Wärtsilä har haft stor framgång, men hur ser framtiden ut?

Nedan finns en utmärkt analys av detta intressanta företag. ![]()

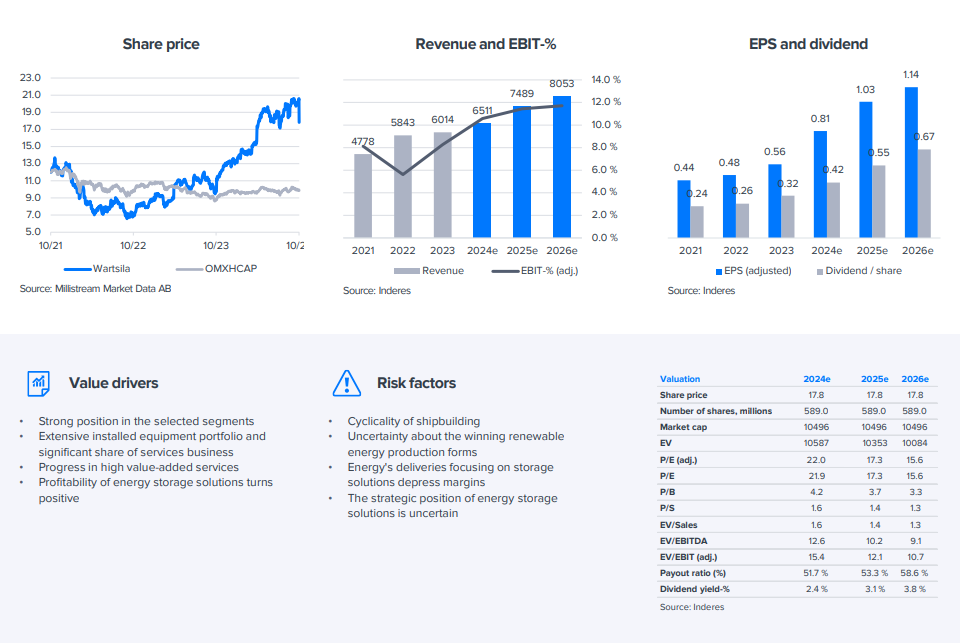

Wärtsilä’s Q3 order intake was below expectations, mainly due to Energy, but profitability was better than forecast, also due to Energy. The company’s demand outlook remains strong. Thanks to the solid performance in storage and Portfolio Business, we have significantly raised our margin forecasts for the group. After the share price decline we have seen and the upgrades to our earnings forecasts, the stock is once again attractively valued on multiple metrics. We raise our recommendation back to Accumulate and, following our forecast changes, increase our target price to EUR 19.50 (was EUR 18.00).