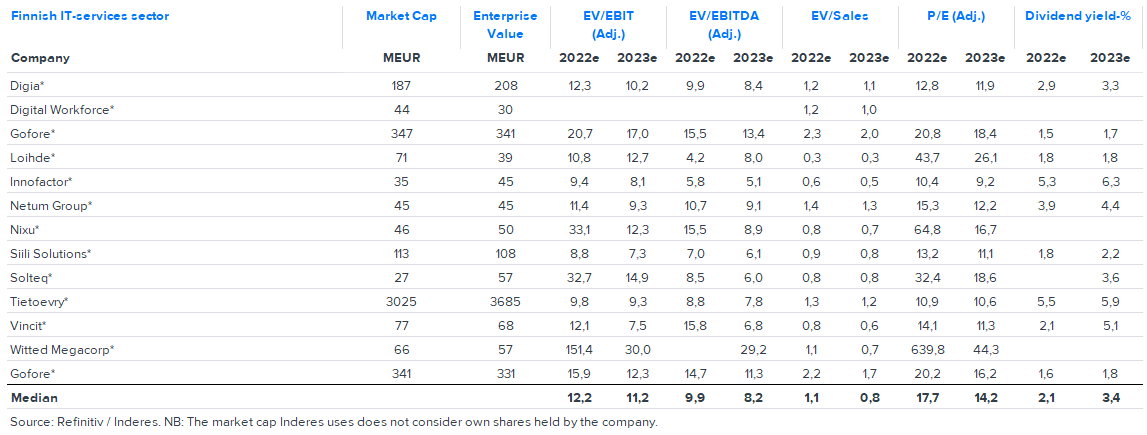

The valuation of the sector in general is currently quite moderate considering the long term potential of the companies and low capital intensity. The short term outlook is windy which justifies moderate valuation levels but in the long run the world is going to require more and more lines of code written. The competition for talent will continue raging also in the coming years and the constraints for new entrants will probably remain low which decreases the justified valuation levels. In my opinion, despite the weaker short-term outlook, with current valuation levels the sector offers a great opportunity to invest in the growth pockets of the economy with limited technology-risk.

