JA! Äntligen är översättningen av analysen här!

Vi passade på att fråga runt på kontoret vad folk har köpt senast i butiken :

Vi svängde även ihop en video om bolaget tillsammans med @arttu.heikura

TOP OF Mind:

lönsamt: även i jmf med peers: coolt!!!

solid outlook

tillväxt: ser bra ut, men på sikt: varthän? Utanför Finlands gränser (i stil med Tokmanni- Dollarstore), eller fortsätta med M&A av mindre, lokala aktörer

Här är en analys av ett företag som är älskat av finska investerare.

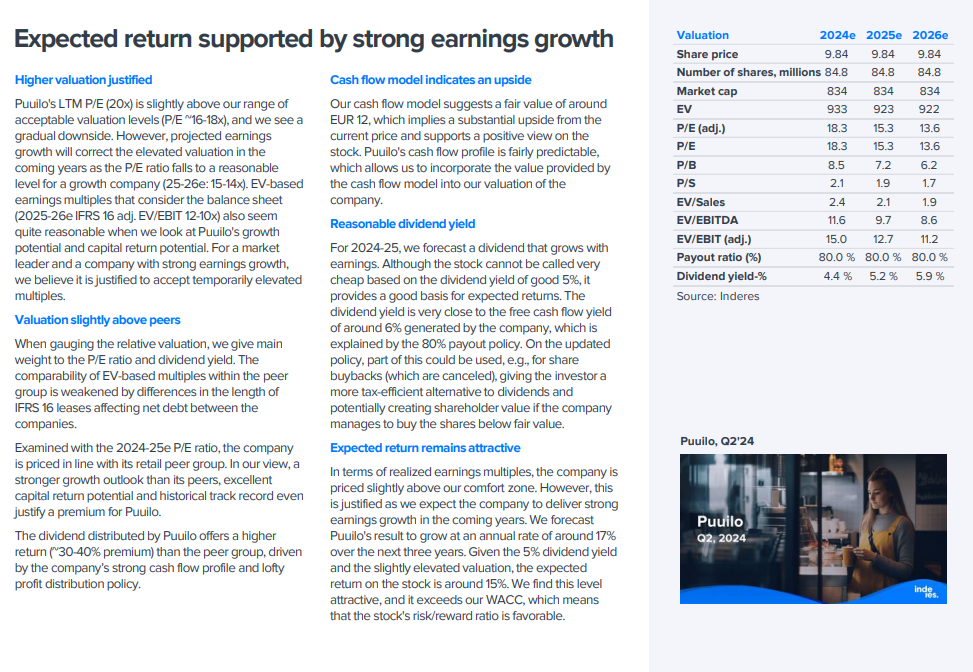

Puuilo’s updated strategy targets stronger growth than previously expected and as a result we have revised our store opening forecasts upwards. The main drivers of the company’s profit growth are a scalable cost structure driven by an expanding store network and the growth of existing stores. The near-term valuation of the stock remains slightly elevated, but we believe this is justified by the strong earnings growth profile and high return on capital.

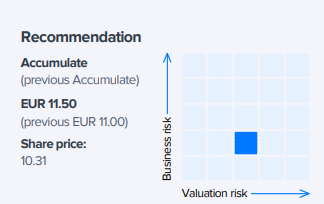

Puuilo’s Q1 report was strong as usual, driven by strong growth in customer numbers. Although the market environment remains unstable, the company has demonstrated its ability to grab market shares through a distinctive concept and cheap price image. Our growth forecasts for the next few years are driven by several annual store openings toward the target of 70 and sales growth in existing stores. The near-term valuation of the stock remains slightly elevated, but we believe this is justified by the strong earnings growth profile and high return on capital. We reiterate our Accumulate recommendation and raise our target price to EUR 11.5 (was 11), boosted by positive forecast changes.

Puuilo will report its Q2 results on Thursday September 12 at 8:30 am EEST. Although the retail trade has seen a slowdown recently, we believe the company was one of the market winners, as in previous quarters.

Analytikern Arttu Heikura har gjort en ny analys av Puuilosta.

Puuilo released a Q2 report that was quite in line with expectations. Strong revenue growth was driven by both new store openings and growth in existing stores. Profitability rose to near the historic highs of the COVID era due to favorable sales mix and successful cost control. The company revised the high end of its guidance range downward as a result of what we interpreted as a challenging outlook for the rest of the year, leading us to slightly lower our near-term forecasts. The expected total return on the stock looks attractive to us, even if the near-term valuation is somewhat stretched. We reiterate our Accumulate recommendation on the basis of a favorable risk/reward ratio but lower our price target to EUR 11.0 (was EUR 11.5) following the forecast changes.

Puuilos Q3’24-resultat förväntas visa stark tillväxt tack vare öppningen av nya butiker och måttlig försäljningstillväxt. Lönsamheten tros ha förbättrats genom ökade volymer och effektivitet. Prognosen förväntas förbli oförändrad.

