Greetings!

We initiated the coverage Enento about a week ago. I’m the analyst following the company and if you have any questions I’m happy to answer them. Here’s a link to the fresh extensive report: Enento: The Nordic credit information king

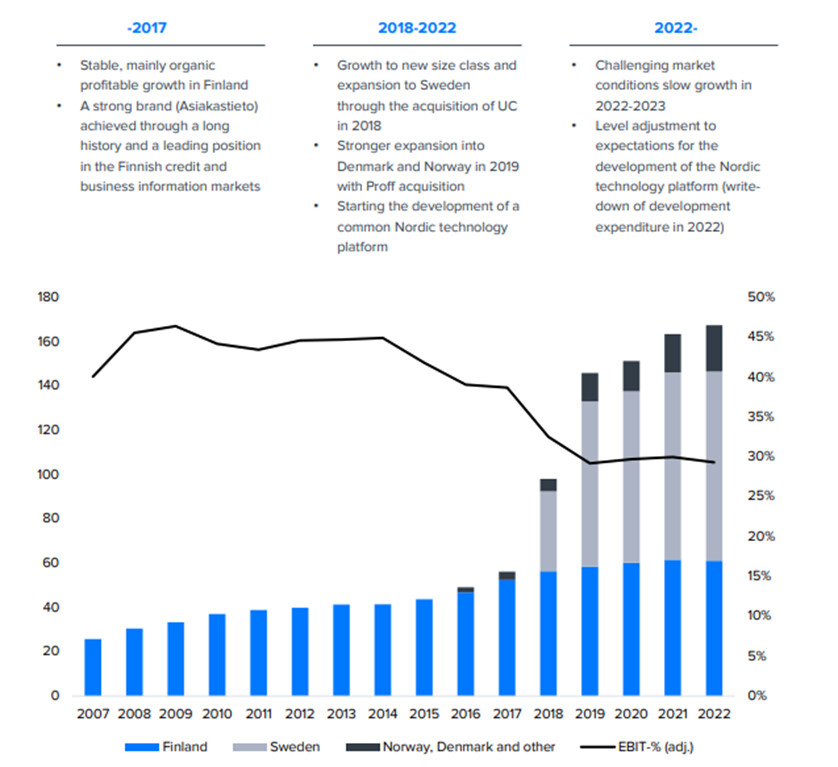

Enento is one of the leading providers of digital business and consumer data in the Nordic countries. The company’s product offering, and client base is broad, and its services are used in areas such as risk management, sales and marketing, and real estate. At the core of these services is the data collected from a wide range of information sources in the company’s database, which the company processes and uses to develop a range of services that enable informed decisions in the various financial transactions of its clients. Enento has long-standing roots in Finland, where the company still operates mainly under the Asiakastieto brand. The company has expanded into other Nordic countries through acquisitions and operates under the UC, allabolag.se and Proff brands. The core of Enento’s business are credit information services where Enento is the market leader in Finland and Sweden (under Asiakastieto and UC brands).

Enento has a solid track record in profitable growth and the company’s business model is quite stable and defensive (revenues include both cyclical and counter-cyclical elements). This year, the company faces a number of headwinds as the challenging market environment (lower demand for loans and weak SEK), regulation (Finnish interest rate cap regulation in the fall) and internal factors (exit of the Tambur service) weigh on net sales. Typically the company as been resilient against bigger crisis situations and been able to generate strong cash flows in harder market environments as well.

I’ve been somewhat prejudiced towards this company for a while because the industry it operates in has seemed old-fashioned to me, something that can’t grow and generate enough returns. However, this has been my own conclusion and imagination, not based on facts.

Nevertheless, Enento has shown surprisingly good profitability over the years, even in the long run. It didn’t particularly surprise me that the company is stable.

Not particularly for me, but some might also be interested in the company’s decent dividend yield…

Risk and opportunity at the same time in a new technology platform.

I see that this company could be a defensive representative in the portfolio, providing security.

Enento lowered it’s net sales guidance for the current year. The profit warning was not particularly dramatic, as our estimate was already previously at the lower end of the previous guidance range. Thus the estimate cuts were rather modest. Nevertheless, Enento is not immune to the challenging operating environment and suffers especially from weakened demand for its consumer information services. On the other hand the demand for its risk management and compliance services seems to be on a good level.

Here’s a link to our report published today with new estimates:

Analytikern Roni Peuranheimo har gjort en intressant analys av Enento inför deras Q4-resultat som kommer att publiceras på fredag.

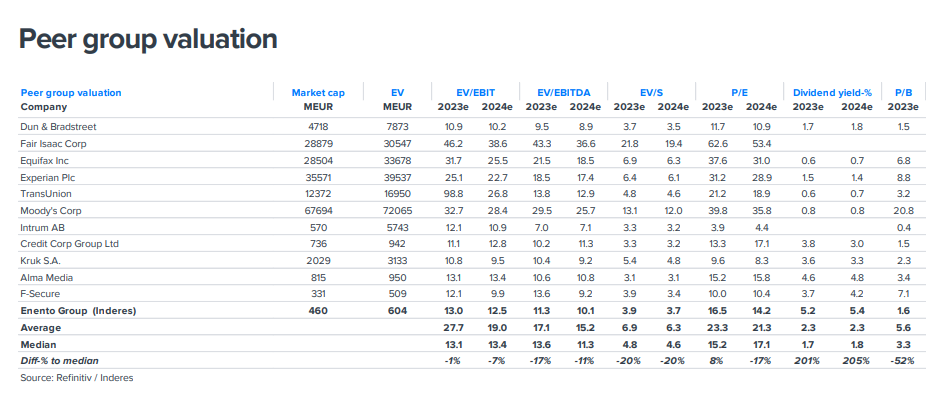

Enento’s operating environment has remained challenging in Q4, and thus we expect the company’s revenue and earnings to continue on a clear downward trend. Due to the weak market development, we have made slight negative adjustments (2-3%) to our revenue and earnings forecasts for the next few years. With the share price rise, the strongest undervaluation (2024e adj. EV/EBIT 12.5x and adj. P/E 14x) has dissolved, but we still find the expected return consisting of earnings growth and dividends attractive.

