Duell börslistades under senare halvan av 2021. Vid en första anblick ter sig caset mindre intressant för den som inte är insatt i “power sports”. Vid en närmare titt kan man konstatera att detta distributörsbolag:

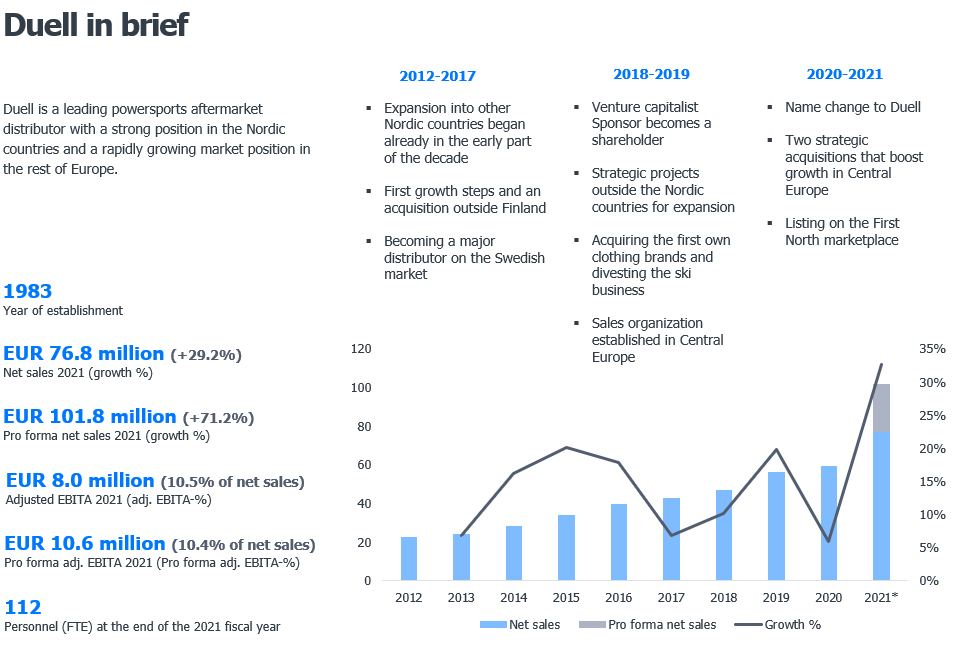

1)har en imponerande brand portfölj : över 290 st, varav 19 egna varumärken.

2) är ett tillväxtcase i alla meningar. Bolaget har en historia av organisk tillväxt som alltid varit snabbare än marknaden i sig. Framöver (se översiktsgrafer nedan) ämnar man växa både organiskt och genom M&A:s (vilket redan inletts).

opererar på en marknad som ger utrymme att växa. Klipp från bolagets webbplats: “Duell’s main addressable aftermarkets in Europe was estimated to be worth approximately EUR 6.1 billion in 2019. The aftermarket for onroad motorcycles accounted for EUR 5.2 billion and the aftermarket for offroad motorcycles for around EUR 0.9 billion.”

“Between 2019 and 2025, Duell’s main addressable market is estimated to grow at a compound annual growth rate (“CAGR”) of approximately 2 percent.”

RISKER?

Hur mkt påverkar inflationen? Hur tacklar en distributör krångel i distributionskedjan? Är bolagets tillväxtplaner realistiska: vad krävs isåfall?

På dennna video sammanfattar analytiker Petri Gostowski Duell som case:

Inderes Portfolio has a pretty solid track record, and I thought it would be useful to highlight its most recent transaction here. Duell was bought as a new company about a week ago in the portfolio.

Two operational directors have left, there is a lot of debt, and the growth prospects seem a bit weak to me. I am somewhat concerned, but on the other hand, the stock is not “expensive”.

Do you think Duell has a chance to improve its profitability and adjust its cost structure?

