Riktigt fint att se att även under besvärliga rådande makro-omständigheter så förbättrar Consti både det relativa och det absoluta rörelseresultatet! Jag har ägt bolagets aktier redan på den tiden då resultatet var dåligt även i goda tider, så det har skett en rejäl förändring i rätt riktning de senaste åren. Jag ökade ännu en gång min position direkt vid öppningen; jag tycker att priset var mycket rimligt, 9,12€.

”Liikevaihto kasvoi alkuvuotta nopeammin ja kannattavuus jopa parantui vertailukauteen nähden vaikeassa markkinassa, mitä voi pitää hyvänä suorituksena.”

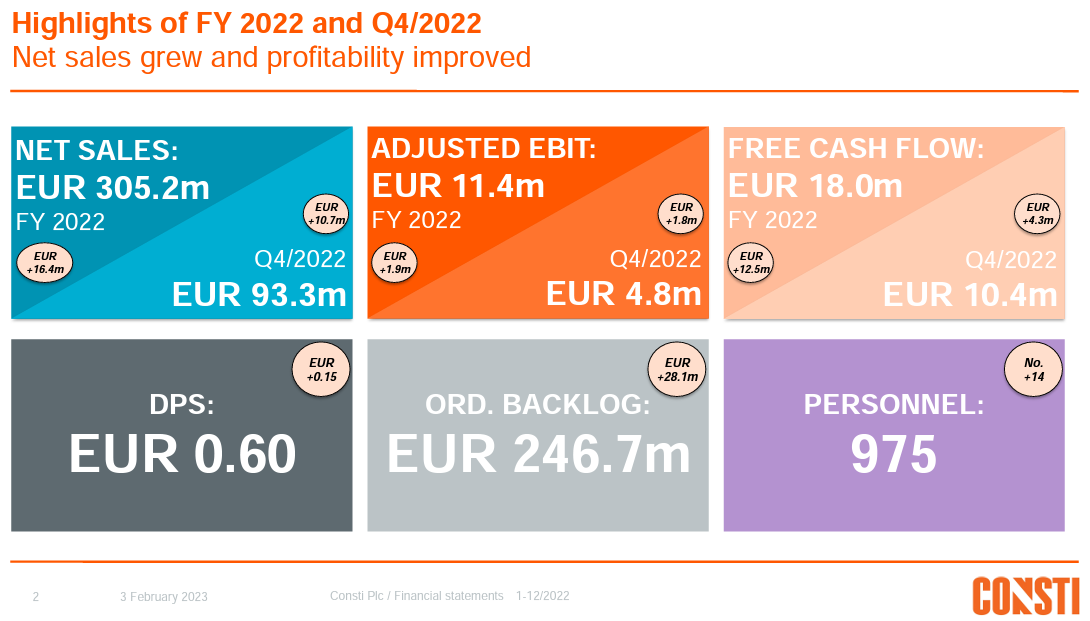

Consti performed very well during Q3 and has done so all the year 2022. Seems that Consti can manage to keep its profitability on a stable level even during exceptionally uncertain and difficult market environment. What is good to see that the order book has remained solid and revenue has been growing also. Next year is of course a little bit of a question mark considering the market environment but we see that renovation has capabilities to withstand poorer conditions on the economy far better than new-building construction. Considering that the valuation is very low in our opinion we see great upside the stock.

Evli ökar riktpriset till 12.00 EUR och behåller Köp-rekommendationen.

Evlis prognos är på det stora hela i linje med Ollis / Inderes. Evli tror dock på högre dividendutdelning: 2022 0.49€, 2023 0.56€ och 2024 0.61€. Motsvarande från Inderes: 0.47€, 0.50€ och 0.55€.

Oberoende vem man väljer att lyssna på, så tycker jag själv att Consti erbjuder en för H:fors-börsen ganska unik kombination av relativt hög direktavkastning, fint stigande dividend, moderat tillväxt, stigande lönsamhet och låg värdering (P/E ~10x). Kommer Consti att bli nästa Apple? Garanterat inte, men här borde finnas alla möjlighet att slå index och med en ganska moderat risk. Branschen i sig är inte speciellt konjunkturkänslig (byggnader är alltid i behov av underhåll, och att skjuta upp underhållet kan i förlängningen ofta bli dyrare för kunden) och Consti verkar har lyckats med att reda ut sina egna, interna problem.

