Kortisktiga utmaningar, men långsiktig potential. Så sammanfattar @Antti_Luiro Saasbolaget LeadDesk i korthet på denna video. Bevis på lyckade internationalisering finns sedan tidigare och efterfrågebilden på sikt ser intressant ut.

Kolla in:

Läs även den “långa analysen” :):

Videoinnehåll:

Contents:

00:00 Introduction

00:12 Why read the extended report?

00:55 LeadDesk in a nutshell

02:30 Income streams 03:52 Businessmodel

07:00 International markets and competitors

08:49 Strategy

12:00 Valuation

Got a few questions on LeadDesk over email, sharing my comments here in case its interesting for other as well

Viking Ventures came in as LeadDesk’s major owner recently (release here in Finnish). I’m not expecting major strategy changes to be driven by Viking, but rather support for LeadDesk executing on current one (international growth, continuing expansion to Enterprise customers + tech focused M&A). Viking came in as owners to another SaaS-company I cover (Heeros) and I’ve so far heard good things from their SaaS-company network for knowledge sharing.

Current liability / working capital development has also raised some questions. I wouldn’t say I’m too concerned on that. LeadDesk sends a lot of invoices for of 3-12 month subscriptions in June & December due to contract timings, which shows in their working capital development. Also, 2021 year end current liabilities included a 1,5 MEUR earn-out for Loxysoft deal, which was irregular and paid out during 2022. 2022 year end current liabilities (non interest bearing) relative to revenue were actually quite close to 2020 levels.

But of course working capital development trend is something to keep an eye on going forward. Especially on receivables, as there we can has been an upwards trend relative to revenue (ties up more working capital).

Are there any other significant risks for LeadDesk beyond the challenges mentioned by Inderes below?

Challenges in new sales due to the company not being well known.

Does LeadDesk have particularly larger technology and cybersecurity risks compared to other companies in the industry? This question arose because you mentioned these risks in your report.

The success of integrating acquisitions and opening new markets.

Hey @börsen84 ! Sorry for the wait - just came back from vacation

We’ve tried to highlight our view of the most relevant risks in the extensive report, which happens to be in English for LeadDesk (from 12/2022 so largely relevant still!) - this is the best package we’ve built on LeadDesk so going through it should give a good view of the company & its risks as a whole

On a high level the risks are either company & market related. Market drivers are good in the long term, but some risks & impact from short term cycles is still there:

For the company internally the main factors are product competitiveness & sales execution. Also operational issues (e.g., scaling the organization & management model) are among possible risks and M&A can bring quite a few of these if unsuccessful.

I think for new market openings LeadDesk has actually a solid track record and they seem to have a model of getting around the initial lack of brand awareness in new markets:

M&A risks however are there and some did realise with LoxySoft (bought market share + overlapping tech). Technology driven M&A (complementary tech, not overlapping like with Loxy) LeadDesk has on the other hand done well and they are focusing there now. So I do feel that the risks are now lower (lessons were learned with LoxySoft acquisition ) but you never know how a M&A deal turns out right away.

For LeadDesk this is a more generic risk as for all software businesses I would say. Of course LeadDesk handles consumer info (customer service call/chat transcripts etc.) so problems might turn out painful, but naturally we’re not talking about e.g., personal health records so I guess LeadDesk is at roughly an industry average risk level here.

