Incap’s CMD was held a month ago. There were some excellent and useful slides. I recommend to go trough the materials. Here a few highlights that I did.

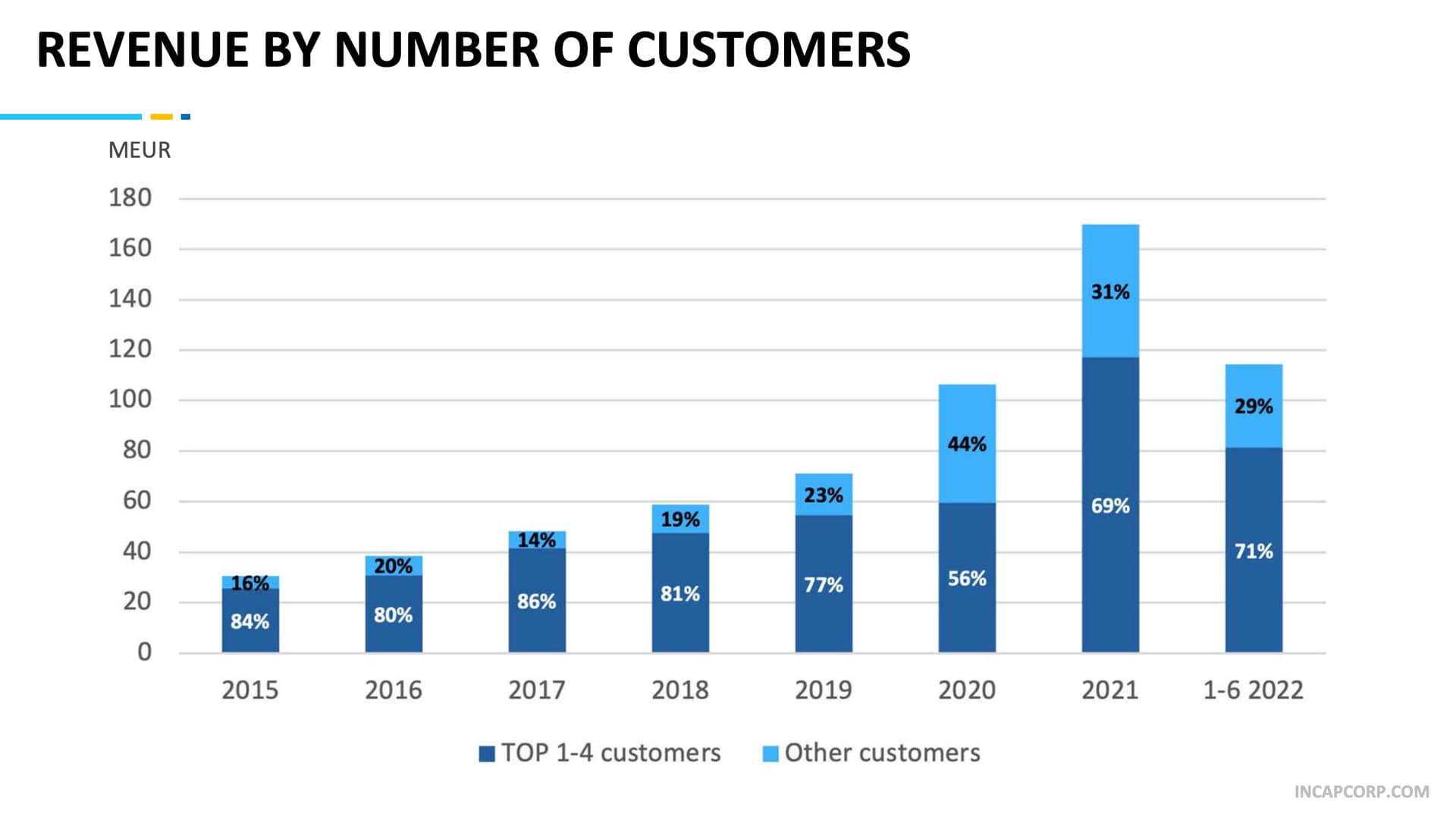

Concentrated customer structure

A concentrated customer structure is typical for the industry. When a customer’s business starts to roll, the share of the contract manufacturer’s business grows rapidly.

Typically the customer relationships are long, even strategic, and the contract manufacturer is not easily changed which is one reason why winning new customers takes time. If I only quote right, CEO Otto Pukk said: "Incap is increasingly integrated in customers’ business processes, e.g. prototyping and product creation.”

Incap have customers from many industries, but a lot of the business is related to green energy and electrical mobility. Its biggest customer is Victron Energy. Incap does not report its customers but the company’s name has come up in several contexts.

Quality is important. Companies do not change EMS-suppliers easily because of price.

