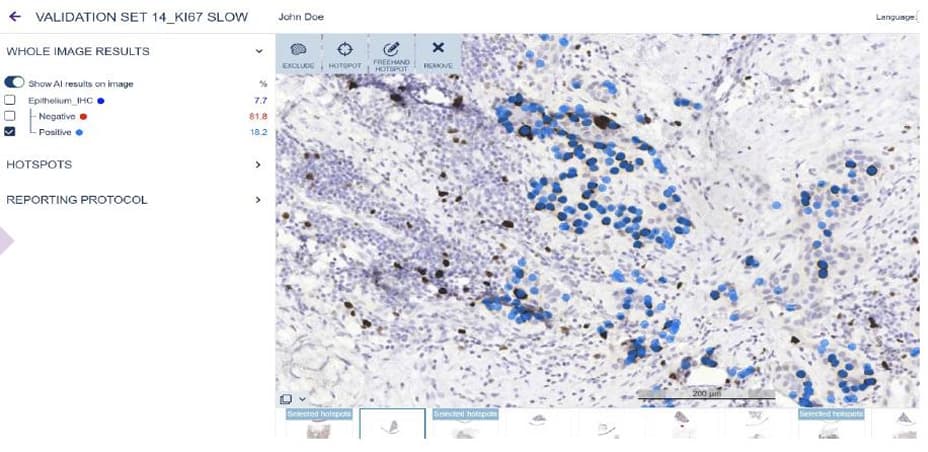

Aiforia (Artificial Intelligence for Image Analysis) is a Finnish software company focusing on automating pathology. Their software is used to aid pathologists in tissue analysis. Their software can, for example, quantify the number of certain cancer-diagnosis related cells and highlight them in a scanned image of a tissue sample. Pathologists can then check if the cells are correctly identified and write their report for the doctor treating the patients. Pathologists can create their own image recognition models by annotating their tissue sample slides, so they don’t need to wait for ready-made models that software providers need to push through regulative approval processes.

Demand for automation in pathology seems clear: population is getting older and living longer, which unfortunately brings more cancer cases to medical services. There is already a shortage of pathologists and meeting the demand of cancer diagnostics creates a need to improve productivity in pathology laboratories. Cloud storage has gotten cheap enough quite recently (tissue sample slide images have pretty huge file sizes) and COVID pandemia gave laboratories a reason to start going digital (you need to have tissue slides scanned to digital format to work remotely - pathologists used to look at their images with microscopes). Adding to these market drivers is the recent increased interest in AI & automation. Together these changes seem to have now triggered the first wave of investments in digital pathology and related AI-solutions.

Aiforia started from medical research / education segments and already had a global customer base in this segment when they did their IPO late 2021. Since then, their entry to the clinical market (which has the big revenue potential) has progressed steadily. Mayo Clinic (USA, often ranked #1 hospital in the world) begun Aiforia’s clinical use in breast cancer diagnostics in March 2023. Aiforia has also signed clinical deals with a NHS trust (UK), Veneto Hospital district (Italy), City of Hope & Wake Forest (USA, including pre-clinical use and clinical use), and many large pharmaceutical companies (10+ large customers in the segment). While there is a varity of players competing in this market, Aiforia has gotten really strong reference cases (especially Mayo Clinic) and seems to have a competitive solution.

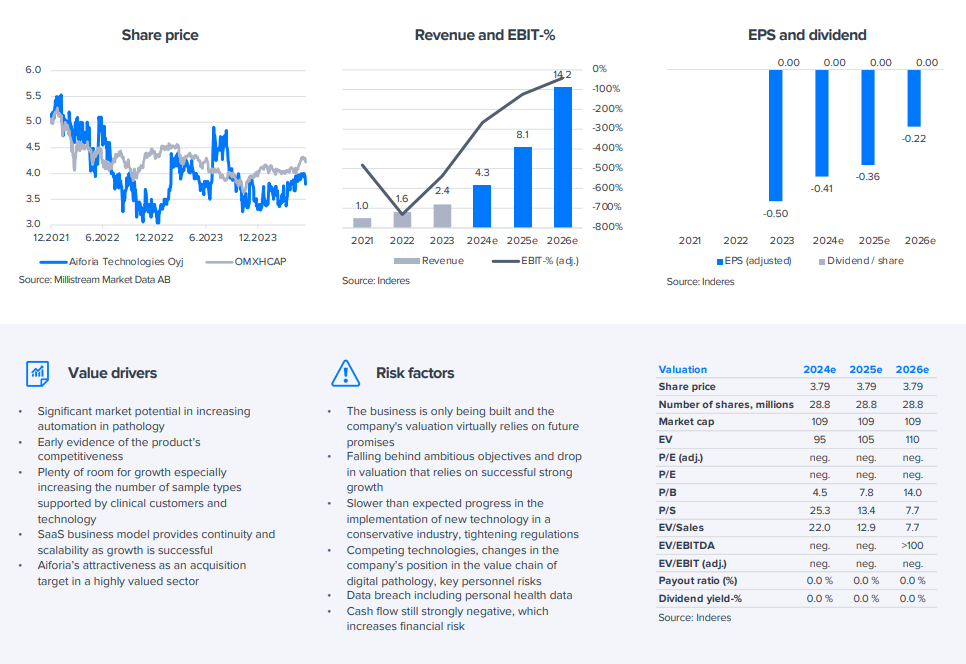

The customers Aiforia has already won have significantly broad & high volume use cases and we believe that each of their existing ~3 large clinical customers have revenue potential of at least a few MEUR per year. Aiforia’s 2022 revenue was just below 2 MEUR and hence their growth is largely dependent on especially how fast they can expand their existing customers. New customer wins are naturally also important, but their near-term growth is leaning heavily on a selected number of existing customers.