Här är analytikerns kommentarer inför Q3-resultatet som publiceras nu på onsdag.

Puuilos Q3-resultat var utmärkt. Omsättningen ökade tack vare nya butiker, även om tillväxten i jämförbara butiker förblev oförändrad. Den genomsnittliga varukorgens minskning påverkade, trots att kundantalet ökade. Förbättrad marginal och effektivitet höjde resultatet. Aktiekursen förväntas reagera positivt.

Puuilo fortsatte att uppvisa stark lönsamhet och tillväxt under Q3, stödd av nya butiker, även om den jämförbara försäljningen förblev oförändrad.

Inderes förväntar sig att vinsttillväxt och en attraktiv värdering kommer att stödja aktiens avkastningsförväntningar och höjer riktkursen till 11,5 euro.

Puuilo har ökat sin marknadsandel stadigt trots den utmanande marknadssituationen.

Företaget bedöms ha potential att fördubbla sin omsättning på lång sikt, vilket skulle stödja aktiens värdeutveckling. Strategin fokuserar på att öka marknadsandelen genom att expandera butiksnätverket och stärka den redan utmärkta lönsamheten. Puuilo har visat sin konkurrenskraft även under svåra marknadsförhållanden. Trots ökad konkurrens gör företagets riskprofil och tillväxtpotential det till en attraktiv investeringsmöjlighet, särskilt tack vare en stark utdelning och förväntad resultatökning.

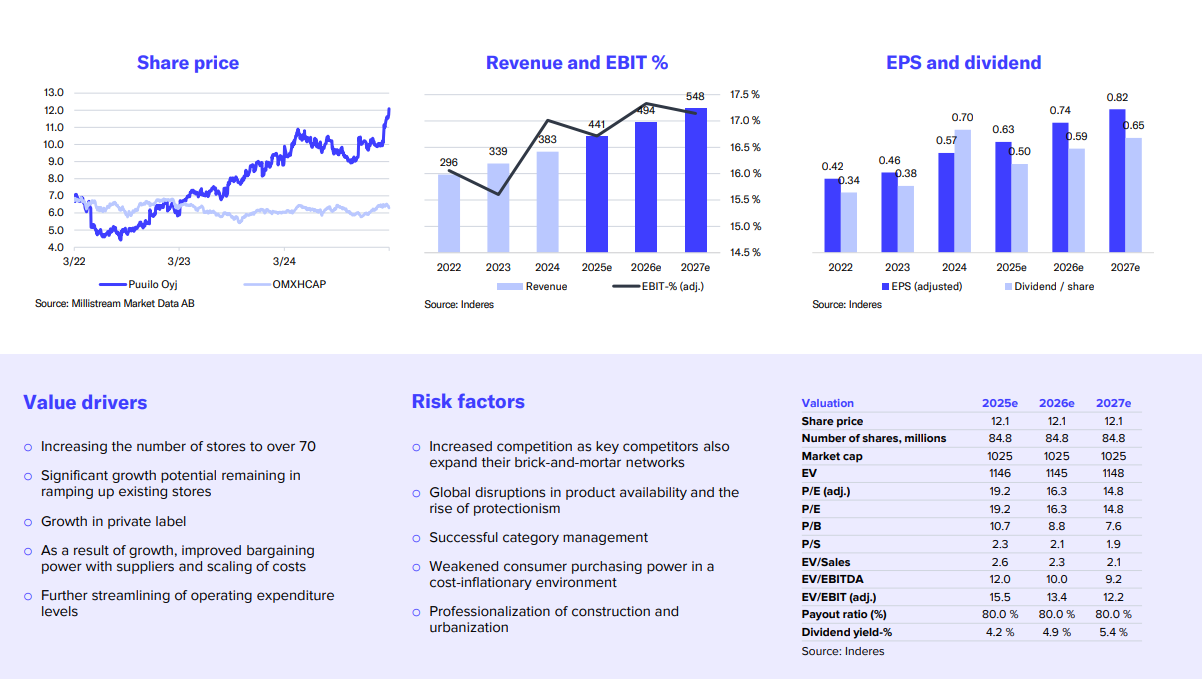

Puuilos resultat för årets sista kvartal var rekordstarkt, främst tack vare tydlig omsättningstillväxt från nya butiker. I befintliga butiker sjönk dock genomsnittsköpet, eftersom konsumenterna valde billigare produkter och egna varumärken, vilket ändå stärkte marginalerna. Bolaget meddelade en extrautdelning tack vare starkt kassaflöde och låga investeringsbehov. På kort sikt kan kostnadstrycket och öppningen av nya butiker pressa lönsamheten, men på längre sikt stöds resultatet av ökad effektivitet. Dagens aktiekurs förefaller ändå hög jämfört med tillväxtutsikterna, vilket innebär att investerarnas avkastning främst baseras på utdelningar och att säkerhetsmarginalen är begränsad.