Ny intervju med Incaps VD Otto Pukk på svenska

3 gillningar

In this video, we’ll get to know two contract manufacturers.

![]()

1 gillning

Detta borde intressera investerare som är intresserade av kontraktsproducenter. ![]()

1 gillning

Incap’s (and Scanfil’s) Swedish peer Note issued a profit warning related to its FY’23 sales yesterday. The warning is rather mild and it seem to stem from company specific reasons related to new customer ramp ups. At the same time, Note gave also the guidance for FY’23, which indicates slowing growth and slight margin improvement. Note will have also CMD later today ( the link is here) and the company published also a new medium term financial targets for growth and profitability.

Note’s share is down by more than 15% now, so the market got disapointed. The reasons are a bit difficult to assess as there are no estimates at Bloomberg for Note, even though SEB should be covering the company. However, I guess that the net sales warning for this year and the guidance of slower growth for the next years may be the main disappointing themes to the market. In addition, the share price movement is also be affected by the fact that Note has been premium-priced compared to many of its peers recently due its strong track record in growth and profitability.

3 gillningar

Den svenska konkurrenten NOTE släppte sin Q4 denna morgon. ![]() Kan det säga något om marknaden?

Kan det säga något om marknaden?

2 gillningar

Note’s report was well taken in the market as the share is rising by some 8%. There is no information about the forecasts for Q4’23, Q1 or the full year 2024 at Bloomberg even if SEB should cover the share.

Note is counting on some degree of “hockey stick” for H2, although the snapshot still shows no clear signs of improvement in Q1. Naturally that can come true if/when inflation keeps on slowing down and the central bank rate cuts start supporting the economy and investment demand roughly as predicted.

3 gillningar

Incap ended the year 2024 better than I expected: organic growth 15% and 10,4 % adjusted EBIT which are both good. However, the outlook was a bit disappointing, although such a scenario was there. I was hoping that Incap would have get back on the growth track this year, and analysts’ estimates was on that track.

4 gillningar

Q4:a och bokslutskommuniké av Incap i dag. Otto Pukk är både friskspråkig OCH svenskspråkig. I dagens intervju används allt från uttryck som “Dark hours” till “it is what it is”. Att intervjua på per är trist Teams, så jag tänker ta Pukk på orden (dvs på allvar planera resa till lämplig fabrik). Vore väl kul att se :)?

Kolla in dagens intervju här:

2 gillningar

Incap is a high-quality company that HAD significant risks, but perhaps not anymore…

Here is a fresh and high-quality analysis of the company. ![]()

