Tråkigare aktie får man leta efter på Helsingfors-börsen. Nokia har väl närmast levererat en lång rad besvikelser de senaste +20 åren. Under den nya(ste) ledningen verkar det dock som det börjat synas ljus i tunneln; kanske t.o.m. någon slags turn-around i sikte.

Idag gjorde jag ett köp @4,35 €. Jag har inte rört denna position på flera år; senaste köpet gjort under €4. Men nu levererade Nokia ett så starkt resultat (både Q4/2022 och 2022), kombinerat med någon form av prisnedgång (YTD: -1,95% / 3m: -2,31% / 6m: -14,75% / 12m: -14,48 %) att jag helt enkelt inte kunde motstå frestelsen.

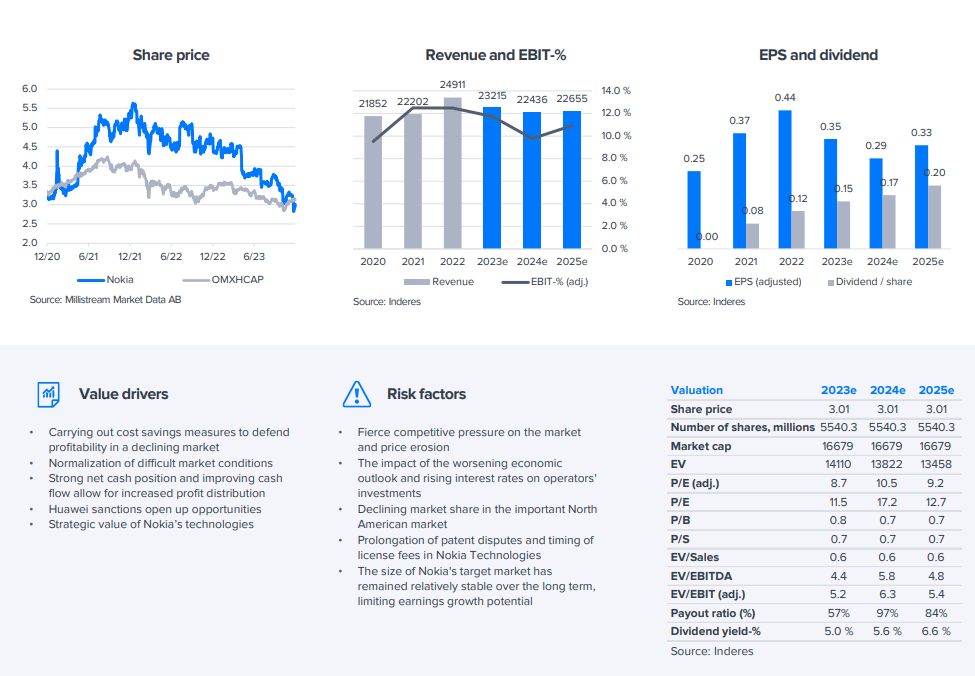

Svårt att se hur Nokia skulle vara dyr just nu. 2023 prognoser ~ P/E 10x, P/B 1.1x, dividend 4.1% och EV/EBIT 6.5x. Men om aktiekursen fortsätter att falla från denna nivå, så tror jag att jag kommer att fortsätta köpa.

Yeah it is easy to agree that Nokia looks undervalued at the moment. The key question is what will be the catalyst or value driver that fixes the situation. Everybody can see those low multiples but for some reason investors are cautious that Nokia’s current earnings levels will hold up. Despite the fact that Nokia’s outlook and financial targets indicate that the comparable EBIT will still improve from current +3000 MEUR levels. All in all, interesting situation with the share and hard to see much downside if the earnings hold up.

Pretty much my 2 cents as well. The markets have abandoned Nokia years ago, and seemingly no results are sufficient to rectify the situation. It might be that we’ll continue sideways for a long time still (my own guess), but indeed I think the upside (after a couple of more Q:s beating the forecasts) is larger & more likely than a substantial drop from the current valuation level.