At the flipside of the potential and good market momentum in an attractive market, Aiforia is at their early stage of growth and still burning cash. With our current estimates cash would run out early 2025. Their growth is also difficult to forecast and long term development of their competitiveness & market is naturally really hard. However, if their good market momentum continues, we see a good likelyhood that the needed growth capital would be available at reasonable terms and dilution.

We published our latest report after their H1’23 report today, feel free to take a read / ask us questions / add your thoughts here

You produce excellent analysis and material, and you explain things very clearly and realistically. It’s enjoyable to read investment-related content like yours that is both pleasant to read and easy to understand.

You don’t need to answer my question if you find it irrelevant, but when you analyze a company like this or, I apologize, when you begin analyzing a company like this for the first time, how do you familiarize yourselves with such a company and its industry, which can be very difficult to understand unless you work in that field?

Aiforia published a blog post summarizing year 2023 a few interesting pieces of information:

“The Veneto Region Health Authority in Italy selected Aiforia as a partner for AI-assisted diagnostics in its clinical pathology laboratories. The full clinical workflow has now been installed and is in pilot use.”

"We expect to launch our first IVDR-approved AI model next year. " (Regulatory approvals have been stuck for a while due to EU MDR-legislation update that became effective in May 2022)

"Short-term targets for 2024–2025 will be published in January. " (More visibility incoming to how the company sees its business developing - 3/4 of the previous short term targets were reached and the 4th one almost, so compan’ys track record with these has been so far pretty good)

Aiforia uppdaterade sina affärsmål och här kommer analytikernas kommentarer i frågan.

Aiforia updated its short- and mid-term targets and provided specified strategic priorities, which in the big picture were largely in line with our expectations. Aiforia in practice achieved its previous short-term targets, and the new targets concretize the business progress in the short term. The company is also aiming for positive profitability by the end of 2027, which is in line with our forecasts.

Aiforia, a software company automating pathology with AI, will publish its H2 report on Thursday at around 9 am EET. We expect the company’s revenue to continue to grow strongly as deployment to new customers in clinical segments progresses. Growth investments continue to keep the result at a clear loss, but we expect the earnings trend to be reversed and the loss to decrease from the comparison period. In addition to the growth figures, we focus on the progress of clinical customer deployment, order book development and comments on the 2024 outlook. We do not believe that the company will provide guidance due to the low predictability of the business, even if it would be a clear signal of the company’s confidence in its own growth.

Aiforia’s H2 was largely in line with our expectations and the company’s sales pipeline is still promising. We still consider the company’s competitive position as good and if Aiforia continues winning customers as expected, the potential will gradually begin to emerge more clearly in revenue. On the other hand, poor growth predictability and elevated financial risks argue for some caution in pricing the potential.

Förra veckans aktieemission på 10 miljoner euro har stärkt Aiforias finansiella situation. Med tanke på positiva försäljningsnyheter verkar företaget fortsätta mot en stark position på sina snabbt framväxande marknader, även om den svaga förutsägbarheten i tillväxten fortfarande talar för en viss försiktighet vid prissättningen av potentialen.

Här är analytikerns färska kommentarer om företagets nya samarbetsarrangemang.

The regional health management of Castilla y León in Spain has chosen Aiforia as its partner for AI-based diagnostics. The collaboration involves the use of selected Aiforia AI solutions for the analysis of tissue samples, e.g., from breast, prostate, and lung cancer patients. The total value of the contract for Aiforia is around 500 TEUR over three years, which means an annual billing of around 167 TEUR. This makes the contract quite significant for the company, but achieving the growth forecasts for the coming years will obviously require similar successes.

Fimlab Laboratories Ltd, Finland’s largest healthcare technology company, has selected Aiforia Technologies Plc as the provider for breast and prostate cancer diagnostics solutions. The value of the first order is approximately EUR 300,000 for the first year, which is some 7% of our 2024 revenue forecast. The order and the concrete launch of the collaboration again support Aiforia’s strong growth prospects.

This is an exciting company; many see a lot of upside potential… but there are risks as well.

Aiforia’s revenue growth stalled in the first half of the year, particularly in the US, although recent months’ customer wins suggest that the company is continuing to capture the market. Our near-term forecasts have been reduced significantly and we now see a more likely need for additional capital, but customer wins and good sales prospects have improved visibility on revenue growth. After the share price increase (+17%), we think the stock looks quite correctly priced. We reiterate our EUR 4.6 target price and switch our recommendation to Reduce (previous Accumulate).

We reiterate our EUR 4.6 target price and raise our recommendation to Accumulate (was Reduce). Building of Aiforia’s growth continues and a positive news flow is expected from the company, especially on the sales front, but also on regulatory approvals progressing in Europe. The company’s customer gains have brought predictability to growth, although forecasting risks, especially in terms of growth timing and in the long term also concerning the revenue level, remain high. We believe Aiforia has clear preconditions to grow into one of the long-term winners in its market and after the share price drop (-12%), we find the risk/reward ratio attractive even within a year.

Aiforia har fått CE-certifikat enligt den nya EU-förordningen (IVDR) och har lanserat tre nya AI-modeller. Detta möjliggör expansion inom kliniska partnerskap och ökar storleken på nya avtal.

Jag rekommenderar att läsa analytikerns kommentar.