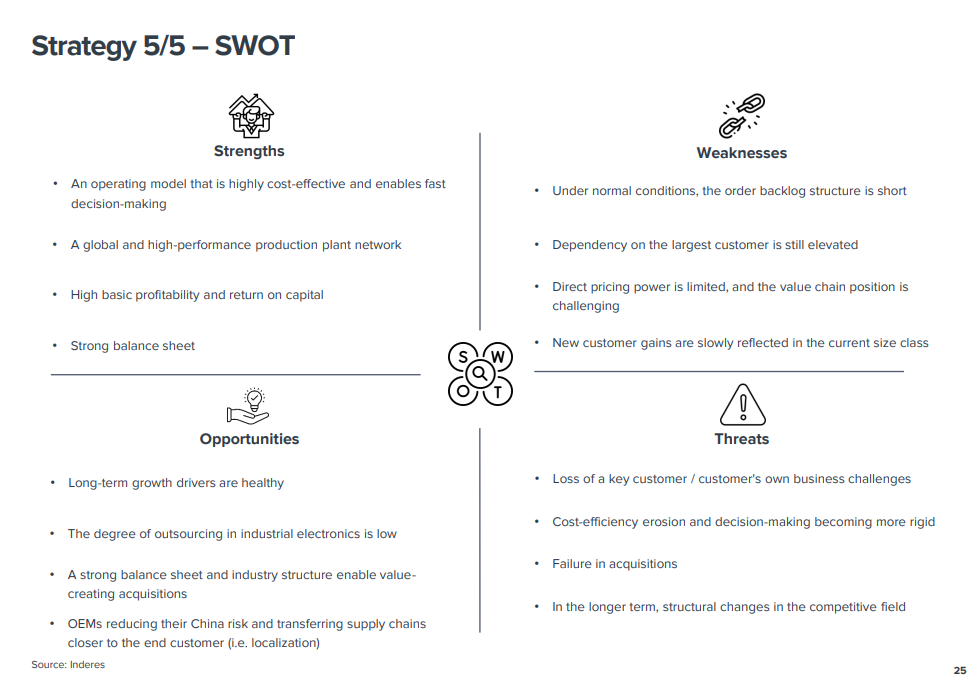

The negative surprise element that we had flagged in our pre-comment on Incap’s outlook materialized and we lowered our forecasts for the company quite significantly, especially for this year. On the other hand, the strong profitability in Q4, the solid cash flow in H2 and the comments on the quarterly turnaround, as well as the decline in the revenue share of the largest customer have, in our view, also removed a fair amount of risk from the stock.

3 gillningar

Incap related Q&A post by the company ![]()

3 gillningar

Spontana tankar kring Q4:an och nuläget:

- Tuff Q4:a, men förhoppningsvis “darkest hours” (för att använda Pukk’s egna ord) bakomlagda.

- Kapaciteten i Indien: bra om det förekommer nyförsäljning vid sidan av den största kunden. En höjning av användningsgraden → bra att den sker på många fronter. Bra med små tecken på att det sker “ramp up” : dvs viss återanställning av personal, även om mkt låga nivåer.

- Drastiska drops i både topline (o övrigt) gällande den största kunden, MEN att ha i åtanke: den övergripande risken med bolaget minskar - att man växer inom alla andra kundsegment positivt.

- Fortfarande lönsamt, med råge, trots enorm påverkan av den största kunden gällande “helhetskakan”.

2 gillningar

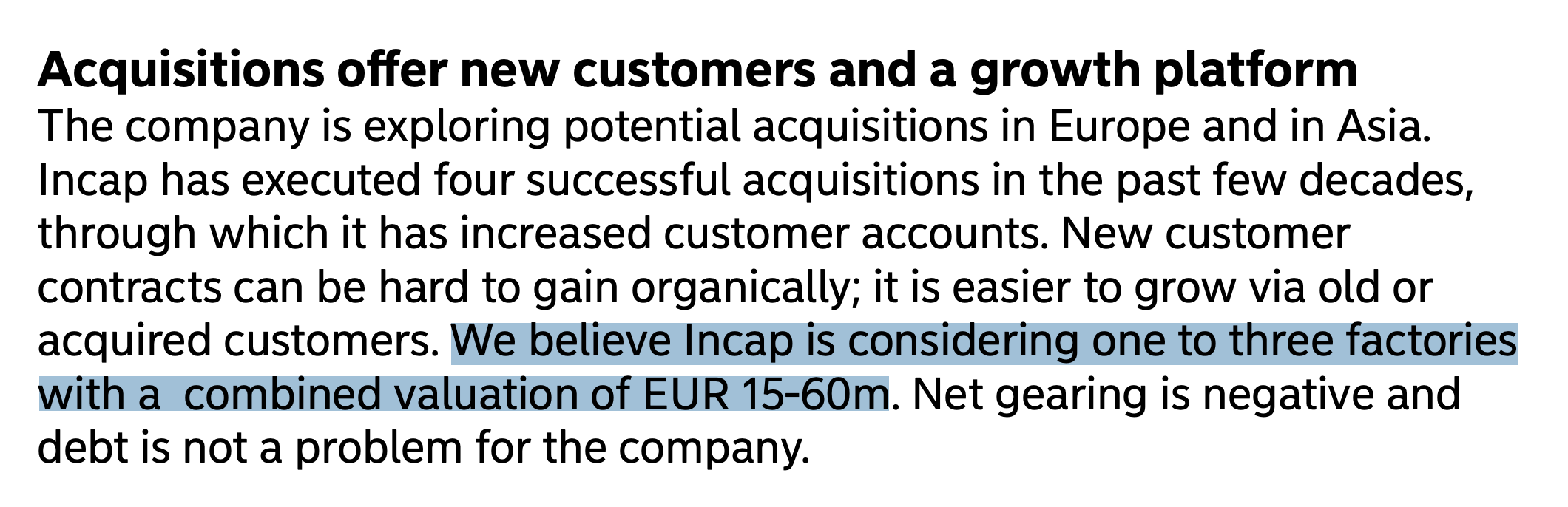

En amerikansk företagsköp har överträffat förväntningarna och kundernas sektorer går bra.

