We initiated coverage of Hexagon, one of the leading digital twin companies globally. In big picture it has made an impressive transformation from a low-value-add industrial conglomerate in the late 90s into a global high-tech large cap nowadays. Recurring revenue’s share is already almost around 40 % as the M&A focus has been on software.

Hexagon’s organic growth has been at very good level of 8% this year despite the macroeconomic slowdown and partial dependence on hardware sales to cyclical sectors like construction and manufacturing. We have assumed the organic growth to slow-down in 2024-25 to 5% that is also in line with Hexagon’s historical organic growth (average of both past 5 and 10 years). The profitability continues to improve driven by sales mix (software and new hardware innovations grow faster). Improving gross margins together with moderate growth in fixed costs should help the company to grow their adjusted EBIT by some 8% annually in 2024-25. The rationalisation programme kicked off in 2023 (target 160-170 MEUR savings by 2025) should restrain fixed costs growth even if global salary inflation continues and depreciations increase.

We initiated coverage with Reduce recommendation because we are slightly more cautious on earnings growth compared to consensus and see a risk of moderating demand. We find current valuation (2024e) with ~10% discount on historical levels to be rather fair given the increased interest rates in the market. Also other peers with hardware sales and cyclical market exposures are currently trading below their long-term levels.

Här kommer tråden vi la ut på twitter angående just Hexagon. Länk till inlägget

Twitter-TRÅD angående #Hexagon. Vi har initierat en bevakning på Hexagon som är ett globalt diversifierat teknikföretag som bygger på en rad förvärv och som tillhandahåller produktivitetsförbättrande lösningar till flera olika branscher.

Hexagons nettoomsättning uppgick till 5,2 miljarder EUR 2022 med en justerad rörelsemarginal på 29%. Företagsstrukturen består av två affärsområden, Geospatial Enterprise Solutions (GES) och Industrial Enterprise Solutions (IES).

Hexagon erbjuder högkvalitativ hårdvara för sensorer, mätning och positionering genom båda sina affärsområden.

Här nedan kan vi läsa av att de två affärsområdena är nästan identiska vad gäller storlek och lönsamhet.

Ett moget och diversifierat företag med hög lönsamhet och goda tillväxtutsikter.

Över en tredjedel av försäljningen är återkommande intäkter.

Det höga operativa kassaflödet är tillräckligt för att finansiera investeringar i organisk tillväxt eller medelstora förvärv.

Marknaden för Hexagon är global och omfattar olika produktsegment. Dessa faktorer gör den adresserbara marknaden ganska diversifierad och flerdimensionell. De rådande ekonomiska förhållandena påverkar särskilt hårdvaruförsäljningen genom kundernas investeringsvilja.

Vi anser att Hexagons finansiella mål är ganska rimliga, det är ett möjligt scenario att nå tillväxt- och lönsamhetsmålen på medellång sikt. Hexagon siktar på en årlig genomsnittlig försäljningstillväxt på 8-12% under 2022-26, varav 5-7% organiskt och 3-5% via förvärv.

Hexagon är ett mycket lönsamt teknikföretag med stabila utsikter för organisk tillväxt. Även om de makroekonomiska förhållandena inte är gynnsamma förväntar vi oss att Hexagon fortsätter att förbättra sitt resultat under 2024-25.

Vi förväntar oss dock att den organiska tillväxten kommer att vända under de kommande åren och inleder bevakning med rekommendationen REDUCE och riktkursen 102 SEK.

The Capital Markets Day is being hosted by Hexagon on Thursday, December 7. The company is expected to have its growth opportunities showcased and demonstrated in both business areas.

https://www.youtube.com/watch?v=MvyFWMllqzY&t=581s This was a very interesting interview with Fraser Perring from Viceroy Research. There was a lot of talk about Hexagon, and their short report about the company claiming that they are comitting fraud by not reporting correct revenues. Viceroy has recently been correct with exposing SBB, so I am interested to hear from Inderes analyst @pauli.lohi_124524 what you think about the short report?

I have not read the report myself but Bard summarizes it as following: In July 2023, Viceroy Research published a report titled “Hexagon AB - Six Sides to Every Story,” alleging that Hexagon AB, a Swedish multinational technology company, had committed fraud. The report accused Hexagon of engaging in a number of questionable practices, including:

Aggressive acquisition strategy: Viceroy claimed that Hexagon had been pursuing an aggressive acquisition strategy, acquiring companies at inflated prices and artificially inflating its earnings.

Lack of transparency: The report also criticized Hexagon for its lack of transparency, arguing that the company had failed to provide adequate disclosures about its financial performance and business operations.

Front-running: Viceroy alleged that Greenbridge, the investment company of Hexagon’s CEO, had engaged in front-running, using its knowledge of Hexagon’s acquisition plans to profit from insider trading.

I’m writing my own views on the three topics you listed above.