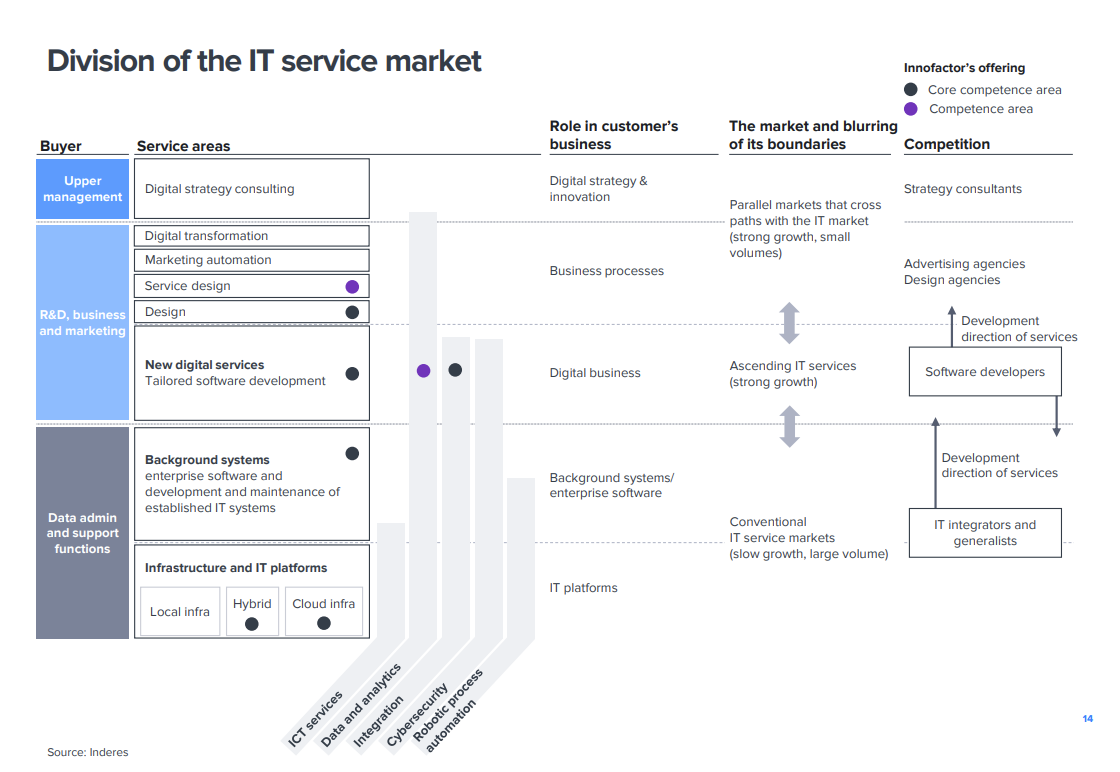

Here in the latest Innofactor extensive report we have described the market in depth (~15 pages) for those of you who are interested to read more. This is the high level division of the market in our view.

We are also looking to do an in-depth case study of the listed Nordic IT-services market. In the Nordic peer group we are currently including Bouvet, Enea, KnowIT and Netcompany outside of Finnish companies. Are there other Nordic firms which we should include in the Nordic peer group?

I love this sector, solid long term growth, cash flow and stable profitability with limited tech hype and no bullshit artists. I have pretty big weight in the sector in my portfolio with Gofore being biggest, a great company. Most latest addition is Loihde, not the sector star but 0,2x sales for a profitable company seems just undervalued, I have time to wait for the valuation to reverse towards sector levels even if it takes a few years.

Det som jag gillar med sektorn är definitivt den låga kapitalintensiteten och de återkommande, jämna kassaströmmarna, samt det som även ovan nämndes: den, i jämförelse låga teknoligirisken. Har personligen haft svårt att skilja bolagen åt -. ni får ursäkta en som gärna vill ha det så tydligt som möjligt, men som med allt annat: den som orkar läsa på, (vi har material !) kan även skilja agnarna från vetet. Min personliga åsikt är den, att det kan finnas många vinnare i denna bransch, men i längden måste man kunna leverera fortsatt mervärde till kund. Den som levererar kan även höja priserna.

Efter Q2’22 gjorde vi en djupdykning i sektorn tillsammans med @joni.gronqvist

Långt avsnitt, men fyllt med guldkorn för alla som orkar lyssna till slut. Förutom en allmän genomgång av branschen tittade vi även närmare på de olika bolagen och deras specifika kompetensområden och kundgrupper. Ta en kopp kaffe och lyssna : på svenska.

Siilens aktie är verkligen inte för dyr, dessutom kommer det ständigt nyheter om nya bra affärer. Jag tycker att det är trevligt att Siili har en bra position inom den offentliga sektorn och att internationaliseringen fortsätter. Jag litar på att det kommer att finnas organisk tillväxt i framtiden och att förvärv kan ge ytterligare styrka för lönsam tillväxt.

Generellt sett ser utsikterna för hela sektorn bra ut. Om vi bortser från kända riskfaktorer som brist på kompetens och löneinflation, vilka är de större riskerna för Siili efter dessa nämnda risker?

On a sector level, the big question in IT services right now is demand. We had severe talent war lasting for years. Now since mid 2022 and more strongly this year, we’ve seen the market’s growth bottleneck move from talent to sales. Many private companies have cut back their IT spending. Often the easiest place to cut spending is outsourced work, which especially impacts IT services companies. There has also been price competition as many companies have had a growing number of consultants benched without paying customer projects (bad for margins!) and are willing to compromise on price to lock in revenue. However, public sector demand remains stable and long customer relationships with private sector customers can also help combat the tougher demand environment.

My colleague @Frans-Mikael_Rostedt could comment on Siili specifically once he comes back from vacation

Thank you, Antti, for your interesting and excellent message!

One could imagine that especially in the long term, this industry will showcase its strengths the most. Of course, there can always be temporary “sluggish” phases, etc.

sluggish phases = mörnimisvaiheet

I need to monitor the situation more closely, and I believe that in this field, the best practices will gradually become more apparent.

To add to Antti’s comment, I would flag as more Siili specific risks the cyclicity of automotive industry and the uncertainty regarding how resilient Supercharge’s business is in this tougher economic market. They have both performed well in the last years (SiiliAuto after the Covid slump). If they would start to take hit by the tougher market conditions, it would slow down Siili’s overall performance. International business accounts for about 1/4 of Siili’s revenue and to our knowledge the profitability has been on a good level.