Acquisitions

Incap wants to accelerate growth with acquisitions. It is not interested in turnaround companies, the company to be bought should already be in good shape, compatible with the company culture and the purchase price reasonable.

Otto Pukk said that they are targeting geographical expansion in markets with a well-functioning operating environment (e.g., Germany and the USA).

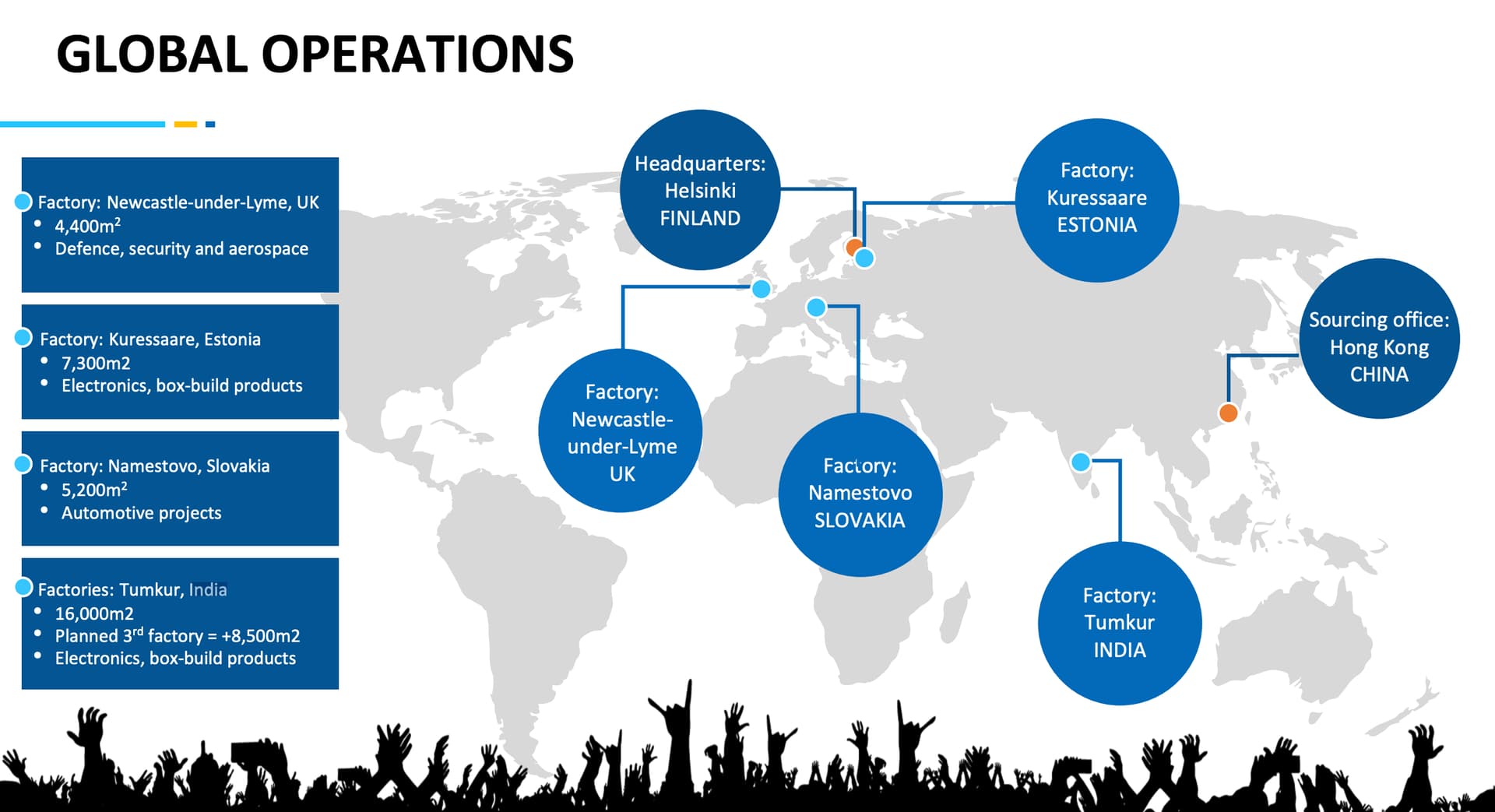

Production plant network

Incap has four manufacturing units located in Estonia, Slovakia, Great Britain, and India which is kind of the heart of the company.

There has been a lot of discussion about the trend of localization. According to Incap it started before the supply chain problems of the pandemic era from the trade war and the pandemic only gave it more boost. For example in the USA, the Made in USA label is even more important. However it is still more talk than action, Pukk said.