How will Nokia fare if the economy clearly weakens? When considering how fierce the competition is in Nokia’s fields of market. On the other hand, Huawei is facing major problems, which offers opportunities for Nokia. The company also has the “money” and possibilities, as it has technological expertise.

Feel free to answer my question briefly, although it may be challenging. I’m trying to understand the big picture better.

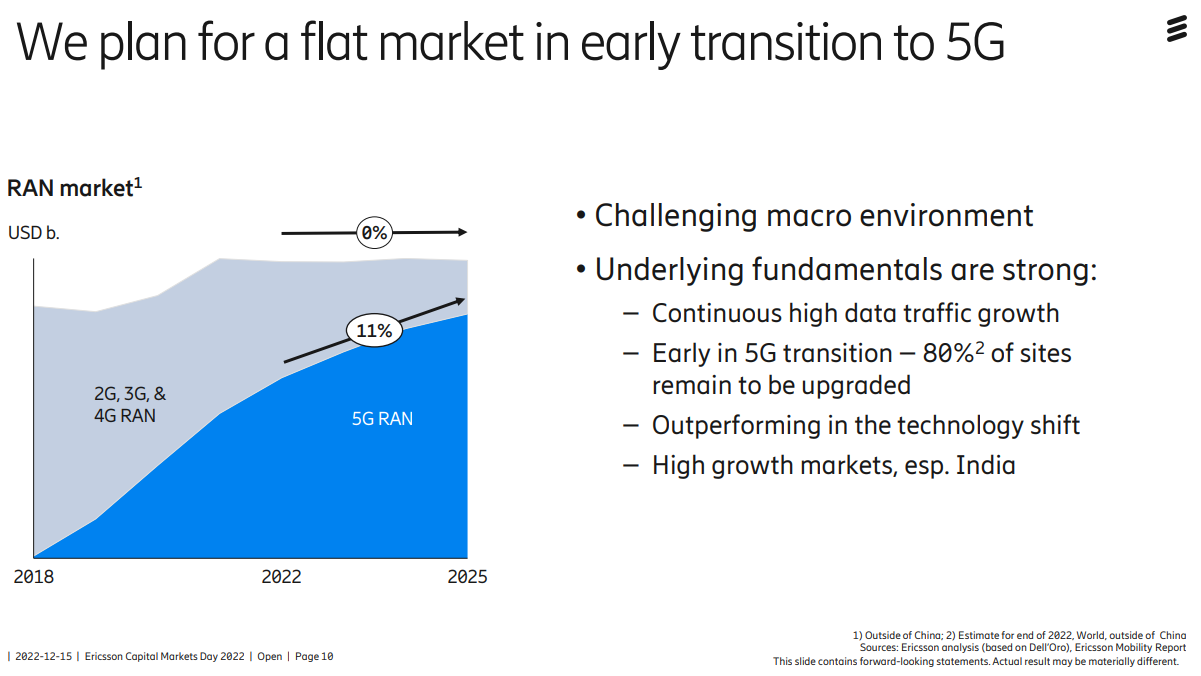

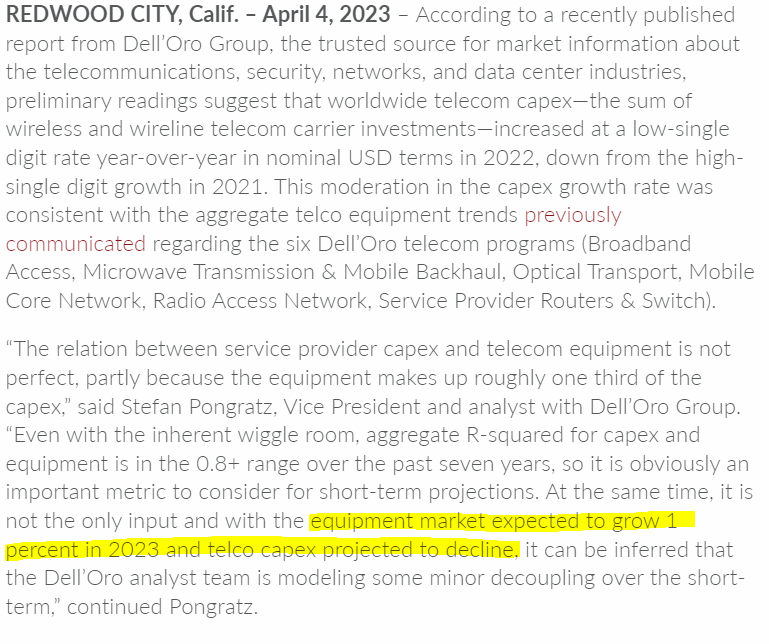

Market research firm Dell’Oro published their latest market forecast just a month ago and they are still expecting 1 % growth even though capex budgets are declining this year.

Nokia also reiterated its outlook for 2023 and is still guiding with the guidance midpoint stable earnings for this year. All in all, in a recession it would be really hard for Nokia to grow its earnings, but I think pretty stable development is still achievable. The stock is trading currently with 2023e P/E ratio of 9x so it seems that markets are already pricing in pretty steep decline in earnings. So if Nokia is able to roughly maintain its current adj. EBIT level of +3000 MEUR, it is pretty fair to say that the stock is very cheap at the moment.

I appreciate how interestingly and comprehensibly you are able to explain these things. Thanks to you, I now have a better understanding of the whole picture.

I could imagine that Nokia is really cheap. Nokia has had a tendency to surprise both downwards and upwards, so it’s definitely not a sure case.

Alltså Nokia, Nokia… vad kan man säga. Just nu nästan lite sorgligt.

Jag har personligen svårt att se vad som skulle kunna fungera som tillväxtmotor i detta skepp…

SAMT: Vad är det, egentligen, som får en kund att välja ett visst bolag inom sektorn? … Syftar nu på AT&T dealen. Dvs varför förlorade Nokia mot Ericsson, denna gång, egentligen?