Det finns tillräckligt med kapacitet för tillväxt och det finns också möjligheter för företagsförvärv…

Det går bra för Incap och Pia intervjuade Incaps VD Otto. ![]()

00:00 Start

00:21 Q1:s höjdpunkter

01:11 Organisk tillväxt

01:49 Största kundens lagernivå

03:05 Största kundens försäljningsutsikter

03:42 Allmänna marknadsutsikterna för EMS

04:38 Försiktighet i förväntingarna

05:47 Företagstransaktionsmarknaden i EMS-sektorn

06:43 Är AI en möjlighet eller ett hot för Incap?

1 gillning

Kvalitetsbolaget Incaps början på året gick betydligt bättre än väntat. Detta berodde på att leveranserna från den största kunden återhämtade sig mycket snabbt.

Inderes höjde prognoserna avsevärt för detta år och även för de kommande åren. Bolagets risker har också minskat. Incaps tillväxt- och resultattrend förbättras under andra halvåret.

En positiv resultatvarning är till och med sannolik enligt Inderes.

Här är en mycket omfattande och högkvalitativ analys av Incap. Det är värt att läsa, du kommer inte att hitta en bättre informationskälla någon annanstans. ![]()

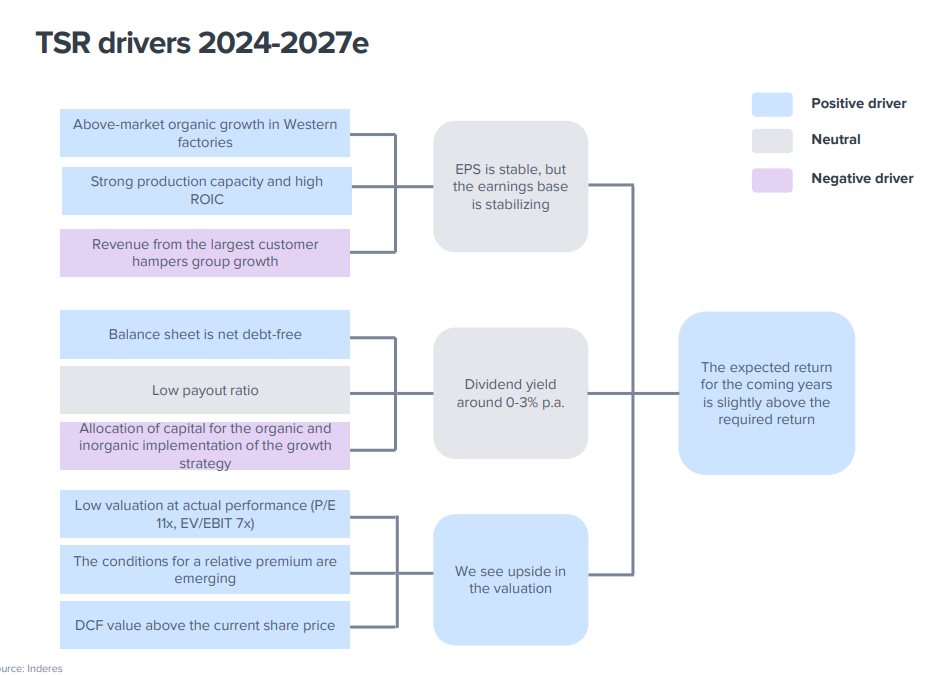

We reiterate our Accumulate recommendation for Incap and raise our target price to EUR 13.50 (was EUR 12.50). Since the rocket-like growth at the start of the decade, the company has faced a pressure test in the past quarters due to the destocking of the largest customer, but we feel Incap is passing the test with flying colors. We estimate that the company’s demand picture is starting to look slightly brighter and expect Incap’s key strength, i.e. cost efficiency, to carry the company also in growth mode. We still find Incap’s valuation reasonable (2025e: EV/EBIT 9x) considering the earnings turnaround budding in H2 and the earnings growth potential of the next few years.

2 gillningar

Hade nöjet att intervjua Incaps VD Otto Pukk om andra kvartalet både på svenska och engelska i dag

3 gillningar

Här är en färsk analys av Incap från Inderes.