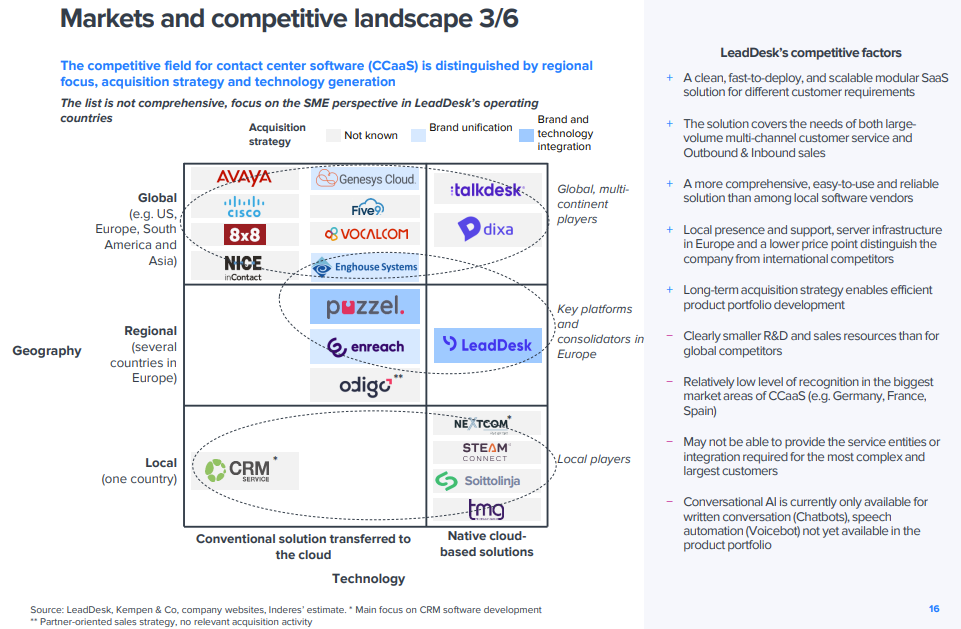

Another one to add is product competitiveness. LeadDesk does seem to be in a good position here (modern cloud product, good sales traction). Compared to the key consolidators in Europe, LeadDesk (along with Puzzel) are the only ones that seem to integrate on a technology level. Some players just buy similar players and give them a new logo, but then let each one run with their old product == lots of overlapping work if you want to keep evolving your product.

Integrated tech = R&D focus goes to developing one main product = less time wasted on overlapping development. This puts LeadDesk at a good position to keep their product competitive, but of course the largest global players win at the R&D resource game so it is not easy to tell how LeadDesk’s product competitiveness will fare in the long run

Thank you very much, Antti! I didn’t have to wait long.

I’m really, really pleased with your response - you answered much more thoroughly than I could have imagined. You told me a lot of new things that were partly unfamiliar to me or that I might not have fully understood before.

The extensive report is truly a comprehensive package and makes perfect sense. It’s really good and useful analysis, thank you for that!

I understand that LeadDesk’s product is excellent, and the management also seems to be competent. The fact that the CEO holds a significant portion of the company’s shares is noteworthy. Moreover, the company’s acquisitions have been successful, and it operates in a growing industry with scalable operations.

However, there have been recent challenges, such as fluctuations in weak currencies, and the company lacks significant visibility. Despite these factors, many aspects of the company appear to be in good shape.

The stock seems undervalued considering the expectations for the company. Perhaps LeadDesk needs to provide further evidence in the market to see its stock price “correct” and reflect its true value.

These are just my own thoughts and I might still need more evidence to buy a share.

n my opinion, LeadDesk’s revenue was weak in H1, likely due to the weak Norwegian and Swedish currencies. On the other hand, there was also nothing to praise in terms of operating profit.

I was expecting some interesting information about the outlook, but in my opinion, the company didn’t provide anything intriguing in that regard.

Overall, this H1 was unremarkable, somewhat poor in my view, but it could have been worse.

We had the same initial reaction with Frans when looking at the high level figures, but after digging into the figures Q2 were actually quite okay in our view:

Overall revenue growth for H1 was 9 % currency adjusted vs. 5 % in euros

Recurring revenue grew ~9 % (June 23 vs. June 22 - note, in Euros despite NOK&SEK negative effects being significant!)

Lower overall revenue mainly due to low project-revenue (mainly driven by the low volume of Enterprise-customer deployment projects linked to slow sales in this segment)

Only one of two customer groups is creating the recurring revenue growth (SME good, Enterprise bad). Enterprise companies have been prioritizing faster effect cost savings moves, but would be surprising if they don’t start software investments again as CCaaS they should be cost-saving in nature (just slower in effect >> second/third wave priority for saving costs).

ARR + 10 % y/y (this is their recurring revenue contract base, closed deals but not fully in billing = indicates growth prospects for next 3-6 months)

Outlook, as we interpreted it, was basically kept the same because small M&A is included in guidance - so 14 % growth is possible if LeadDesk buys a few smaller companies.

