Tecnotree has generated a lot of discussion among Finnish retail investors, so I created a dedicated thread for this.

Tecnotree är verksamt inom IT-sektorn. Bolaget är specialiserat inom utveckling av digitala kommunikationslösningar. Tjänsterna används huvudsakligen bland bolagets små- och medelstora företagskunder och innefattar exempelvis affärsanalys, marknadsföring, samt utveckling av digitala marknadsplatser. Verksamhet innehas på global nivå, med störst närvaro runtom den nordiska marknaden.

Tecnotree’s Q2 report came in below our estimate for net sales, but above for earnings. The company reiterated its guidance, but the uncertain operating environment is reflected in the company’s order flow as customers postpone their investments to some extent. In the coming years, a critical part of Tecnotree’s investment story will be how the company allocates the capital raised through convertible bonds, which it intends to allocate to M&A and product development, among other things. The risks of the stock are high, but at the current valuation the risk/reward ratio turns marginally positive in our view.

Greetings everyone! Thank you @börsen84 for creating the thread. I follow Tecnotree as an analyst and I’m happy to help if you have any questions regarding the company. Here is a link to our extensive report from last year: Tecnotree: Fruit of the money tree yet to be harvested

Tecnotree is a global IT solutions provider focused on serving telecom operators. The company offers its customers cloudbased BSS systems that enable them to manage their products, customers, invoicing and digitalize their business.

Tecnotree has a colorful history since the company was under significant distress from ca. 2015-2018. The company went through a restructuring phase. Eventually the company managed well in its turnaround under the current CEO Padma Ravichander and managed to turn itself to strong growth and improve its profitability.

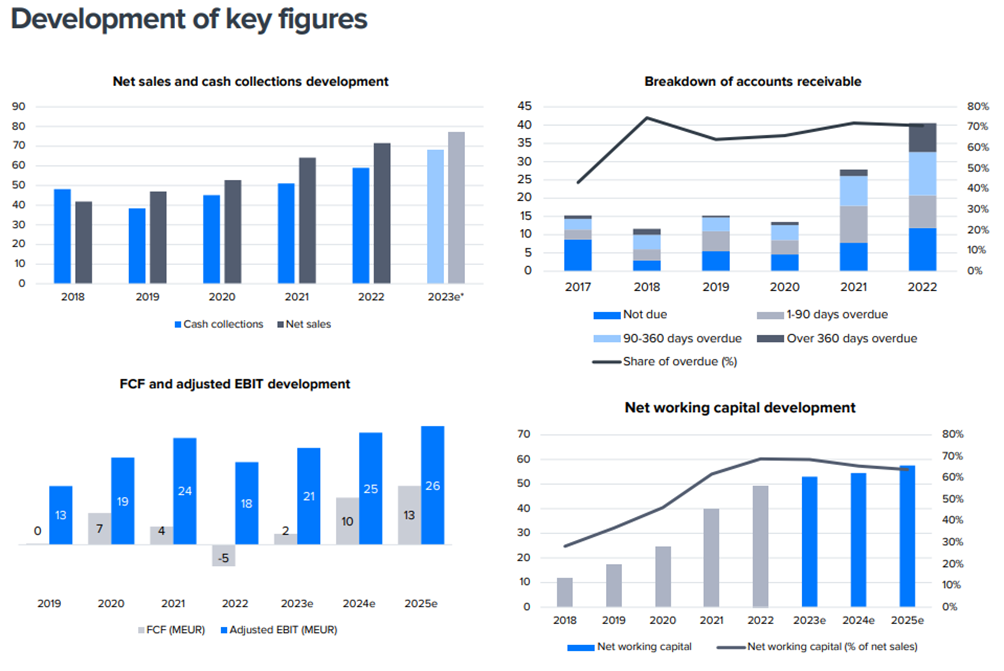

However, the return to growth has again highlighted some structural weaknesses in the company’s business model and geographical positioning. Due to the strong commitment of working capital, the company’s cash flow has been well below the strong earnings level reported in recent years. Currently Tecnotree is trying to expand into developed countries as well to mitigate risks related to operating in developing countries. For this reason as well as due to investments to R&D the company collected 43 MEUR from debentures this year.

Additionally, it’s important to note that Tecnotree invests currently heavily in R&D and activates these costs in its balance sheet. While the depreciation levels are much lower than the R&D investments this gives somewhat too good picture of the profitability.