Asia’s dominant share is driven by the historically lower cost level of the region than in developed economies. However, the cost dynamic has been shifting over the last decade and have resulted in new production and relocation of old production to more advantageous regions, like India and Vietnam.

Incap has done capacity investments in India and a third factory is will be ready by next year first quarter. It is important to remember that there are opportunities to increase production even without increasing the floor area, e.g. from 2 shifts to 3.

Ramping up production in the EMS industry is relatively straightforward and usually takes from three to six months, once needed machinery and equipment have been received.

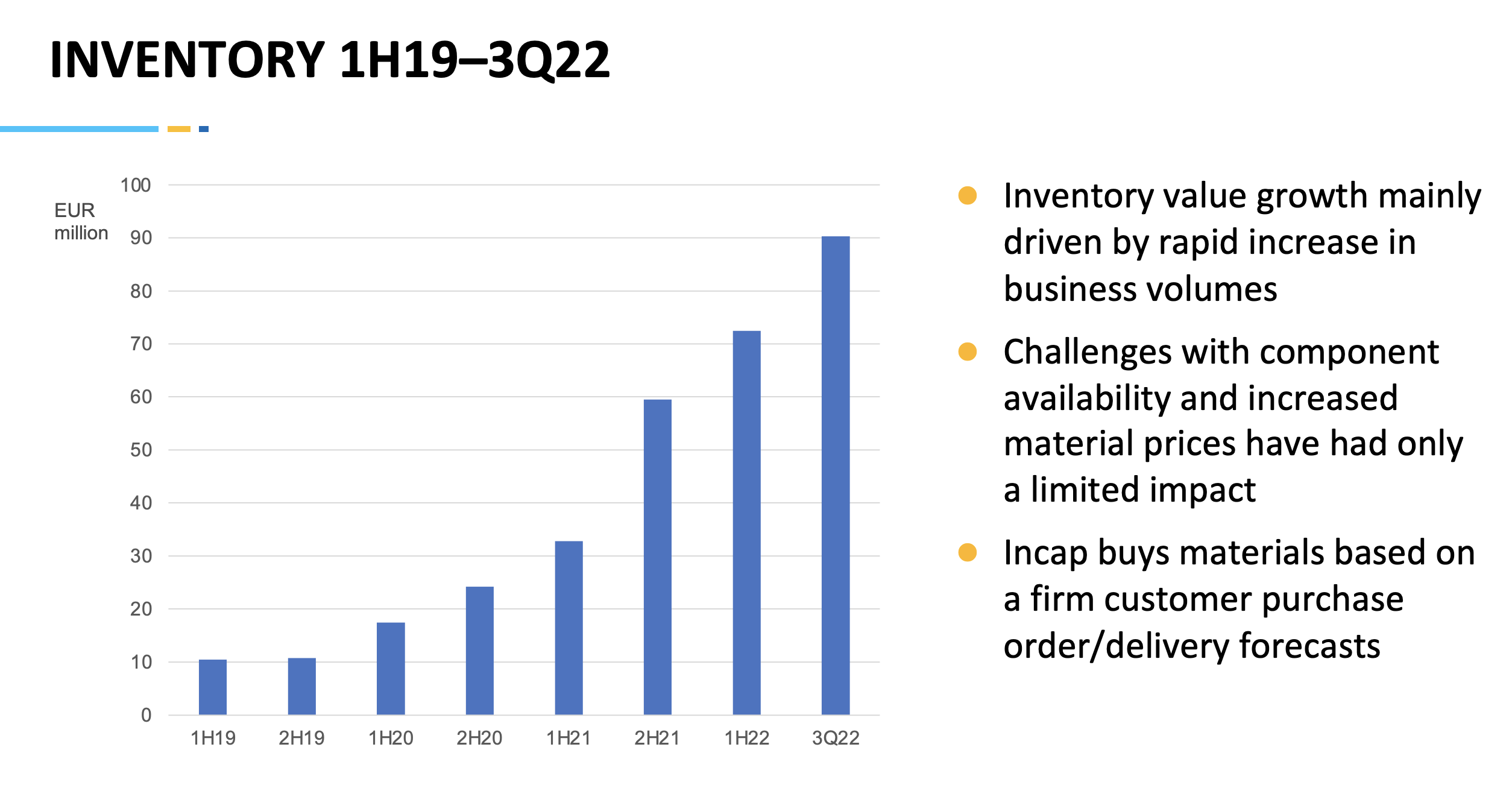

Inventory

Incap’s operations are reasonably working capital intensive and especially during a period of strong organic growth, investments in inventories and thus in its own supply capacity/customer relationships is necessary both from a tactical and strategic perspective.

CFO Antti Pynnönen highlighted that Incap buys materials based on a firm customer purchase order and delivery forecasts. “The materials we have today is the business for tomorrow for Incap.”