Om jag, på ett personligt plan, inte tydligt kan definiera ett bolags kritiska framgångsfaktorer framom konkurrenternas, så håller jag mig borta.

OBS! DISCALIMERS:

Detta INTE rådgivning - bara allmäna tankar och mitt eget synsätt gällande min egen handel.

Det kan även handla om att jag själv bara har för lite förståelse för såväl case, som bransch, eller helt enkelt är för fattig (i såväl plånbok, som sinne) för att det skall vara ngt för mig

We have updated our forecasts to take into account the extension of patent negotiations in Nokia Technologies into this year and the divestment to be made in Cloud and Network Services. For other areas, we will review our forecasts in the context of the Q4 report

Nokias Q4 från igår. . Togs överraskande emot positivt av marknaden under gårdagen.

Nu finns en ny analys ute av @Atte_Riikola. “Nokias resultat för det fjärde kvartalet och utsikterna för 2024 var i stort sett i linje med förväntningarna. Vi såg inget behov av betydande förändringar i våra vinstprognoser på koncernnivå, och det är därför vi fann aktiekursreaktionen (+11%) på resultatdagen överraskande.” Läs mer här:

Investors in Nokia may be interested in the company’s latest strategic moves and the insights provided by analyses. Here’s a summary of the most essential aspects from an investor’s perspective:

Collaboration with Google Cloud Nokia has announced an expansion of its 5G partnership with Google Cloud. The aim is to accelerate the development of 5G applications using telecommunications Application Programming Interfaces (APIs). This collaboration could offer significant opportunities, particularly in the healthcare sector, where telemedicine services are being enhanced.

Financial Results and Profitability Nokia has succeeded in improving its return on equity, reaching 18.1% in the first quarter of the year, up from 17.1% the previous year. Additionally, the cost-to-income ratio remained stable at 40%, excluding regulatory expenses.