Research front page available here (only in Finnish unfortunately):

Quite often, I find myself in a situation where, after initially reading a press release, I think I have a clear understanding of the details. However, in the end, when analysts have examined the situation more closely, things haven’t always been exactly as they seemed at first.

Fortunately, ChatGPT translates Finnish text into English and vice versa quite well.

This is a very familiar experience I would imagine! Before I started working as an analyst this happened to me quite frequently as well.

When you spend more of your waking hours on looking at a particular company (+ have gotten used to how they report over a few years) and get the context & answers to your questions directly from the management, it often opens new layers to the reports. We of course try to close this transparency gap as well as possible with our content to make it easier for everyone to understand the companies not to say that we are always right - we definitely are not - but at least we try to lay out all the facts as well as possible to help investors make educated decisions.

Some companies are able to build their reports so clearly that a quick look already lets you get up to speed, but this is not always easy (and can take quite a bit of work). We frequently give feedback to the companies on what would make their reports easier to understand from investor point of view, but obviously not everything is feasible to be changed right away.

I understand what you mean very well. It is indeed a bit different to be a specialized investment professional, like a stock analyst, compared to an ordinary investor.

Easily, I might scrutinize the numbers in the same way for every company, even though they operate in different industries, which often requires looking at different metrics in different ways.

At times, I wonder about the day’s price reactions, but later I realize what perhaps more experienced investors have been considering.

In my opinion, Finnish companies are quite realistic and honest in their communications. Thanks to them for that!

LeadDesk has a good product, many things have fallen into place with their acquisitions, and they have the ability to continue making such moves in the future. The industry is growing, the CEO has been praised and holds a significant number of shares, the customer base is extensive, and the valuation multiples aren’t considered particularly high… etc.

However, how does the company compete with larger competitors, given that the company doesn’t have particularly strong visibility? In other words, how does the company succeed in international expansion in the long term? Because the company is sustainably generating clear results, I’m pondering, although right now the company is striving for growth. Why has LeadDesk’s stock price continued to decline? Is it the case that the company has simply not been able to convince investors with its current actions and figures, and perhaps there’s an expectation for the company to demonstrate more international and profitable growth?

To be frank, I can’t even quite fathom how the company will progress in the coming years, or if it’s moving too slowly and unprofitably. Of course, companies in the sector can scale effectively and have opportunities for significant margins and growth, but how will this company fare in the long term…

I will write a short update later this week after LeadDesk has reported their Q3-figures (coming out on Wednesday) in the meantime our comment before Q3 can be found here in Finnish and includes some perspective to these questions.

The automatic translation (easily available with Chrome) seems to get the main points across OK