Jag har av princip valt att bojkotta byggbranschen (bränt fingrarna ett par gånger), men jag intalar mig själv att Consti inte är ett byggföretag per se. Snarare kan Consti tänkas gynnas i för byggföretagen dåliga tider, dvs. då fokus skiftas från nybyggnation till underhåll.

Så summa summarum: tråkig bransch, fragmenterad marknad, bolag med någorlunda tillväxt och stigande lönsamhetstrend, bra direktavkastning som även den är i stigande trend, låg värdering → my kind of company!

@olli.koponen : do you see a potential shift of Consti’s dividend policy? You’ve forecasted DPS 2024e 0.55€ and now we indeed already reached DPS 2022 0,60€.

@olli.koponen : I see in today’s report that you are positive as well, but still remain slightly cautious. Given that Consti has substantially beaten your estimates multiple quarters now, I wonder what will it take for Consti to get your “Buy” recommendation?

Can not comment on that Buy-recommendation but yes still some uncertainties remain. But it is looking quite good and this is a good start for the year.

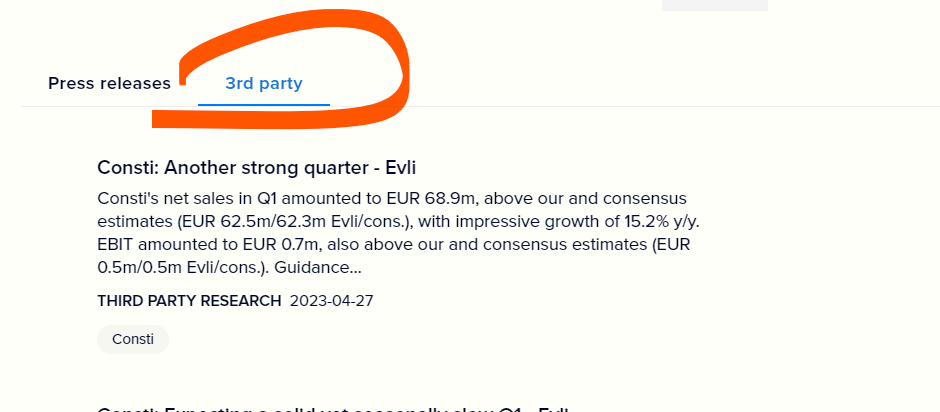

Hej, bara som mellankommentar ang Consti. I vissa fall har vi tillgång till 3rd party analys från andra andra analyshus i vår tjänst (har skrivit om detta tidigare ang ngt annat bolag). I Constis fall verkar det finnas flera tillgängliga rapporter på ENG.

Vi kan inte ta ställning till tredje parts utlåtanden, men som infokanala för den som vill läsa är det alltid ett alternativ iom att infon finns tillgänglig

Is this too broad of a question, perhaps, but a shorter answer would suffice for me.

Does the energy efficiency trend have a significant impact on Consti in the long term? Or is this trend just one small factor in a larger context?

Of course, energy efficiency has always been considered, but I’m just wondering if the energy efficiency trend has somehow risen particularly in recent times.

I will let @olli.koponen give the in-depth answer, but just to open the discussion, Consti has indeed increased its focus on energy efficiency / sustainability solutions. To what extent these initiatives are paying off is beyond me though. A couple of examples: Consti Optimi and Eco Consti.

Looking at the initiatives and incentives from the Finnish government (ARA etc.), it should be a highly interesting market.

You made some interesting points and brought up some things that I didn’t actually know. Now I might also know where to search for more information with the help of Google.

I dare to ask these kinds of questions because I think that the answers can bring joy to others as well, not just me.

I think that will be one of the biggest benefactoring megatrends for Consti and renovation market as a whole for the coming years. In Finland (and I assume in Nordics aswell) we have founded apartments massively during 1950s-60s-70s that are coming in to the roughly 50 year lifespan renovation age. That means we have a lot of work to do if we seek to keep our buildings safe and sound.

As there is a underlying need to renovate buildings, they might aswell make the building more energy efficient. With that comes for example Consti Optimi which @Dividendseglaren nicely mentioned here above. But Optimi might be a high end solution or step that takes your energy efficiency to a whole new level. Even just renovating or upgrading your insulation, pipes, air conditioning, automating lights, automating ventilation, monitoring building’s flows (water, air, electricity) with digital solutions can drastically improve energyefficiency. That trend is very supportive now for renovation market as ppl are more focused on that and the legislation is pushing building companies and property owners to be more energy efficient.

Thank you also Olli for your comprehensive answer! I now understand the whole better, there were many things that came up that I wouldn’t have thought of myself.