Jag måste säga att jag tycker att Inderes erbjuder den bästa aktieanalysen som finns. Här finns en mycket omfattande och högkvalitativ rapport om det här företaget, och den är dessutom gratis.

We are a family of brands, driven by our desire to make great design available to everyone in a sustainable way. Together we offer fashion, design and services, that enable people to be inspired and to express their own personal style, making it easier to live in a more circular way.

Så… analysen nästan glömdes bort. Här är en utmärkt analys av detta företag, enligt min åsikt hittar du inte en bättre analys någon annanstans.

We believe H&M is on an improving margin trend and will get close to its 10% margin target in 2024, driving a substantial earnings growth y/y during 2023-24. We see solid growth potential for this globally strong fashion brand.

Här är en ny, bra och gratis analys av Hennes & Mauritz.

H&M’s Q4 sales development was slightly behind our forecast, leading to minor estimate cuts. The share has performed well since our initiation and the multiples have corrected to quite fair levels in our view (P/E 19x for 2024).

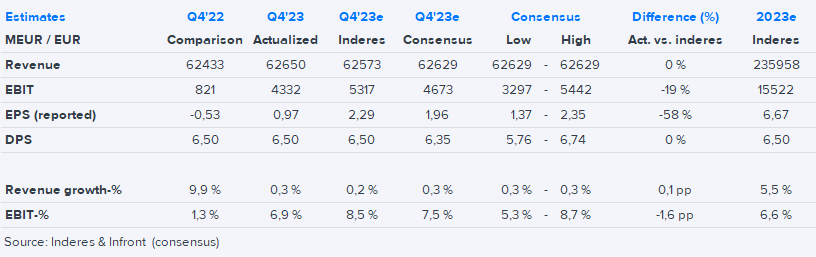

H&M reported its Q4 this morning. With sales reported earlier, the focus is on margins. On that front, gross margin was strong at 53.7 %, up almost 4%-points y/y, but fixed costs were higher than we expected and hence EBIT fell short of our and slightly also vs. consensus. Dividend was maintained at 6.50 SEK as widely expected and the company still has the “ambition” to reach 10 % EBIT margin this year, although this is not a guidance. Dec-Jan sales are down 4 % in local currencies, which looks like a weaker than expected start for the year.

Company also announced a change of CEO as Helena Helmersson is stepping down and Daniel Erver, currently head of H&M-chain, is appointed as CEO. Erver has been in the company for 18 years are will continue to lead the main brand H&M. We see this as a very smooth-looking transition to a solid internal candidate.

Styrelsen för H & M Hennes & Mauritz AB har idag utsett Daniel Ervér, ansvarig för varumärket H&M, till ny vd och koncernchef för H&M-gruppen. Han efterträder Helena Helmersson som har beslutat sig för att lämna vd-rollen och H&M-gruppen.

Daniel Ervér, född 1981, har arbetat inom H&M-gruppen i 18 år i olika roller inom flera delar av verksamheten, nu senast som ansvarig för H&M som är det största varumärket inom H&M-gruppen. Daniel, som tillträder som vd idag, kommer även fortsättningsvis att operativt ansvara för H&M vilket innebär att ingen efterträdare till Daniel som ansvarig för H&M utses.

Här är en färsk, gratis och högkvalitativ analys av H&M.

H&M’s Q4 earnings fell short of expectations and also fiscal 2024 seems to be off to a soft start. This pushed our EBIT estimates down 8% and 1% for 2024-25 respectively.

H&M closest peer Inditex reported their Q423 today (which is Nov-Jan, actually closer to H&M Q124 period, which is Dec-Feb) - H&M reports Q1 report ahead of Easter on 27.3. (EDIT: no separate sales report published anymore and Q1 report date moved to 27.3. from 28.3.)