Ett intressant företag som jag inte har köpt… än. ![]()

We reiterate our Accumulate recommendation for Incap with a target price of EUR 13.50. Incap’s Q2 developed fully in line with our expectations as the quarterly turnaround progressed, especially with the recovery of deliveries to the largest customer. We did not make any forecast changes after the report. Incap’s earnings trend is turning upward in H2, against which the stock is still moderately priced (2025e: EV/EBIT 8x). Thus, the stock’s expected return is attractive over the one-year and medium-term horizons. Our extensive report on Incap, published in June, is available here.

2 gillningar

Incap släppte sin Q3:a förra veckans fredag, dvs 25 oktober. Det var ett tag sedan jag senaste hade äran att snacka med O.Pukk, så måste helt ärligt inleda med att säga att det var riktigt roligt att “ses”, även om det inte var IRL.

![]() Innan jag går vidare till mina kommentarer ang själva ämnet, dvs rapporten och därtillhörande intervjun, så önskar jag ge två kommentarer på bokstavskombinationen IRL (därav utmärkt i "bold"ad stil ovan.

Innan jag går vidare till mina kommentarer ang själva ämnet, dvs rapporten och därtillhörande intervjun, så önskar jag ge två kommentarer på bokstavskombinationen IRL (därav utmärkt i "bold"ad stil ovan.

-

Jag är, per definition, någon som kidsen (egna inkluderade) kallar för boomer

. Det är fullständigt ok. Jag är trygg i mig själv. Jag brukar glatt svara: tänk vilken tur att din mamma är en boomer! Med det etablerat, (mitt boomertillstånd alltså), vill jag skrika ut: TÄNK - att man kan utföra intervjuer med en person som befinner sig på andra sidan Atlanten (vilket Otto gjorde vid tidpunkten) UTAN att linjen brister 22 gånger, utan att det ekar, och utan att det känns som att den andra skulle sitta på månen… - tvärtom: med denna typ av set-up känns det nästan som om vi skulle sitta i samma rum! Vad vill jag säga med detta (förutom att jag är en boomer och att det , det facto är närmare hundra år sedan jag gjorde TV debut, eller hade mitt första uppdrag som journalist… )? Jo, det jag vill säga är ett stort TACK till all får fantastiska personal och våra superba studios som möjliggör detta!

. Det är fullständigt ok. Jag är trygg i mig själv. Jag brukar glatt svara: tänk vilken tur att din mamma är en boomer! Med det etablerat, (mitt boomertillstånd alltså), vill jag skrika ut: TÄNK - att man kan utföra intervjuer med en person som befinner sig på andra sidan Atlanten (vilket Otto gjorde vid tidpunkten) UTAN att linjen brister 22 gånger, utan att det ekar, och utan att det känns som att den andra skulle sitta på månen… - tvärtom: med denna typ av set-up känns det nästan som om vi skulle sitta i samma rum! Vad vill jag säga med detta (förutom att jag är en boomer och att det , det facto är närmare hundra år sedan jag gjorde TV debut, eller hade mitt första uppdrag som journalist… )? Jo, det jag vill säga är ett stort TACK till all får fantastiska personal och våra superba studios som möjliggör detta! -

Yes: jag är, boomer till trots, en stor vän av “remote” möten via Teams, Slack, eller var det nu kan vara, till exempel diskussioner (eller monologer) som denna via forum. Underbart att det är möjligt

, precis som jag skrev ovan. Vad denna typ av möten (oberoende av syfte) inte, enligt mig, någonsin kan ersätta är det verkliga mötet, IRL. Att utföra en intervju på plats i fabrik är fortfarande mkt högt på önskelistan! Hoppas vi kan få till det i framtiden!

, precis som jag skrev ovan. Vad denna typ av möten (oberoende av syfte) inte, enligt mig, någonsin kan ersätta är det verkliga mötet, IRL. Att utföra en intervju på plats i fabrik är fortfarande mkt högt på önskelistan! Hoppas vi kan få till det i framtiden!

Nu till mina egna tankar efter o inför snacket med Pukk.

- många peers har vinstvarnat: Note o Kitron i sept. Scanfil tidigare, redan i somras, men kom därefter m. förvärvsnyheter. Hanzas VD har varit ute o lovat i pressen att de INTE kommer att vinstvarna o släppte en riktigt stark rapport i tisdags. Incap däremot verkar ha tagit smällen något tidigare, och som Pukk sade " ifjol var vi slagpåsen". Nu har läget vänt - dvs Incap är, som rubriken antyder, tillbaka i tillväxtspåret.