Risk Factors and Challenges Major potential risks include declining interest rates, uncertainties in European and Nordic economic development, and weak trends in the housing market. Competition, particularly from China, has posed a significant challenge impacting Nokia’s profitability.

Cost Savings Program and Future Outlook Nokia has initiated a cost savings program expected to generate approximately 400 million euros in net savings this year and positively impact cash flow next year. Nokia aims to maintain a net cash position of 10-15% of revenue, providing flexibility for potential future investments and shareholder rewards.

Stock Price Performance and Share Buybacks Investtech analysts predict continued positive stock price development for Nokia. Nokia has also announced plans to repurchase its own shares, which could enhance shareholder value. The net cash position is expected to remain strong, although it may decrease slightly in the Q2 report due to performance-based payments.

Market Situation and Competitive Position Increasing market share, disciplined cost control, and new patent licensing agreements could improve Nokia’s competitive position. Challenges posed by Chinese state subsidies have slowed profitability improvement, but Western measures to restrict Chinese competitors could yield long-term benefits.

Investor Patience and Future Expectations Investor patience is being tested, but the company’s strategic initiatives and investments in research and development could yield long-term results. Expectations are high for Nokia’s management to increase shareholder value and operate more profitably.

Nokia säljer Alcatel Submarine Networks-verksamheten till franska staten

Nokia har tecknat ett försäljningsoptionsavtal om att sälja Alcatel Submarine Networks (ASN)-verksamheten till franska staten för 350 miljoner euro. Affären är dock villkorad av konsultation med Nokias och ASN personalrepresentanter. Denna försäljning, tillsammans med gårdagens tillkännagivande om förvärvet av Infinera, innebär en betydande omstrukturering av Nokias nätverksinfrastrukturverksamhet. Försäljningen stödjer Nokias strategiska fokusering, och nätverksinfrastrukturverksamheten kommer framöver att koncentreras till tre enheter: Fixed Networks, IP Networks och Optical Networks. Nokia behåller en 20 % ägarandel i ASN under övergångsperioden, och affären förväntas slutföras i slutet av 2024 eller början av 2025. Affären förväntas förbättra affärsområdets lönsamhet.

Ny analys av Nokia av Inderes analytiker Atte Riikola

We reiterate our Reduce recommendation for Nokia but revise our target price to EUR 3.3 (was 3.1 EUR). We believe that the bid for Infinera and the sale of ASN, the submarine network business, are strategically sound moves and strengthen Network Infrastructure’s position as Nokia’s most valuable network business. However, the price paid for Infinera is high relative to the company’s current profitability, and value creation requires the realization of targeted synergies, for which the growing scale of the Optical Networks business provides a good basis. However, the transaction does not completely change the big picture around Nokia, and we believe that the weak earnings outlook for Mobile Networks in the coming years will continue to weigh on Nokia’s acceptable valuation level.

Nokia, denna före detta stolthet i Finland, har publicerat sitt resultat.

Nokia rapporterade ett jämförbart rörelseresultat som överträffade förväntningarna, tack vare en stor engångspost relaterad till mobilnätverken på grund av uppsägningen av AT&T-avtalet.

Utan denna engångspost var utvecklingen inom nätverksverksamheten svagare än väntat, och Nokia sänkte sina tillväxtförväntningar för hela året. Omsättningen minskade med 18 % till 4,5 miljarder euro, vilket var lägre än förväntningarna. Inom mobilnätverken sjönk omsättningen med 25 % på grund av den svaga marknadssituationen. Omsättningen inom nätverksinfrastrukturen sjönk med 11 % jämfört med föregående period. Omsättningen inom moln- och nätverkstjänster minskade med 17 %. Inom teknikdivisionen var omsättningen något bättre än förväntat. Nokia förväntar sig fortfarande att det jämförbara rörelseresultatet för 2024 kommer att vara 2,3–2,9 miljarder euro.