Aggressive acquisition strategy: I find Hexagon’s M&A strategy successful in general. For our extensive report, we did a analysis of post-synergy valuations of their acquisitions in the past 10 years (2013-22). We compared the money they spent in these acquisitions (net purchase price or EV) to the increase in adjusted EBIT between 2012 and 2022. We of course don’t know how much of their EBIT growth was due to organic improvement and how much due to the acquisitions so we have to assume certain organic EBIT growth rate. If we assume their organic EBIT growth during this period has been 5%, it would assume that the post-synergy EV/EBIT for the acquisitions has been around 10x. Or if their organic EBIT growth had been 8%, the post-synergy EV/EBIT would be around 16x. This approach does not include likely future synergies from the recent acquisitions of EAM and ETQ, which, if taken into account, would result in lower post-synergy multiples for the past acquisitions. We consider that even an EV/EBIT of 16x would be a fair-to-attractive historical multiple for business growing organically some 5% per year (probably even more as the acquired software businesses grow faster than the group on average) and having high return on new invested capital.

Hexagon group’s accounting policies obviously differ from the policies of the companies it acquires which may cause short-term inconsistencies in group figures. For example, the company activates R&D as capex but many companies it has bought recently (e.g. ETQ and EAM) have not done so in the past. So activating new R&D but not having any old intangibles to depreciate naturally boosts EBIT in the short-term. I don’t see anything wrong with it but investor needs to understand it. For my experience, the company has been open about its policies. I can’t judge every single acquisition the company has made or related accounting policies, but in general they seem fine to me.

Lack of transparency:

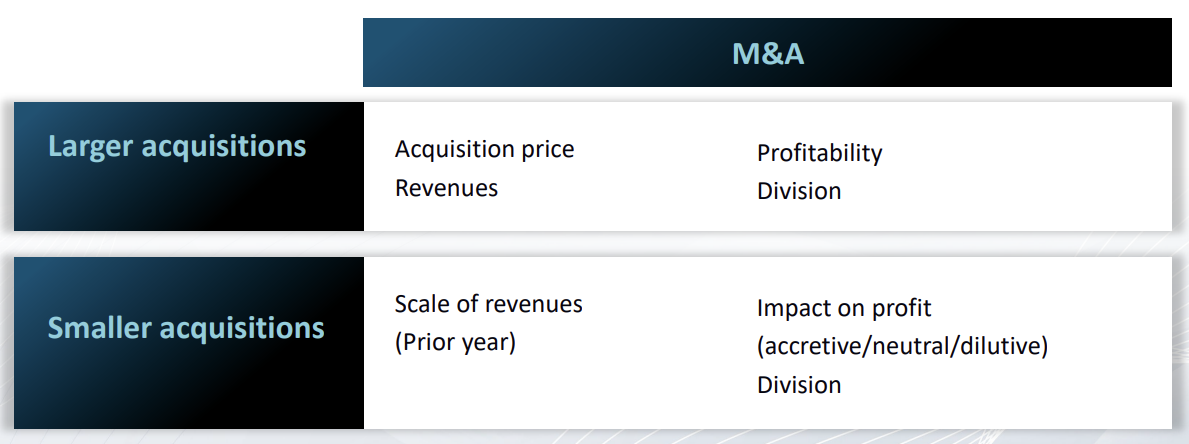

I agree that the company’s disclosure of small acquisitions has been rather scarce in the past. They have given more information about the bigger deals though. In the CMD of 7th December they announced new disclosure policy. In the future this is what they will disclose about M&A. From analyst’s perspective, I find this new policy sufficient.

Front-running: I don’t have any 100% proof evidence from an independent source which version of that story is true. Viceroy claims that Greendbridge front-run Hexagon. Hexagon claims that they invested first and Greenbridge later. Anyway, Hexagon and Greenbridge have agreed to not invest into same companies anymore in the future.

In big picture, I think that Hexagon has not managed its corporate governance perfectly in the past (board composition and Divergent deal at least may look suspicious for an outsider). I guess this negligence might have something to do with company’s success in generating value to all shareholders that has reduced the pressure for change. As the company has grown, the required corporate governance standards have become higher. However, after the negative publicity during summer 2023, they have taken action and I find the proposed measures satisfactory.

Hexagon meddelade på tisdagen att man har kommit överens om att sälja en affärsverksamhet för industriella mätinstrument till ett kinesiskt företag. Förväntad påverkan på företagets EBIT och kassa är mycket liten.

Hexagon launches reality capture based solution to analyse and monitor rainforests. This is a nice example how reality capture and geospational software tools can be used for new different purposes. Rainforest conservation could become a big business in the long-term and this kind of tools could make it more efficient and transparent.

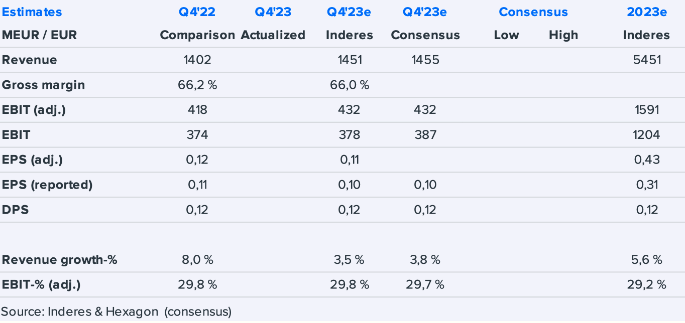

Omsättningstillväxten låg under förväntningarna på grund av en svag byggmarknad. Lönsamheten överträffade förväntningarna tack vare en stark bruttomarginal.