- Det är inte bara tillväxt, utan även det som Pukk sade vid något tillfälle “the darkest hour is behind us” - utan lite av ett nytt Incap som man i slutet av 2023 - början av 2024 kunde ana, men nu verkar ta form. Dvs då m syftning på den största kundens ställning, som numera minskar i takt med att den övriga kundpaletten utökas.

- Den största kunden, icke att förglömma, visar fortfarande tillväxt på sikt, men inte i samma takt som innan, Här bör man även komma i håg marknadens snedvridning, iom läget, så som Pukk även beskriver det var prekärt. Att den största kunden i slutänden satt på alltför stora lager var svårt att se mitt under pågående komponetskris o allt annat kaos som rådde.

- Att man utfört denna “de-stocking excersice” vad skall man säga på sve: lagerkonsolidering (?) , samtidigt som man framgångsrikt integrerar förvärv o - ja, stryr kosan mot tillväxt inom andra områden säger något… förutsatt att detta spår upprätthålls dvs.

- Gillar även inställningen "det är alltid kris någonstans i världen (eller hur Pukk uttryckte sig) , men Incap kan ta vad än som kommer. Återstår naturligtvis alltid att se, men personligen gillar jag attityden. Man kan ALLTID skylla på omvärldsfaktorer, regnet, eller till och med att gräset växer åt fel håll då man inte lyckas göra mål på fotbollsplan. Till syvende och sist lever vi alla i samma värld - där vi alla (med syftning på allt från kattungar, människor, småfirmor, listade bolag, till länder, nationer och unioner) reder ut våra egna problem (mindre eller större) i tur och ordning. Den som ger sig in i den “leken” med offerkoftan på, är sällan den som kommer ut på andra sidan iklädd ledartröja.

- Om lager: detta är något som stört mig enormt: hur skall man, som investerare tolka “lager” i rapporten. Är det en indikation på kommande försäljning, eller något helt annat. Även här ger Pukk ett ärligt svar.

För tydlighetens skull: äger personligen inga aktier i Incap. Inte de som kallar mig boomer heller.

IH

Direktlänk till intervju på svenska:

Incap Q3’24: slagpåsen gör comeback i tillväxtracet - Inderes

För den som hellre lyssnar på ENG:

Incap Q3’24: Kasvu jatkuu (eng.)

För den som missat analysen - LÄS den (!) @antti.viljakainen s text är mkt kvalitativ, till skillnad från mina egna funderingar på temat. Ni glömmer väl inte att han även svarar på frågor ![]() !

!

2 gillningar

Isa intervjuade analytikern Antti Viljakainen från Incap. ![]()

The portfolio managers of Inderes’ very own stock portfolio, aka “the model portfolio” (YES: it is a real money equity portfolio that invests in Finnish equities. It was launched back in 2011 with 50 000 euros, the rest is history…) decided to open a position in Incap. The decision-making process behind this transaction certainly needs a video of its own, but that is another story. Until then: Head of research Antti Viljakainen gives his current view of Incap and why the recommendation is BUY!

Content:

00:00 Intro

00:05 Buy recommendation and Inderes Model Portfolio’s Incap purchase

01:46 Share of the biggest customer

03:19 Visibility in the market

05:01 Inventory levels

06:43 M&As

08:31 Q3 summarized

Subscribe to the Inderes Nordic YouTube channel.

Här är färska tankar om Incap. ![]()

Incaps företagsförvärv i USA har visat sig överträffa förväntningarna, och marknaden erbjuder fortfarande fler möjligheter till expansion. Detta kan vara strategiskt klokt med tanke på förändringar i importtullar och den växande lokala efterfrågan. Samtidigt har företaget haft stor framgång med sina fabriker i Indien, trots att affärsverksamheten där är utmanande. Många konkurrenter har stött på svårigheter, men Incap har dragit nytta av sin skickliga personal och sin optimala produktionsmodell. Lönenivån i Indien stiger dock, vilket påverkar landets konkurrenskraft som tillverkningsplats.

Miljöansvarspriset till de indiska fabrikerna understryker företagets engagemang för hållbar utveckling. Denna utmärkelse omfattar energieffektiva processer och användning av förnybara energilösningar. Expansionen i Indien, inklusive en tredje fabrik som öppnades 2023, möter den ökande efterfrågan och stärker Incaps position som leverantör av högkvalitativa tjänster inom elektronikindustrin.