In the longer term, we believe the growth outlook for Tecnotree is good (although there is some cyclicality in telecom operators investments), underpinned by telecom operators’ operational model shifts and the cloud transformation of BSS solutions. Expanding into new industry verticals also offers new growth opportunities while diversifying the company’s revenue streams.

Tecnotree will publish its Q3 report on Friday at around 9.00 am EEST. We expect the company to deliver single-digit net sales growth and a clear year-on-year improvement in earnings. Of particular interest in the report is the development of the order intake, which has shown signs of softening in the early part of the year. The report also serves again as a benchmark for the development of the company’s growth investments, for which the company raised EUR 43 million in convertible bonds in the summer.

Here are the analyst’s comments about the company, when Tecnotree’s largest owner takes over convertible bonds.

Tecnotree’s largest owner, Fitzroy Investments Limited has signed a binding agreement to acquire unpaid outstanding convertible debentures of EUR 20 million subscribed by Markku Wilenius. The news was awaited, but Tecnotree will probably have to wait a long time for the final funds. At the same time, it was also announced that Markku Wilenius has announced that he will resign from the company’s Board of Directors effective immediately.

Detta företag har väckt mycket diskussion i Finland, vissa ser här många risker, medan andra ser möjligheter…

Tecnotree will publish its Q4 report on Thursday at around 9.00 am EET. We expect the company’s growth to have continued at a double-digit pace, but the result to be slightly below the comparison period. We expect the company’s accounts receivable collection in Q4 to have improved from prior quarters, in line with the company’s cash flow guidance. Our interest in the report is, of course, the outlook, with a particular focus on potential cash flow guidance, which should indicate improving cash flow as the company’s business gradually moves more towards an ARR model. In the report, we are also interested in the status of missing payments on the company’s convertible bonds.

Här är Tecnotrees Q4-resultat och nedan följer analytikernas kommentarer samt en intervju med ledningen.

Tecnotree’s revenue growth in Q4 was in line with our forecast, but EBIT clearly exceeded our forecast and the company’s own guidance range. CEO Padma Ravichander and CFO Indiresh Vivekananda gives their comments on this interview.

Content:

00:00 Intro

00:17 Highlights of Q4

05:24 Revenue at constant currency

07:37 Money collection process

09:00 Decrease in accounts receivables

09:57 Outlook for 2024: currencies staying at current levels

10:39 EBIT in 2023

11:12 Cash collection in 2024

12:11 Possible acquisition

13:35 Expansion in developed markets

14:42 R&D focus areas in 2024

Tecnotree lanserar ett program för att förbättra operationell excellens.

The cost efficiency program aims to achieve annual savings of 5-7% by 2025. The company’s guidance for the current year remains unchanged and the savings are expected to be fully realized by 2025. The program is part of the company’s ongoing efforts to enhance operational effectiveness and therefore does not create an acute need for forecast changes. We will review our cost forecasts in the next update.

Här är analytikerns kommentarer om den senaste nyheten från Tecnotree.

Through the collaboration, the companies aim to launch new solutions that leverage HCLTech’s AI expertise and Tecnotree’s BSS know-how. HCLTech is a large Indian technology company and the cooperation creates interesting opportunities for Tecnotree, although the actual realization of the cooperation will be seen in the future.

A company that has generated a lot of discussion in Finland will release its earnings on Friday.

Tecnotree will publish its Q2 report on Friday at around 9.00 am EEST. We expect the company’s revenue and result to continue their upward trend, which is also indicated by the company’s guidance for the full year. In terms of cash flow, we expect a significant improvement after a very weak start to the year with improved cash collection. The main area of interest in the report will again be the future outlook for the development of the cash flow profile. We also expect an update on the situation regarding the potential company acquisition and the uncollected convertible debentures.

Tecnotrees tillväxt och resultat blev lägre än förväntat, men kassaflödet förbättrades som förväntat under årets första halvår. Bolagets vägledning gällande kassaflödet gav också ökad synlighet för kassaflödet under resten av året. Bolagets vd Padma Ravichander och finanschef Indiresh Vivekananda intervjuas av analytiker Roni Peuranheimo.

Content:

00:00 Intro

00:20 Q2 Key Points

03:39 Background of the Impairment

05:21 Reasons for the Revenue Decline

08:36 Efficiency Measures

12:20 Collaboration with HCLTech

14:57 Benefits of the Acquisition

15:53 Employee Incentive Program

16:56 Status of Convertible Bonds

17:27 Guidance and Outlook for the Rest of the Year