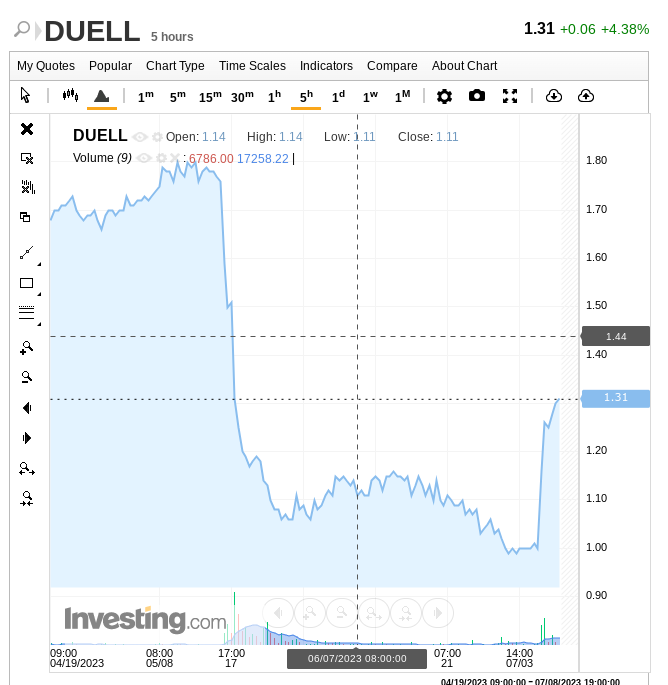

Duellin stock has plummeted incredibly in a rather short period of time.

The company has very little pricing power, and on top of that, the debt burden is very high, with rising interest rates. There have been departures in the company’s management, there is a significant amount of unsold inventory, and overall, the numbers are not reassuring.

Is Duellin’s existence threatened?

I apologize for the dramatic tone, and thank you in advance for your response!

I’ll follow up on @börsen84’s concerns about Duell’s liquidity situation and a possible liquidity crisis. I’d like to ask @petri.gostowski about the cost savings programme: how much do the forecasts for following financial years (especially 2024 financial year) rely on these cost savings? And though the liquidity crisis is a real concern when one considers the risk level of the company, I’d like you to shed some light on how likely this scenario really is, especially when one considers the already released cost savings programme. In addition I’m having a thought that if Duell e.g. has to issue new shares due to the current liquidity situation then it would sound odd in a way for the pricing of the issue to be very low (i.e. the dilution to be high), if the investors see the situation of Duell being a temporary issue (e.g. the NWC narrative that’s been spun around many times already in discussions) Maybe I’m just overthinking because of the fact that I want to believe that the market doesn’t offer free lunches at least easily in any way, shape or form

The revenue is unlikely to be good, and profitability is also unlikely. There are several issues that are troubling, such as inflation and purchasing power, “inventory problems,” and so on. I believe many small investors will see it as a buying opportunity if the stock price continues to decline, but personally, I see a lot of risks that might deter me from getting involved, even if the stock price drops significantly further.

Duell will announce its fiscal year 2023 Q3 report next Thursday at approximately 07:30, and at 08:30 Finnish time.

The Q3 figures reported by Duellin on Thursday were better than expected.

The decrease in net working capital and debt level were positive developments, indicating reduced risks. Duellin’s performance was good in many ways, and as a result, the stock price increased significantly.

The current recommendation is “buy,” whereas it was previously “reduce.” The target price is 1.6 euros.

Duell har utfärdat en resultatvarning. Enligt analytikerna verkar även resten av året bli svagt, och utifrån vad jag har läst ser jag inte en särskilt ljus närtid framför mig.

Bolagets skuldsättning och övergripande dåliga prestation gör mig mycket försiktig när det gäller detta företag. Dessutom verkar branschen inte vara särskilt lönsam, och enligt min uppfattning kan företaget inte “lätt” förbättra sin lönsamhet, eftersom prissättningen inte kan ändras mycket.

Det har skett små förändringar i ledningen, förhoppningsvis kan detta föra med sig något positivt och nytt.