Digital Workforce växer snabbare än IT-tjänstemarknaden och blir mer lönsamt i takt med skalningen. Bolaget förväntar sig högre intäkter och lönsamhet 2025, och en stark försäljningspipeline stödjer tillväxten. Aktiens värdering är attraktiv, och i takt med att vändningen fortsätter stärks förtroendet för den långsiktiga potentialen.

Läs en högkvalitativ analys av bolaget!

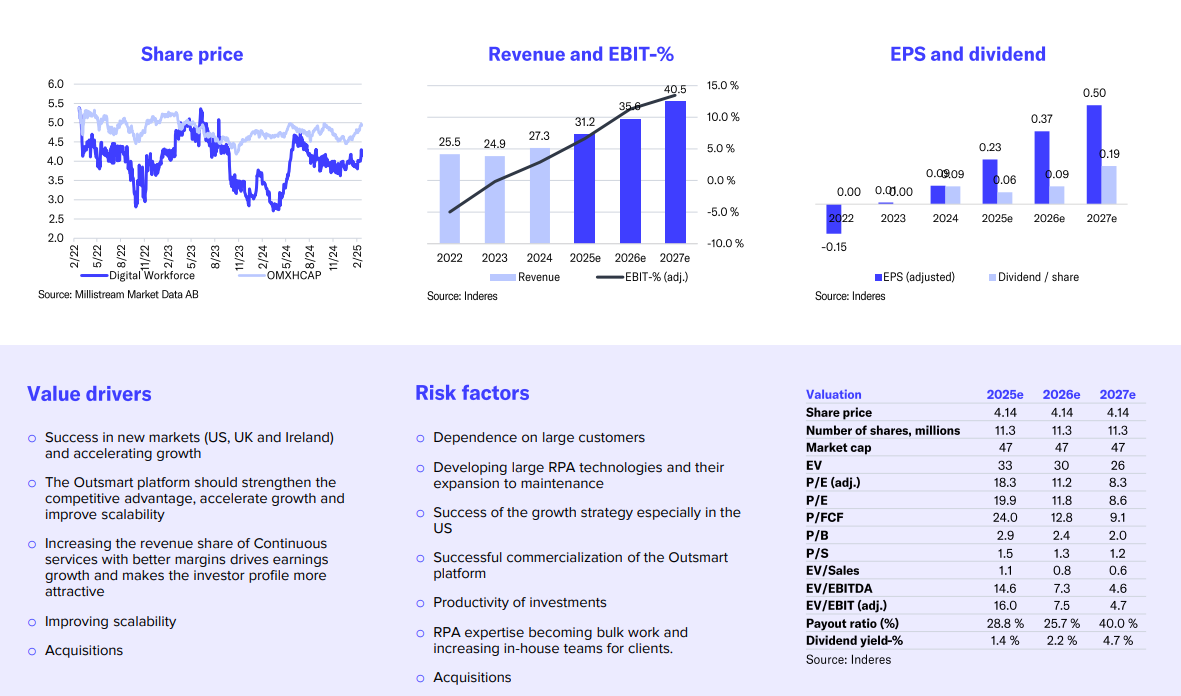

We reiterate our target price of EUR 4.7 and our Accumulate recommendation. Digital Workforce’s financial statements were well in line with our expectations in terms of revenue, earnings and guidance. The company also commented that the sales pipeline remains good and its quality has improved. We leave our forecasts largely unchanged and expect the company to grow well ahead of the IT services market in the coming years and to scale this growth to profitability. The stock’s valuation picture (2025e EV/EBIT 16x, P/E 18x, sum of parts EUR 5.2) supports our positive view on the stock. As the earnings turnaround continues, investors can start to rely more strongly on the company’s very attractive longer-term valuation picture.