Hexagon released its Q4 results today. Revenue growth was slightly below expectations due to cyclical factors such as the weak construction market. However, profitability exceeded expectations, driven by strong gross margin. We don’t expect major changes to consensus EBIT estimates for 2024-25 based on the Q4 report, although the company may provide more information on the business outlook in the earnings call later today (10am CET).

Hexagon är fortsatt aktiva med förvärv. Man offentliggjorde igår förvärvet av Xwatch Safety Solutions. Xwatch tillhandahåller hård- och mjukvara för maskinstyrning utformade för förbättrade säkerhetsprotokoll på byggarbetsplatser.

Samtidigt släpper man sin Q1 rapport på måndag. Vi förväntar oss att intäkterna ökar måttligt och att lönsamheten förbättras, drivet av förbättrad försäljningsmix och operativ effektivitet.

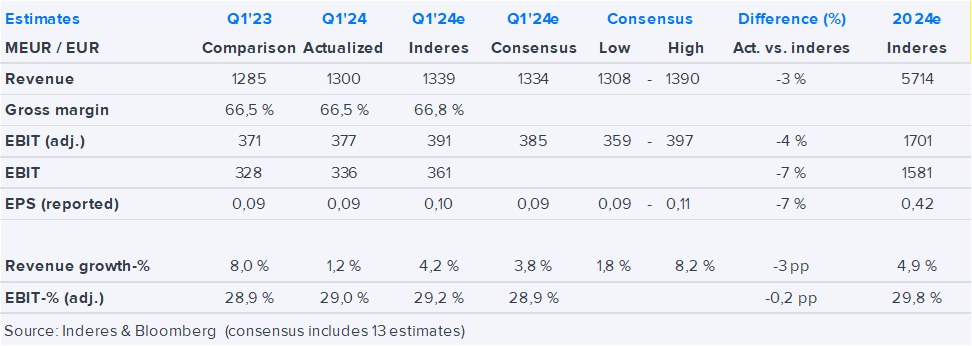

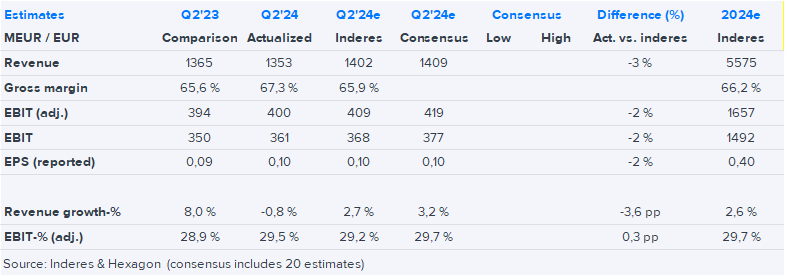

Net sales came 3 % below our and consensus estimate

Adjusted EBIT was 4 % below our estimate. Reported EBIT and EPS were 7 % below our estimate.

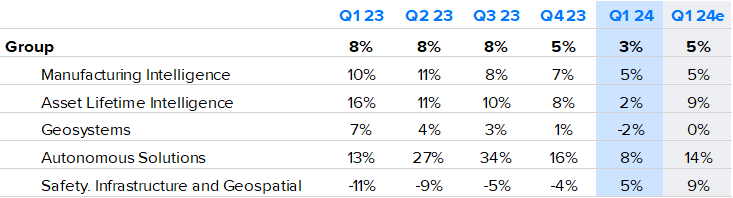

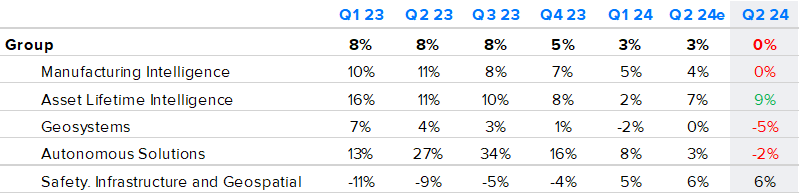

Weakness in organic sales growth was rather broad-based. Only Manufacturing Intelligence reached the estimated level of growth. All other divisions grew less than we expected.

Q2 growth ended up weaker than we expected, which was also reflected in earnings, even if the relative profitability was rather strong. Sales came in 3% below our estimate and 4% below consensus. Adjusted EBIT was 2% below our estimate and 4.5% below consensus.

Here you can find the division-specific organic sales growth figures (y/y).

Large segments with material hardware sales, such as Manufacturing Intelligence and Geosystems, suffered due to cyclical headwinds in their certain important end-markets (automotive for MI and construction for Geosystems). However, recurring revenues, including software and services, grew by 8% year-over-year, indicating an improvement in the quality of revenue as expected. The gross margin reached an all-time high, and operational efficiency measures helped maintain the EBIT margin at a good level. This development signals good potential for earnings growth once the cyclical industries recover.