Nu finns den första intervjun på svenska ute med VD Jeanette Jäger. Lär dig mer om Enento, vad de gör och hur Q4 rapporten var samt mycket mer. Har du fler frågor så finns @roni.peuranheimo här på forumet som gärna hjälper er att förstå mer kring Enento.

Ny analys efter Enentos Q1 rapport som presenterades igår.

Enentos operativa nyckeltal för Q1 var i linje med våra prognoser. Guidning har fortfarande inte lämnats och i synnerhet är visibiliteten för utvecklingen av den svenska marknaden för konsumentkreditinformation fortfarande svag.

Enento publicerar sina resultat nästa tisdag och här är analytikerns kommentarer om det:

Enento will report its Q2 results on Tuesday, July 16 at 12.00 noon EEST. The operating environment remained challenging in Q2 and we expect revenue and earnings to continue to decline despite a relatively weak comparison period. The main reason for the weakness remains weak demand for consumer credit information services in Sweden. The company has still not yet issued guidance for the current year due to the low visibility of the operating environment, which makes forecasts more uncertain than usual. Any comments on the outlook for the market and the company’s adjustment measures will again be of particular interest. We have made slight negative revisions to our Q2 forecasts in the context of our pre-comment.

Hur gick det för Enento i Q2? Titta på videon så får du veta.

Enento’s development in Finland, Norway and Denmark continued in a positive direction while consumer credit information sector continued to face a challenging operating environment in Q2. CEO Jeanette Jäger and CFO Elina Stråhlman comments on the past quarter in this interview.

Content:

00:00 Intro

00:15 Enento Q2

01:52 Costs transferred to H2

03:51 Positive credit register

04:47 Discussion about over-indebtedness

05:40 H2 expectations

06:10 Sweden markets

07:28 Mergers and acquisitions

@roni.peuranheimo har gjort en bra rapport om företaget. Det är värt att läsa!

Enento’s results were slightly ahead of our forecast, but this was driven by a lower-than-normal cost structure, which we expect to change in H2. The company provided anticipated revenue guidance, which, in line with our expectations, indicates a further decline in sales this year. In general, the demand environment is showing signs of stabilization. Looking ahead to next year, we think the valuation is at an attractive level (adj. P/E 14x and EV/EBIT 12x) and argues for a positive view. We reiterate our target price of EUR 19 and Accumulate recommendation.

Enento kommer att publicera sitt Q3-resultat tisdagen den 29 oktober runt middagstid. Efterfrågemiljön har ännu inte visat någon betydande återhämtning, och Inderes förväntar sig att både omsättning och resultat kommer att försämras jämfört med jämförelseperioden. Bolagets utsikter är blandade: räntesänkningar stödjer utvecklingen, och i Sverige verkar det som att det potentiellt skadliga offentliga kreditregistret inte kommer att införas.

Samtidigt kan dock de föreslagna åtgärderna i Sverige för att begränsa skuldsättning, såsom en skärpning av räntetaket, bromsa marknadens återhämtning nästa år. Inderes upprepar målkursen på 19,0 euro men sänker rekommendationen till minska-nivå (tidigare öka), efter att aktiekursen har sjunkit.

Enentos aktie har varit under press, men sjunkande räntor och en mer måttlig värdering gör den mer attraktiv. Trots fortsatt osäkerhet på den svenska kreditmarknaden förväntas bolaget återgå till tillväxt under 2025. Enentos konsumentverksamhet är fortfarande långt från sina toppår, men en stabil affärssegment stöder tillväxten.

Här är en utmärkt analys av bolaget från en analytiker:

Enento kommer snart att publicera sin rapport för det första kvartalet. Omsättningen förväntas ha förblivit stabil medan lönsamheten har försvagats något. Marknadsmiljön har inte förändrats nämnvärt, men den ekonomiska osäkerheten har ökat. Prognoserna har justerats nedåt i viss mån, och med hänsyn till riskerna börjar aktiens värdering se attraktiv ut för långsiktiga investerare.

Enentos vd Jeanette Jäger diskuterar bolagets utveckling och utsikter i en intervju med analytikern Roni Peuranheimo.

00:00 Q1 Highlights 03:18 Profitability 03:52 New Regulation in Sweden 04:37 Premium Business 06:28 Financial Impact 07:30 Trade War Effects 08:20 Focus Areas

The past few years have been challenging for Enento, as weaker demand for consumer credit information due to structural changes in the Swedish market has driven down revenue and results. At the start of this year, the company returned to growth after a two-year downward trend and, despite the still somewhat cloudy outlook for the Swedish market, we expect the company to continue growing in the coming quarters and years. Following a modest increase in the share price, the valuation (2025e-2026e adj. P/E 19x-15x), has reached a neutral level, in our view, already carrying the promise of improved earnings in the coming years. We reiterate our EUR 17.5 target price but lower our recommendation to Reduce (previous Accumulate).