Siili was selected as the supplier for the areas of BackEnd (2.1), FrontEnd (2.2), and new projects BackEnd (2.5). The estimated total value of these three areas over the four-year contract period is 17 million euros.

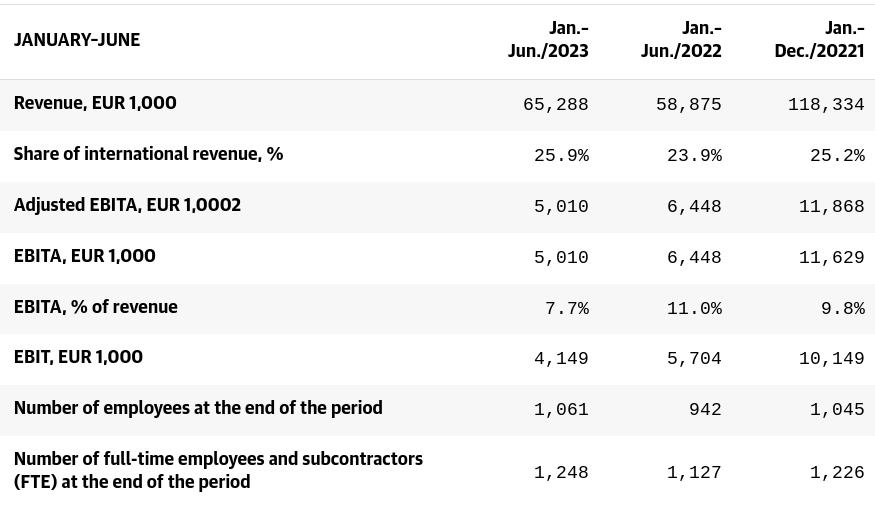

The estimated revenue for the year 2023 is projected to be 120-140 million euros, and the adjusted operating profit (EBITA) is expected to be 8.3-11.8 million euros.

Previous guidance for 2023:

The estimated revenue for the year 2023 was projected to be 125-145 million euros, and the adjusted operating profit (EBITA) was expected to be 12-15.5 million euros.

I have somewhat understood from some discussions and writings that in the IT service sector, at least some companies are facing a shortage of “jobs” when previously there was a shortage of labor.

If this is the case, then there doesn’t seem to be a significant fear of wage inflation anymore. However, has the situation in the IT service sector changed in any way or not?

Yes, the situation has changed quite quickly during the last year, especially in software development in the private sector. Demand in the private sector adapts quite quickly to the overall macroeconomic situation. The public sector demand has so far remained quite stable, but the competition has heated up. The companies with previously strong private sector weight in their customer portfolio have put more efforts in the public markets which has created price competition.

Companies in the sector have responded to slower demand with temporal lay offs (or “forced vacations” as we use the term in Finland). I believe this will dampen the strongest wage inflation, but at the same time collective labour agreements wage hikes will come into effect now in Q2. Q2 wage inflation will seem very high for many companies because the pay rises also include some one-time extra payments.

But on the other hand once the macroeconomic headwinds give away, the demand can pick up very quickly when customers increase again their software development budgets. It is very hard to believe that we would have reached some type of ceiling in the software development demand last year. Even if the AI will make the development more efficient and the customers want to be more in control in their software development projects.

Thank you again, Frans, for the comprehensive and excellent response!

I’m not in the industry myself, but I do follow it closely since I’ve invested in companies within the field. I constantly try to listen and read what other investors, analysts, and companies are saying about the situation.

Sometimes, I find it a bit challenging to keep up.

A somewhat anticipated result from Siili, as they had provided a negative profit warning in advance. The company has also initiated restructuring negotiations, and there have been some challenges for the company, but I believe the stock price has overreacted to the downside.

Enligt min åsikt har Siili-aktien kraschat alltför mycket, eller jag menar att jag upplever den som genuint billig. Visst har företaget stött på olika svårigheter, men om man ser på helheten och de långsiktiga utsikterna verkar företaget ganska bra.

Företaget internationaliserar sig, klarar sig bra inom den offentliga sektorn och effektiviserar sin verksamhet, dessutom är grundläggande faktorer på plats. Jag tror inte att löneinflationen framöver kommer att vara ett så stort problem och inte heller kompetensbristen, jämfört med vad det var tidigare.