Thanks for the patience! Busy days, now finally catching up on my forum backlog

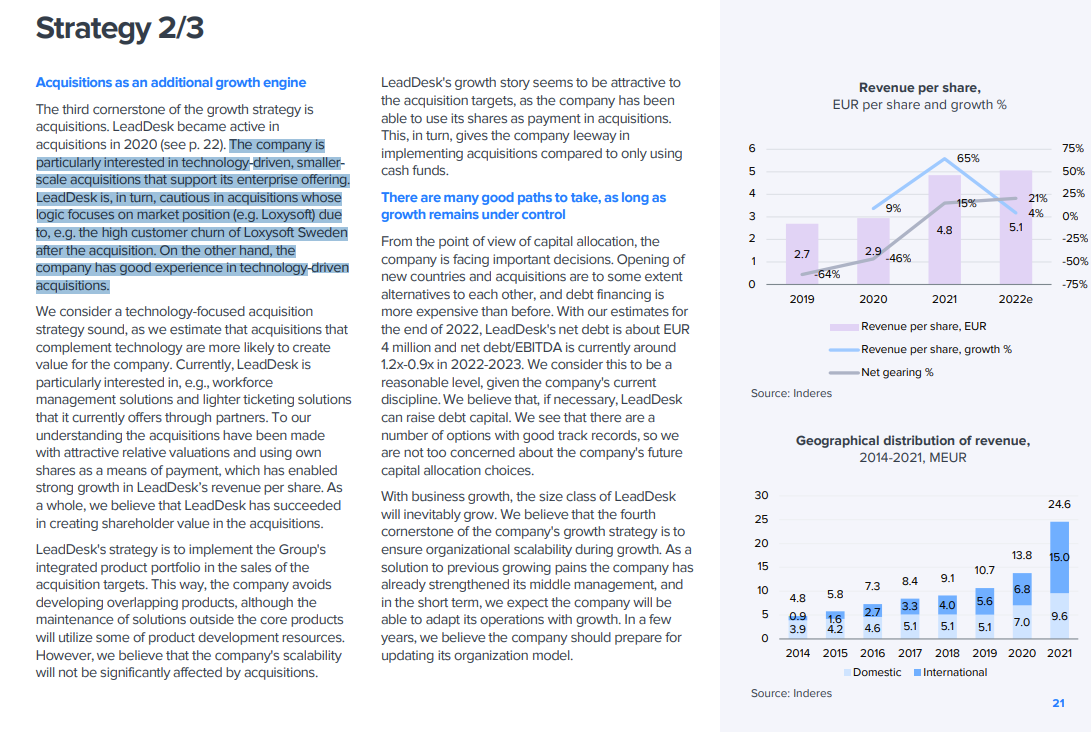

LeadDesk mostly competes with larger competitors in the Enterprise segment. This segment is worth pursuing when LeadDesk has first established a good brand and reference cases through smaller customers in the country. They have a pretty good track record in going in to a new market with SME sales first, with new markets turning cash flow positive in 2-5 years from launch (2021 entry to Spain was cash-flow neutral already year 1).

Anyways, in practice, LeadDesk’s Enterprise sales still focuses on Nordics where their foothold is strongest. There we probably have a typical competitive game around price / product / service quality / brand quality impression tough to get in the details of their competitiveness, but large players can sometimes price themselves too high + they might sometimes be a bit stiff in how they and their products adapt to customer needs. LeadDesk has had good success in Enterprise sales (prior to the industry-wide slowdown starting early 2022) which gives an indication of their competitiveness.

To put it simply, their growth has decelerated and I think markets are sceptical of growth improving. Market situation is indeed tough, but LeadDesk has taken multiple hits in the last few years. With a new problem emerging every 6-12 months it is understandable that investors are feeling a bit worried:

2021 H2: challenges with LoxySoft Sweden growth, post-covid churn (some customers won in 2020 went back to running physical locations instead of call centers)

2022: Customer churn (bankruptcies) due to energy sector crisis in Europe

The situation is double-edged. Our view is that LeadDesk is still in a competitive position in their markets, but at the same time their growth outlook some 12-18 months forward looks challenging. Their profitability is also still low and this doesn’t support their valuation. With growth and profitability the main drivers for Software product /SaaS company valuations, and LeadDesk not really getting support from either in the short term, there might not be great drivers for the valuation to climb. We still find the valuation very attractive and under the company’s fair value (which of course means we trust their growth will pick up after 2024), but I think it does require some patience before the drivers for stock price emerge.

By the way, on the Finnish forum I was challenged by one of our community members that this view & target price is too pessimistic. That might turn out to be true, we will see

Thank you very much, Antti, for your comprehensive answers!

Your responses provided a lot of new information and insights, some of which I hadn’t even considered.

LeadDesk seems to have many things going well for it, although I understand that there are various risks, and, of course, it’s challenging to grasp the longer-term prospects.

There have been exceptional circumstances in the economy, and the company has faced such unique situations, if I may say.

There’s a lot of potential in the long run, although it’s indeed challenging to predict too far into the future.

The stock has risen recently for good reason, but part of the increase has occurred, if I remember correctly, with relatively low trading volume, so there might be buying opportunities. I’m just contemplating…

There is risk in this company, but it also has a good leader and excellent software. Additionally, it scales well and handles acquisitions. The company has a broad customer base, no debt issues, and can use its own shares for acquisitions. There are risks, but it might be capable of growing in the near future both inorganically and organically, and quite profitably at that!