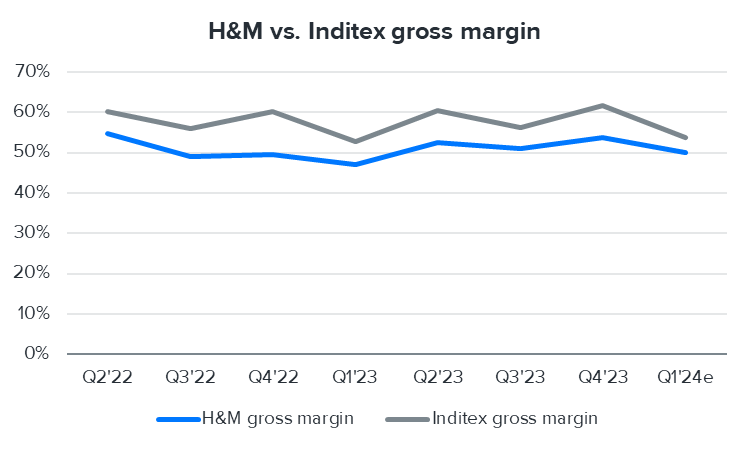

Inditex has been performing better than H&M in terms of growth and profitability for years and continues on that path. Inditex grew close to 10 % in the quarter with an EBIT margin of 16 %, both well above H&M’s expected levels. Hence, we believe perhaps the most usual comparison is to look at the gross margin, where Inditex is also ahead of H&M, but there’s clearly a similar seasonal pattern. As you can see from the graph below, we expect H&M to perform relatively better than Inditex (ie. improve more from comparison period), but still be at a lower level.

On the outlook Inditex says that February-early March sales are off to good start with over 10 % growth. For gross margin, it sees a stable outlook for FY24. We are expecting a slight improvement in H&M gross margin for the similar period, but that’s still below Inditex’s level.

Overall Inditex’s report suggests that H&M should have room to improve their performance as there’s no clear headwinds in the industry, given Inditex’s good performance and outlook.

Sure. H&M uses this to refer to a wide range of factors that impact the gross margin (or cost of goods sold), which include eg. logistics costs, the cost of the actual product for H&M (which are outsourced) and impact of currencies to profitability (mostly USD as goods are purchased in USD). The product cost in turn is impacted by eg. labour cost, price of cotton (and other raw materials to a smaller extent). Recently these costs have been going down and hence the “external factors” are positive compared to last year as H&M is commenting.

Then there’s also “internal factors” (although H&M doesn use this term), which mostly means pricing. Here H&M typically gives comments regarding the impact of markdowns to the gross margin, but obviously also the list prices evolve continuously, typically following the development of “external factors” as H&M wants to keep prices competitive.

Yes, these external factors are typically things impacting the whole industry and it has been there for a few quarters already. For this year the outlook is still supportive in this respect, but one should also bear in mind the pricing component, where H&M has said prices will go down during this year, which obviously mitigates the margin support from lower costs.

Företaget publicerar sin Q2-rapport på torsdag och här är analytikerns kommentarer relaterade till den.

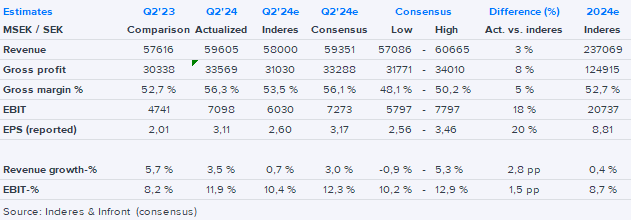

H&M will report its Q2’24 (March-May) results on Thursday at 8:00 am CET. We expect revenue to be flattish in local currencies, but EBIT to improve clearly, supported by both gross margin improvement and lower opex. The company has said its targeting 10% EBIT margin in 2024, which looks optimistic to us as we expect only 7.9%, while the consensus is at 8.9%.

H&M Q2 out this morning. Q2 figures were clearly above our estimates with 3 % growth and a sharp increase in gross margin, however, they were well in line with the consensus.

For June, company sees a 6 % decline in sales, which is obviously weak, and which the company attributes to tough comparisons and weather effects. Company reiterated its goal to reach 10 % EBIT margin this year, but added that it has become more challenging due to “external factors” ie. input costs, have become more negative in H2 than previously believed.

It’s not a surprise that 10 % will not be reached this year as we have been around 8,5 % and consensus around 9 %, but comments regarding the future still look to be on the negative side in our view, even if we need to hike our 2024 estimates due to better than expected Q2.

We also note that opex/sales ratio is not coming down much despite full effect of the restructuring efforts, leaving the improvement to be driven only by gross margin. We believe some of the gross margin strenght might be used to lower prices and hence drive sales going forward.

: what about valuation?")