Företaget har uppenbarligen behållit sin position och förväntas naturligtvis prestera bättre när den ekonomiska situationen förbättras. Ja… alla företag gynnas av goda tider.

Branschen växer, det är tydligt. Produkten är fortfarande bra, så den har inte halkat efter eller åtminstone så antar jag.

Saker skalar upp och kostnaderna är inte höga.

Å andra sidan är det svårt att förutsäga hur företaget kommer att klara sig mot konkurrenterna på marknaden? Kommer det att bli hårdare konkurrens i framtiden, vilket påverkar marginalerna och omsättningen?

Å andra sidan, när branschen växer och företaget inte har misslyckats någonstans specifikt, så ser jag ganska positivt på det här relativt riskfyllda företaget.

Certainly, the company isn’t the most well-known, and perhaps it’s difficult to assess how the company will fare in the future. The product seems to be good, and frankly, I haven’t seen the management make any significant mistakes. In my opinion, the company has been fairly successful in its moves in the long run, if not quite good.

The CEO owns a lot of the company’s shares and seems to have a rather broad understanding of things… sometimes it feels like some other CEOs don’t fully understand their products or services, etc.

If and when the industry markets grow, why wouldn’t LeadDesk thrive? It already has some evidence to show and its products are used by quite diverse customers, some of whom serve as good “advertisements” for the company.

The market situation hasn’t been the strongest and it seems like we’re somewhat at the bottom. Is there only an upward trend expected here, barring any surprises or if there are some competitors, unknown to me, who might suddenly dominate the market with more advanced products?

My weakness has always been numbers, especially valuation multiples, and I don’t really understand them for companies like this.

LeadDesk saw slight organic growth, but profitability remained stable despite challenging conditions. The company has performed relatively well, and there are signs that its direction is clearly improving.

According to Inderes, the stock remains attractively priced (2024-25e EV/S 1.5-1.3x), and Inderes gives it a “buy” recommendation. The company’s long-term prospects appear promising, especially in Europe’s SME and enterprise sectors. Anticipated growth could lift profits to around a 20% EBITA margin in the long run.

LeadDesk’s valuation looks appealing, particularly considering its growth potential and profitability. Inderes’ estimate of fair value ranges from 9.3 to 12.9 euros per share, with potential for upward revision on stronger organic growth.

Finnish tweeter Passi wrote about LeadDesk as follows (translated from Finnish to English):

“AI has been the main reason for me not to invest in LeadDesk, even though the valuation has appeared tempting at times. I cannot assess whether the company will emerge from this rapidly changing landscape as a winner or loser. On the other hand, the same can be said for software development (e.g., Qt). What will these industries look like 10, or even five years from now?”

Analyst Antti Luiro responded with the following, accompanied by the images and screenshots below (Antti’s text translated directly from Finnish to English, so please consider that):

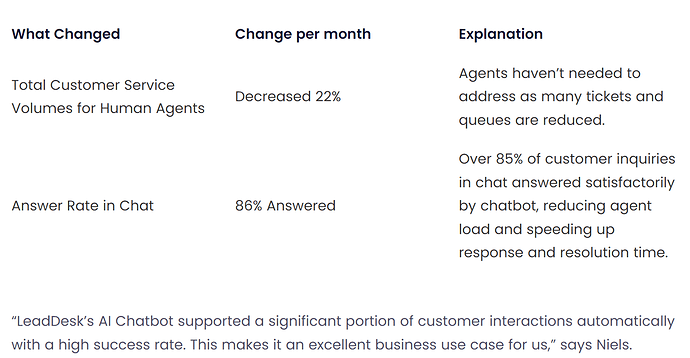

Regarding these customer cases, here’s a chatbot AI case from LeadDesk It took 2 weeks to implement. AI handles 86% of the inquiries (although the chatbot naturally increases the number of inquiries), and in terms of direct efficiency, after implementation, customer service representatives had 22% fewer tickets to resolve.

Innebörden kan ha ändrats lite under översättningen och jag kan engelska dåligt. Jag var till stor del tvungen att förlita mig på översättningsprogrammet.